Mexico Macro Daily(Beta Mode)

Peso Weakens on Trump Cartel Rhetoric

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 68,304.73 | -0.26% |

| USD/MXN | 17.35 | +0.84% |

| EUR/MXN | 19.90 | -0.37% |

| WTI Crude | 74.44 | -3.06% |

| Silver | 66.50 | -5.94% |

| Gold | 4,261.50 | -2.23% |

| Brent Crude | 78.39 | -1.46% |

| Bitcoin | 64,303.92 | -1.98% |

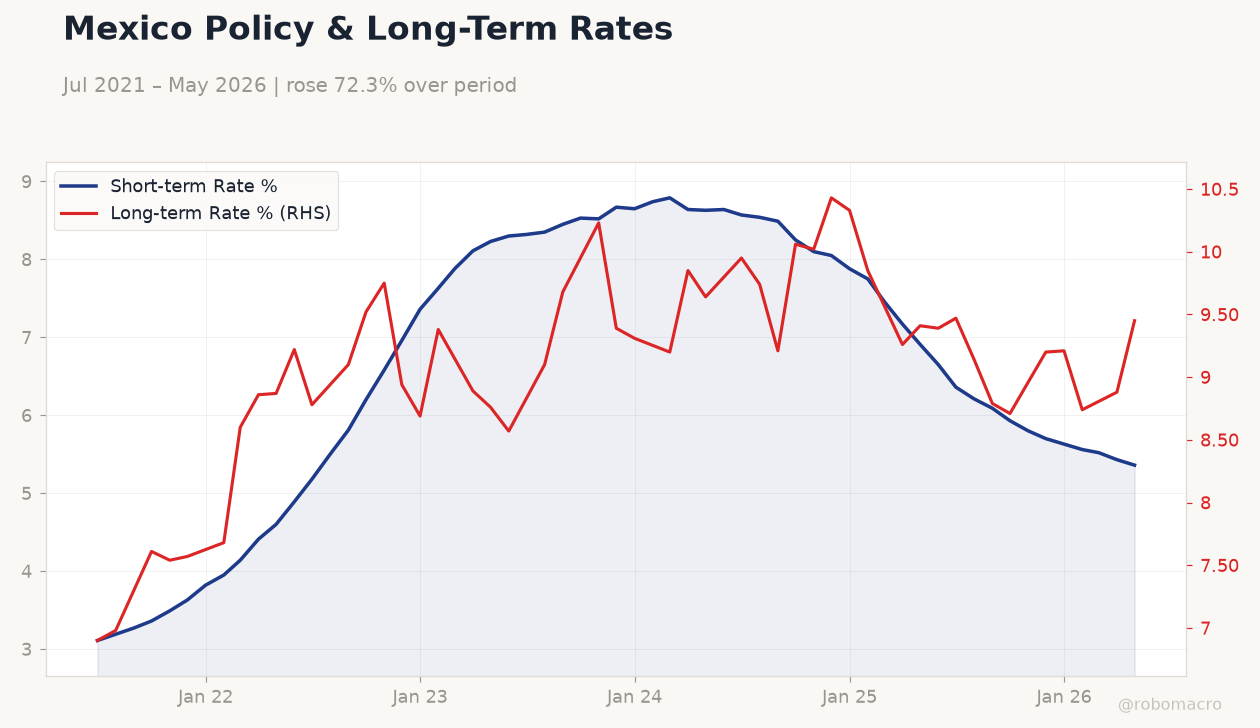

| Mexico Short-term Rate | 5.36% | -1.29% |

| Mexico Long-term Rate | 9.45% | +6.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Policy & Long-Term Rates | Type: macro_line | Short-term Rate %: 5.36 (2026-05-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.36 | Long-term Rate %: 9.45 (2026-05-01) | Range: 6.9–10.43 | Trend(5pt): 6.9,9.52,9.31,9.26,9.45

Mexico Policy & Long-Term Rates | Type: macro_line | Short-term Rate %: 5.36 (2026-05-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.36 | Long-term Rate %: 9.45 (2026-05-01) | Range: 6.9–10.43 | Trend(5pt): 6.9,9.52,9.31,9.26,9.45

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- USD/MXN climbs 0.84% to 17.35 as Trump escalates cartel governance claims at G7

- IPC Bolsa slips 0.26% to 68,304.73 while long-term yields surge 6.42% to 9.45%

- Short-term rate holds at 5.36% amid quiet calendar and global central bank pauses

Yesterday's Recap

Mexico markets absorbed fresh political pressure after President Trump stated that cartels govern Mexico during his G7 address, triggering an immediate 0.84% rise in USD/MXN to 17.35. The IPC Bolsa closed 0.26% lower at 68,304.73 as investors reduced local equity exposure. Mexico’s long-term rate jumped 6.42% to 9.45%, widening the curve while the short-term rate eased 1.29% to 5.36%.

No economic data releases occurred, leaving price action driven solely by the political headlines and global risk sentiment. WTI crude fell 3.06% to 74.44, adding modest downside pressure to the peso via energy linkages. EUR/MXN declined 0.37% to 19.90, showing limited contagion beyond the dollar pair.

The Day Ahead

Markets face another data-empty session with zero scheduled releases for 19 June. Attention will stay on follow-through from Trump’s G7 remarks and any USMCA-related statements from Washington. USD/MXN will likely test resistance near 17.40 if rhetoric intensifies, while IPC Bolsa direction hinges on Wall Street futures.

The 5.36% short-term rate remains the anchor for front-end pricing until fresh inflation prints arrive later in the month. Volatility in silver and gold, both down sharply yesterday, may spill into MXN crosses.

Other Economic Notes

Nearshoring inflows continue to support formal employment despite the absence of new project announcements. USMCA energy consultations remain stalled, keeping policy uncertainty elevated for foreign direct investment. Tourism initiatives tied to sustainable blue-economy corridors offer long-term diversification but deliver no immediate GDP boost.

Remittance flows, though unreported yesterday, historically cushion consumption when political noise rises.

Global Macro News

The Federal Reserve left rates unchanged, citing solid expansion and keeping external pressure on Banxico steady. The Bank of England held its policy rate at 3.75% as easing oil prices from the Iran context reduced UK inflation risks. The Bank of Canada is also expected to stay on hold, reinforcing a cautious global tone.

<i>↓ p.2</i>