Mexico Macro Daily(Beta Mode)

Peso Gains as IPC Climbs Amid Tariff Focus

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 67,954.55 | +1.46% |

| USD/MXN | 17.17 | -0.47% |

| EUR/MXN | 19.95 | +0.16% |

| WTI Crude | 76.59 | -5.15% |

| Silver | 70.67 | +0.85% |

| Gold | 4,365.10 | +0.86% |

| Brent Crude | 80.44 | -3.28% |

| Bitcoin | 66,087.89 | -0.30% |

| Mexico Short-term Rate | 5.36% | -1.29% |

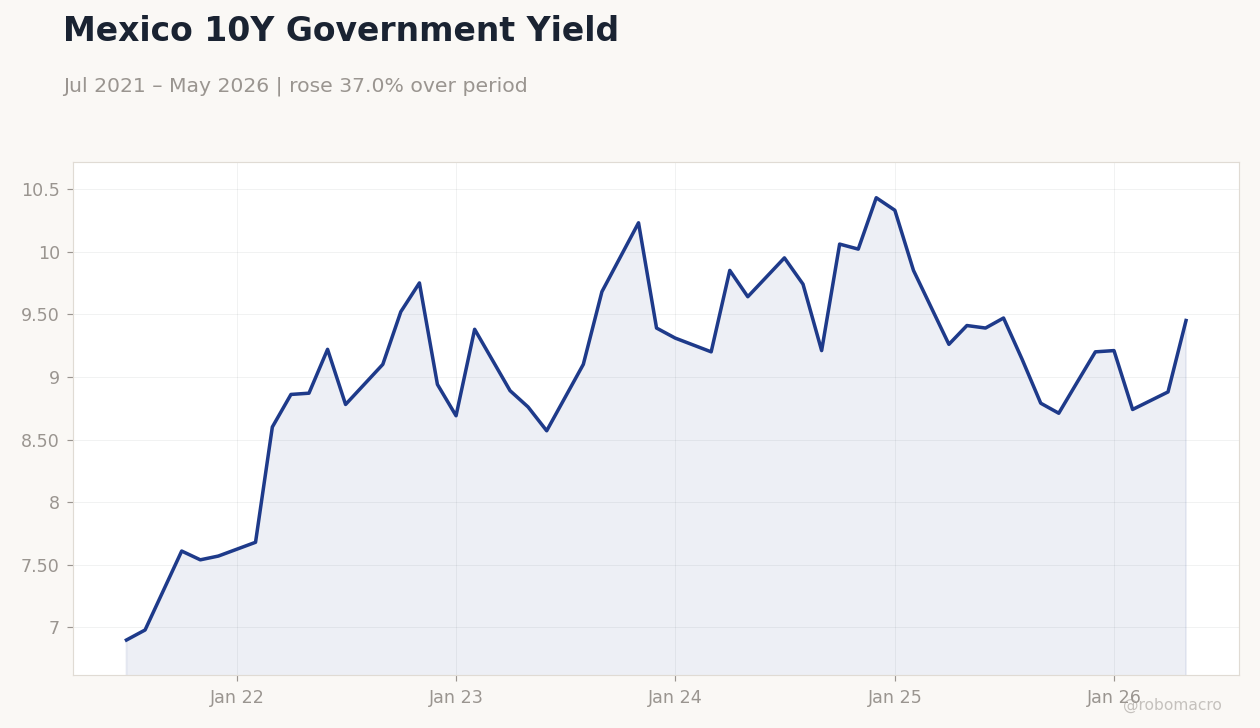

| Mexico Long-term Rate | 9.45% | +6.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico 10Y Government Yield | Type: macro_line | Long-term Yield %: 9.45 (2026-05-01) | Range: 6.9–10.43 | Trend(5pt): 6.9,9.52,9.31,9.26,9.45

Mexico 10Y Government Yield | Type: macro_line | Long-term Yield %: 9.45 (2026-05-01) | Range: 6.9–10.43 | Trend(5pt): 6.9,9.52,9.31,9.26,9.45

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- IPC Bolsa advances 1.46% to 67,954.55 while USD/MXN drops 0.47% to 17.17.

- Mexico short-term rate holds at 5.36% as long-term rate jumps 6.42% to 9.45%.

- US collects $23bn in tariffs from Mexico as USMCA consultations resume.

Yesterday's Recap

Mexican equities closed higher with the IPC Bolsa gaining 1.46% to 67,954.55, driven by nearshoring-related industrials. The peso strengthened as USD/MXN fell 0.47% to 17.17 on remittances support and tariff revenue data. Long-term yields rose sharply to 9.45%, steepening the curve and signaling repricing of easing expectations.

Short-term rates eased to 5.36%. WTI crude declined 5.15% to 76.59, weighing on energy-linked assets. News that the United States collected $23bn in tariff revenue from Mexican exports between April 2025 and April 2026 highlighted ongoing trade tensions.

USMCA dispute consultations on energy rules remain active with markets viewing a negotiated outcome as the base case.

The Day Ahead

The Mexican calendar remains quiet with no major data releases scheduled. Attention centers on USMCA talks resuming and potential tariff relief discussions. Claudia Sheinbaum’s foreign policy role at upcoming G7-related meetings may influence investor views on trade stability.

Regulated import policies continue to draw focus for their impact on fiscal revenue and investment. Market participants will monitor any signals from Washington on bilateral tariffs. Broader regional remote-work trends offer limited direct market implications for Mexico.

Other Economic Notes

Nearshoring momentum persists with new supplier announcements supporting industrial output. Legal import frameworks are highlighted as key to sustaining tax collections amid energy debates. Remittances data continue to underpin consumption and peso resilience.

Broader investment climate benefits from stable USMCA relations despite tariff friction. Fiscal impacts from regulated trade flows remain central to medium-term growth projections.

Global Macro News

The Bank of Japan raised rates to a 31-year high, tightening global financial conditions and supporting safe-haven flows into gold and silver. The ECB and RBA held or adjusted policy amid slowing growth and energy-driven inflation, affecting cross-border capital into emerging markets. <i>↓ p.2</i>