Mexico Macro Daily(Beta Mode)

Peso Gains as IPC Climbs on Equity Inflows

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 68,827.10 | +1.28% |

| USD/MXN | 17.18 | -0.40% |

| EUR/MXN | 19.96 | -0.65% |

| WTI Crude | 80.34 | -5.35% |

| Silver | 71.15 | +4.85% |

| Gold | 4,380.50 | +3.93% |

| Brent Crude | 82.97 | -4.99% |

| Bitcoin | 66,372.26 | +1.01% |

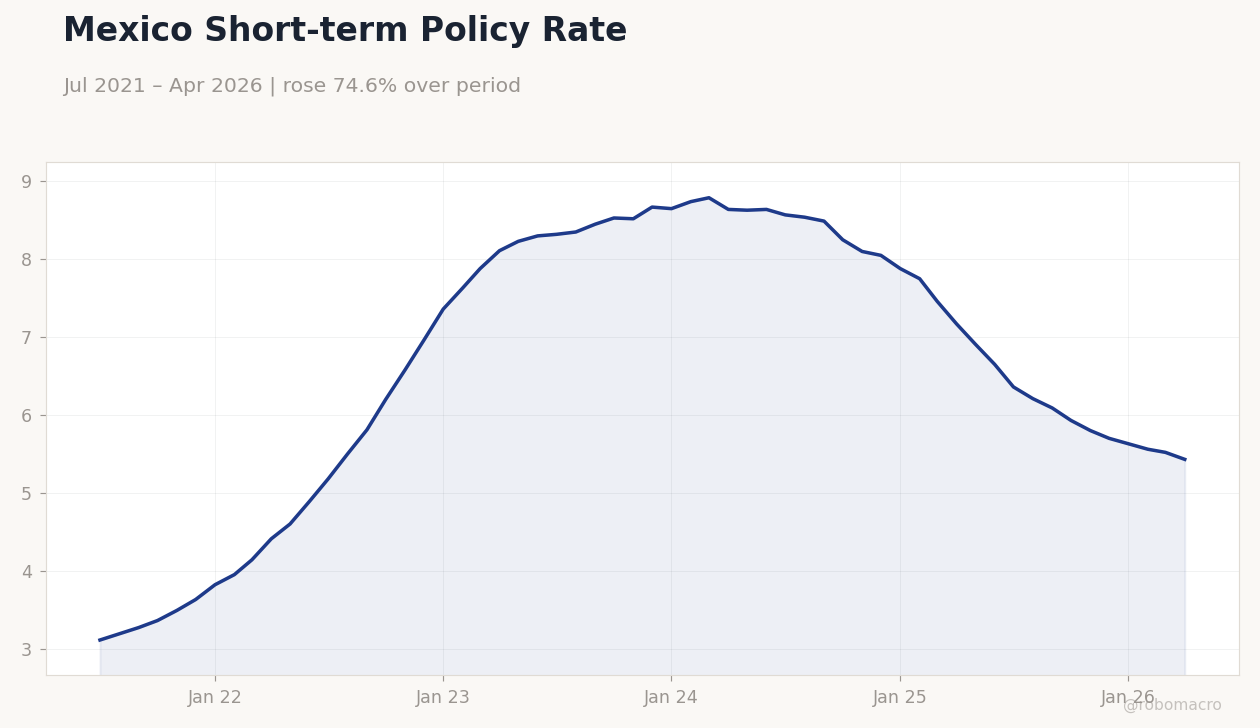

| Mexico Short-term Rate | 5.43% | -1.63% |

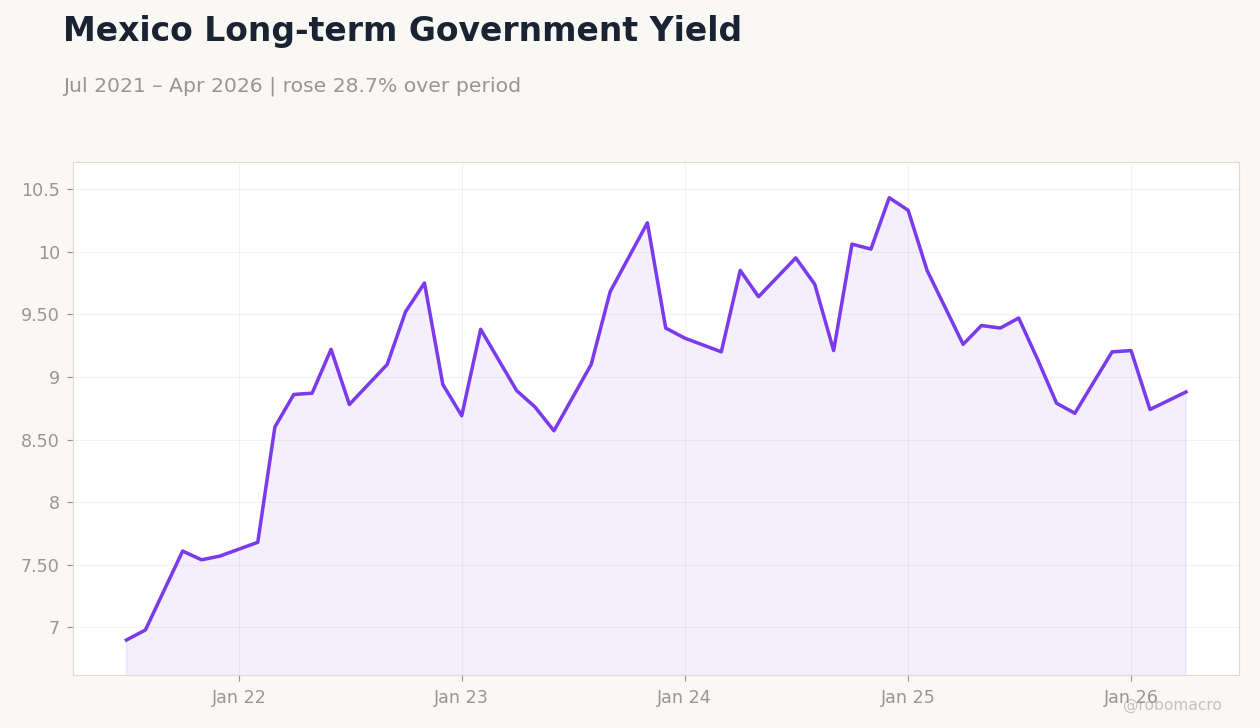

| Mexico Long-term Rate | 8.88% | +1.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Short-term Policy Rate | Type: macro_line | Rate (%): 5.43 (2026-04-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.43

Mexico Short-term Policy Rate | Type: macro_line | Rate (%): 5.43 (2026-04-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.43

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- IPC Bolsa climbed 1.28% to 68,827.10 on equity inflows.

- USD/MXN fell 0.40% to 17.18, extending peso gains.

- Mexico short-term rate held at 5.43% with long-term yields rising to 8.88%.

Yesterday's Recap

Mexico markets posted broad gains despite an empty economic calendar. The IPC Bolsa advanced 1.28 percent to close at 68,827.10 as local equities attracted inflows. USD/MXN eased 0.40 percent to 17.18 while EUR/MXN dropped 0.65 percent to 19.96, signaling broad peso resilience.

WTI Crude fell 5.35 percent to 80.34 and Brent declined 4.99 percent to 82.97, weighing on energy-linked revenues. Gold rose 3.93 percent to 4,380.50 and silver jumped 4.85 percent to 71.15, providing a partial offset through mining exposure. Mexico’s short-term rate remained at 5.43 percent while the long-term rate increased 1.60 percent to 8.88 percent.

National celebrations after the 2-0 World Cup win over South Africa lifted consumer sentiment without altering near-term data flows.

The Day Ahead

The Mexican economic calendar stays empty through mid-week with no releases scheduled. Focus will remain on external drivers including USMCA trade updates and global commodity moves. Sheinbaum’s participation in G7-related discussions at Kananaskis may generate headlines on foreign investment and energy policy.

Market participants will monitor USD/MXN for follow-through after Friday’s decline. Equity flows into IPC Bolsa are expected to stay sensitive to oil price swings and US rate signals. No Banxico communications are listed for the next session.

Other Economic Notes

Regulated import channels continue to support fiscal revenue collection amid ongoing energy-sector debate. Nearshoring momentum persists as manufacturers weigh Mexico’s cost and logistics advantages under USMCA. Tourism inflows are projected to rise further following the World Cup opening and broader Latin American travel recovery.

Blue-economy investment initiatives involving Mexico and regional peers could add longer-term capital spending. These themes remain secondary to the absence of fresh inflation or activity prints.

Global Macro News

Global risk appetite stayed constructive as Bitcoin gained 1.01 percent. European central banks kept cautious tones on rates amid mixed inflation signals. Asian currencies faced pressure, with the Philippine peso weakening faster than regional peers.

<i>↓ p.2</i>