Mexico Macro Daily(Beta Mode)

Mexican Inflation Undershoots, Peso Lifts IPC

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 67,846.29 | +1.30% |

| USD/MXN | 17.42 | -0.19% |

| EUR/MXN | 19.89 | -0.97% |

| WTI Crude | 86.59 | -1.28% |

| Silver | 66.39 | +3.92% |

| Gold | 4,199.50 | +2.67% |

| Brent Crude | 89.30 | -1.19% |

| Bitcoin | 63,906.30 | +0.54% |

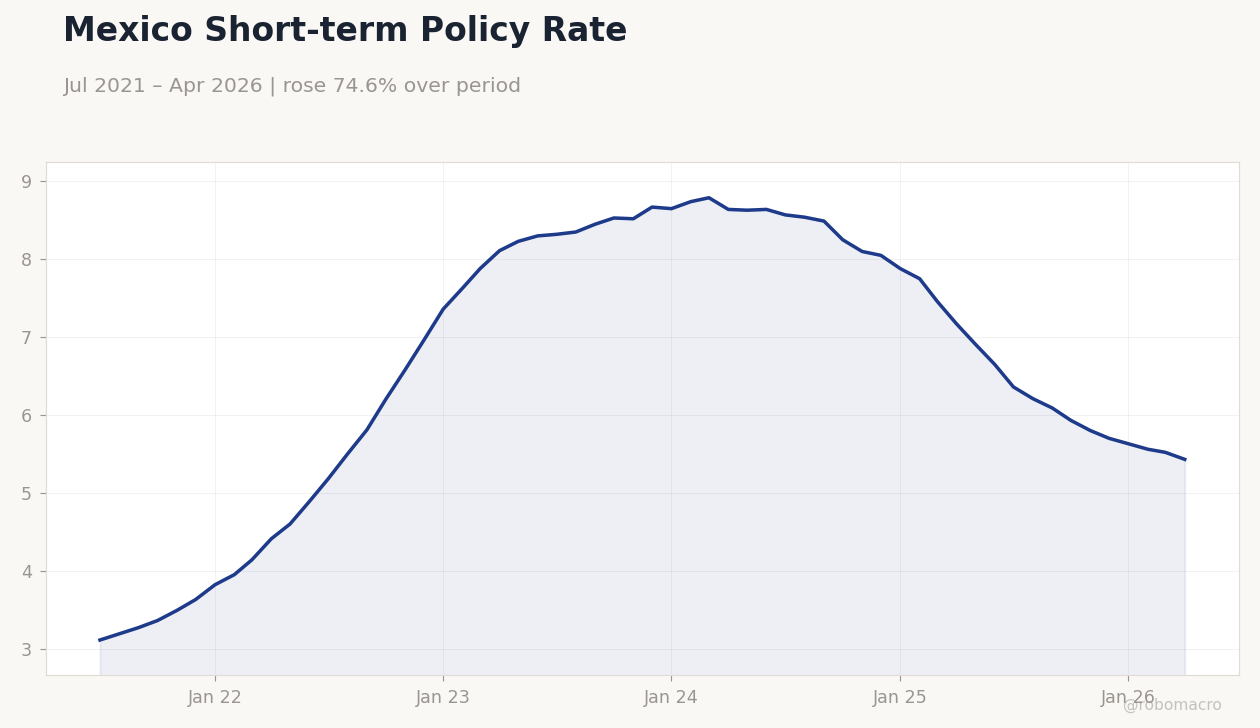

| Mexico Short-term Rate | 5.43% | -1.63% |

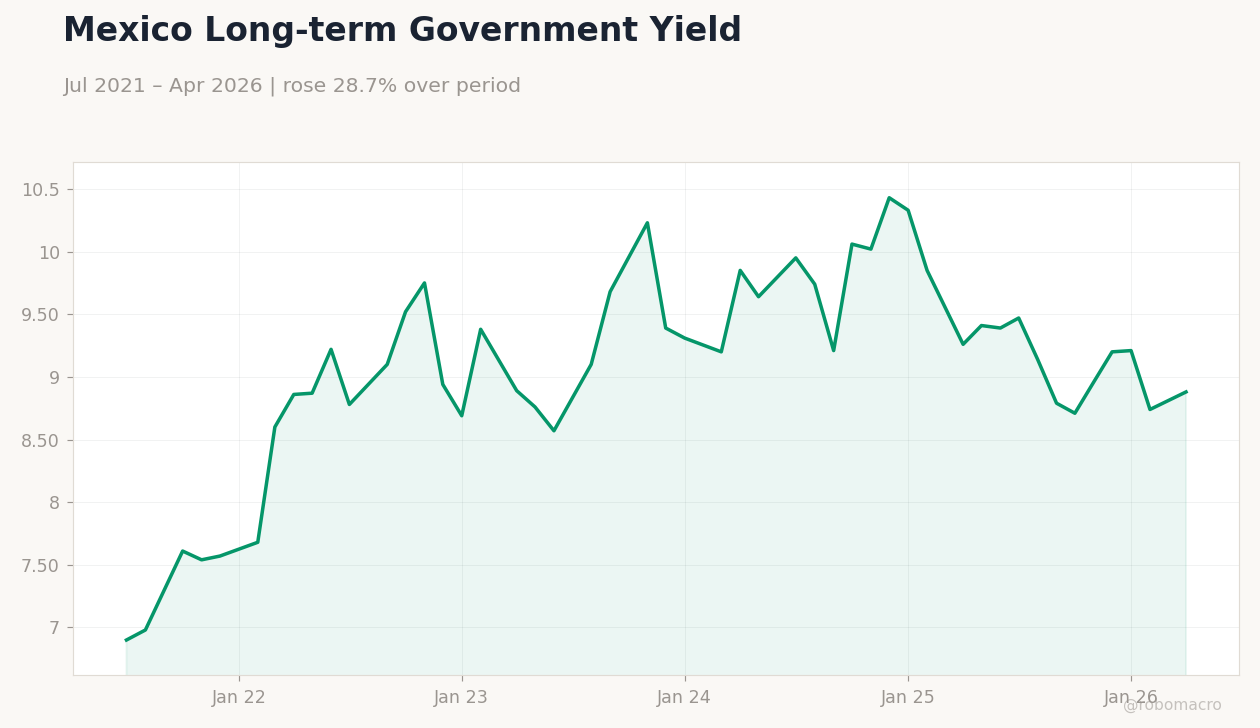

| Mexico Long-term Rate | 8.88% | +1.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Month-over-Month | 0.20 | -0.12 | -0.21 |

| Inflation Rate Year-over-Year | 4.45 | 4.03 | 3.94 |

Mexico Short-term Policy Rate | Type: macro_line | Policy Rate %: 5.43 (2026-04-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.43

Mexico Short-term Policy Rate | Type: macro_line | Policy Rate %: 5.43 (2026-04-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.43

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Mexico May inflation missed forecasts at 3.94% y/y and -0.21% m/m

- IPC Bolsa advanced 1.30% to 67,846.29 while USD/MXN fell 0.19% to 17.42

- Short-term rate steady at 5.43% as long-term yields rose to 8.88%

Yesterday's Recap

Mexico’s May inflation rate came in at 3.94% year-over-year, below the 4.03% consensus and prior 4.45% reading. The month-over-month figure printed -0.21%, softer than the -0.12% expected. Equity markets responded positively, lifting the IPC Bolsa 1.30% to close at 67,846.29.

The peso firmed, with USD/MXN declining 0.19% to 17.42 and EUR/MXN dropping 0.97% to 19.89. Short-term Mexican rates held at 5.43%, down 1.63% on the day, while long-term yields climbed 1.60% to 8.88%. Commodity moves included WTI Crude falling 1.28% to 86.59 and gold rising 2.67% to 4,199.50, providing mixed external signals for Mexican assets.

The Day Ahead

No major Mexican data releases are scheduled for today or tomorrow according to the calendar. Markets will monitor global risk sentiment and any follow-through from the World Cup opening in Mexico City. Focus remains on incoming U.S.

trade data and USMCA compliance updates that could influence nearshoring flows. Peso volatility may stay contained absent fresh Banxico commentary. Participants will watch long-term yields for any further steepening after yesterday’s move.

Other Economic Notes

Nearshoring continues to support Mexican manufacturing and FDI inflows under the USMCA framework. Remittance growth and private-sector investment in renewables point to sustained external demand for Mexican output. The combination of cooling inflation and stable short-term rates keeps real yields attractive for local fixed-income investors.

Equity outperformance in the IPC reflects growth exposure rather than policy divergence from Banxico.

Global Macro News

The ECB raised its policy rate by 25 basis points to 2.25%, citing persistent inflation risks despite energy-price pressures on the euro area. This move tightens global financial conditions and may limit capital inflows into emerging markets including Mexico. The U.S.

dollar remained under pressure after softer domestic CPI prints, supporting peso strength. Oil prices declined on demand concerns, weighing on Mexico’s fiscal revenues from energy exports. <i>↓ p.2</i>