Mexico Macro Daily(Beta Mode)

Peso Weakens as Long-Term Yields Jump

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 68,265.11 | -0.06% |

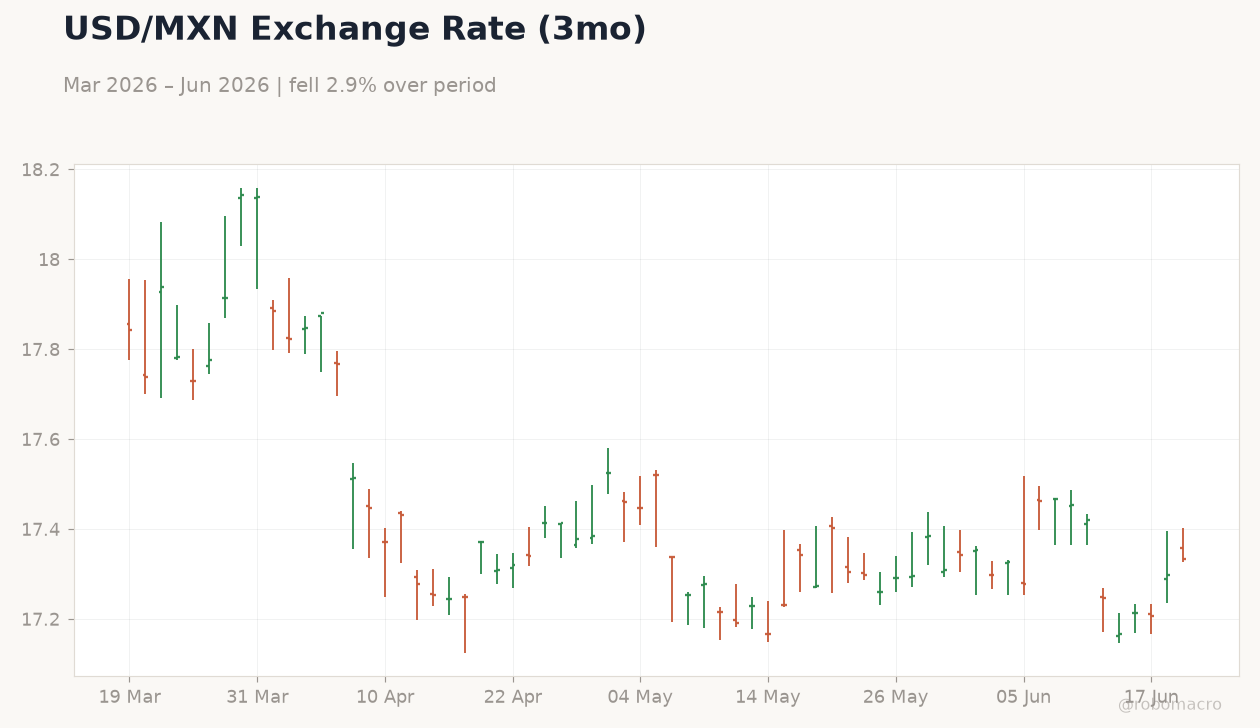

| USD/MXN | 17.30 | +0.53% |

| EUR/MXN | 19.88 | -0.13% |

| WTI Crude | 75.88 | -0.94% |

| Silver | 64.82 | -2.17% |

| Gold | 4,168.90 | -1.31% |

| Brent Crude | 79.74 | -0.14% |

| Bitcoin | 62,570.52 | -0.52% |

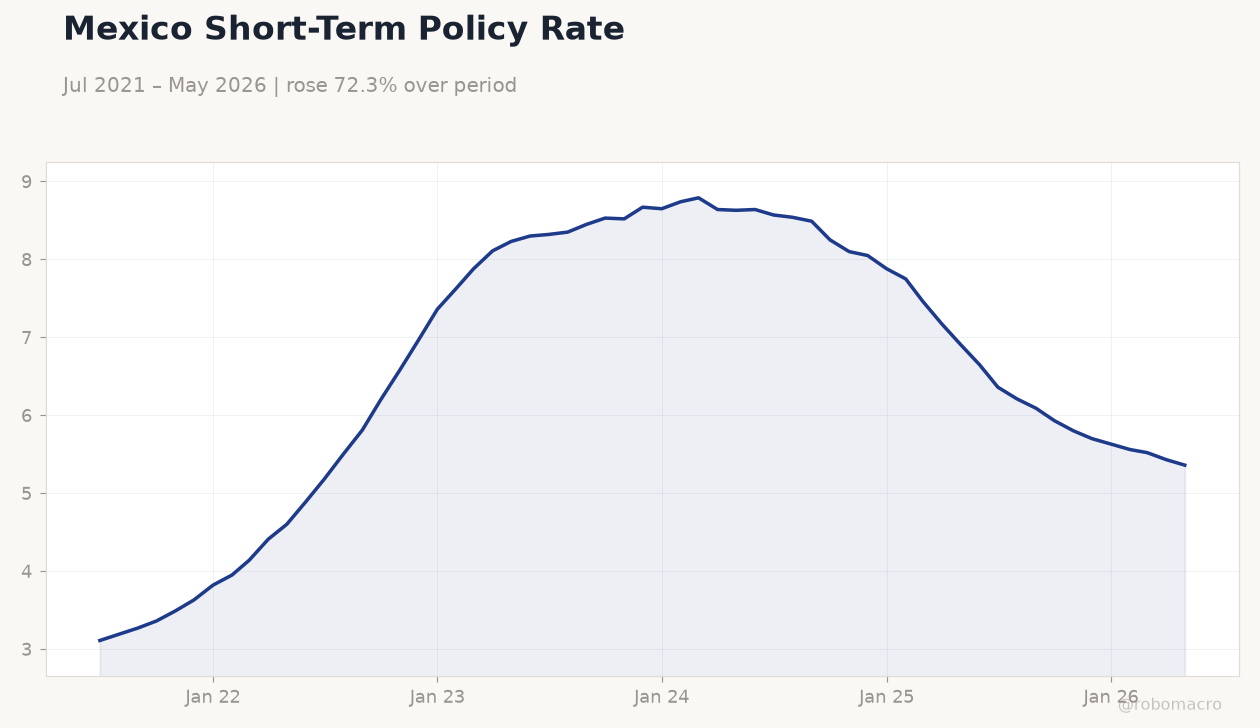

| Mexico Short-term Rate | 5.36% | -1.29% |

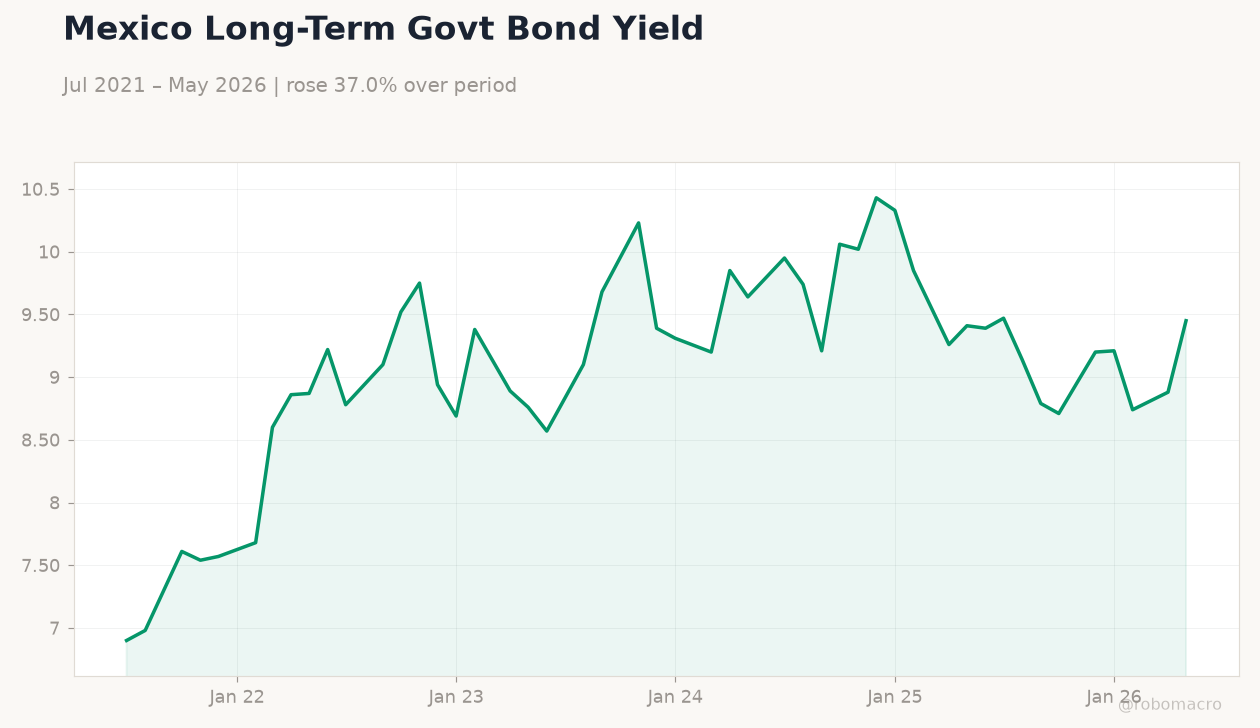

| Mexico Long-term Rate | 9.45% | +6.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Short-Term Policy Rate | Type: macro_line | Rate %: 5.36 (2026-05-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.36

Mexico Short-Term Policy Rate | Type: macro_line | Rate %: 5.36 (2026-05-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.36

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- IPC Bolsa slips 0.06% to 68,265.11 on quiet flows

- USD/MXN climbs 0.53% to 17.30 while long-term rates jump 6.42%

- Banxico short-term rate holds at 5.36% amid USMCA talks

Yesterday's Recap

No economic data releases occurred on 18 June. The IPC Bolsa finished 0.06% lower at 68,265.11 as foreign buying slowed. USD/MXN advanced 0.53% to 17.30, extending recent peso softness against the dollar.

Mexico’s long-term rate surged 6.42% to 9.45%, steepening the curve sharply, while the short-term rate eased 1.29% to 5.36%. Brent crude settled at 79.74, limiting energy-linked support for the peso. Intensifying USMCA review consultations in Washington added caution without triggering immediate volatility.

WTI crude fell 0.94% to 75.88 and gold dropped 1.31% to 4,168.90, reflecting softer risk appetite across commodities. Silver declined 2.17% to 64.82. Bitcoin eased 0.52% to 62,570.52.

The moves occurred against a backdrop of no fresh Banxico commentary and limited regional data.

The Day Ahead

No Mexican data prints or Banxico events are scheduled for 19 June. Traders will monitor progress on USMCA automotive-rules consultations in Washington. Global central-bank decisions from the Bank of Canada and Bank of England may influence USD/MXN direction.

Focus stays on long-term yield stability after yesterday’s sharp move. Any fresh comments on nearshoring FDI commitments could support sentiment toward the peso. Markets also track broader North American trade developments ahead of U.S.

midterms.

Other Economic Notes

USMCA review discussions now test Mexico’s China and Asia policy stance, with lawmakers anxious ahead of midterms. Nearshoring announcements continue in northern states, sustaining FDI momentum despite stalled energy-reform legislation. Sustainable tourism initiatives linking Mexico with Costa Rica and Colombia aim to boost coastal revenues through marine conservation.

Brazil’s stronger M&A activity has widened its lead over Mexico in regional deal flow. JD Vance’s remarks on potential U.S. action against cartels introduced additional political noise around bilateral security cooperation.