Mexico Macro Daily(Beta Mode)

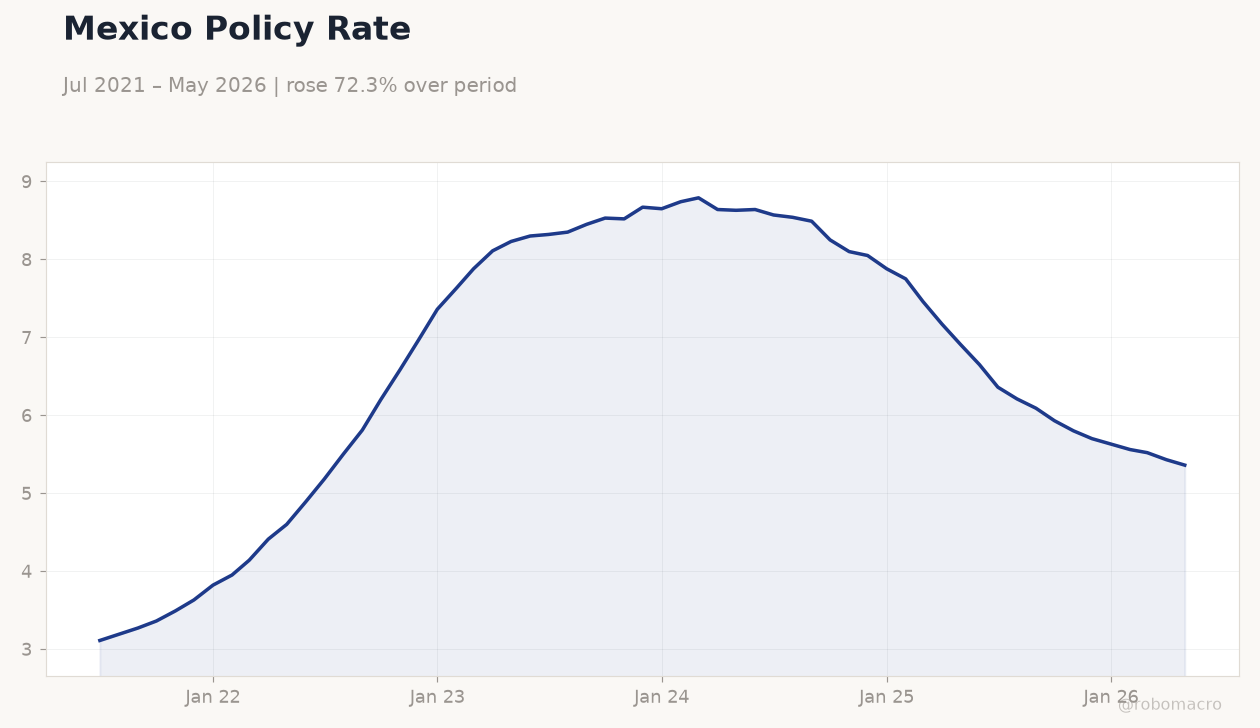

Banxico Set to Hold Rate at 6.5%

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 66,848.42 | -0.41% |

| USD/MXN | 17.61 | +1.42% |

| EUR/MXN | 19.84 | -0.20% |

| WTI Crude | 71.06 | -2.94% |

| Silver | 59.85 | -3.50% |

| Gold | 4,064.00 | -1.60% |

| Brent Crude | 74.77 | -3.00% |

| Bitcoin | 62,772.59 | +0.17% |

| Mexico Short-term Rate | 5.36% | -1.29% |

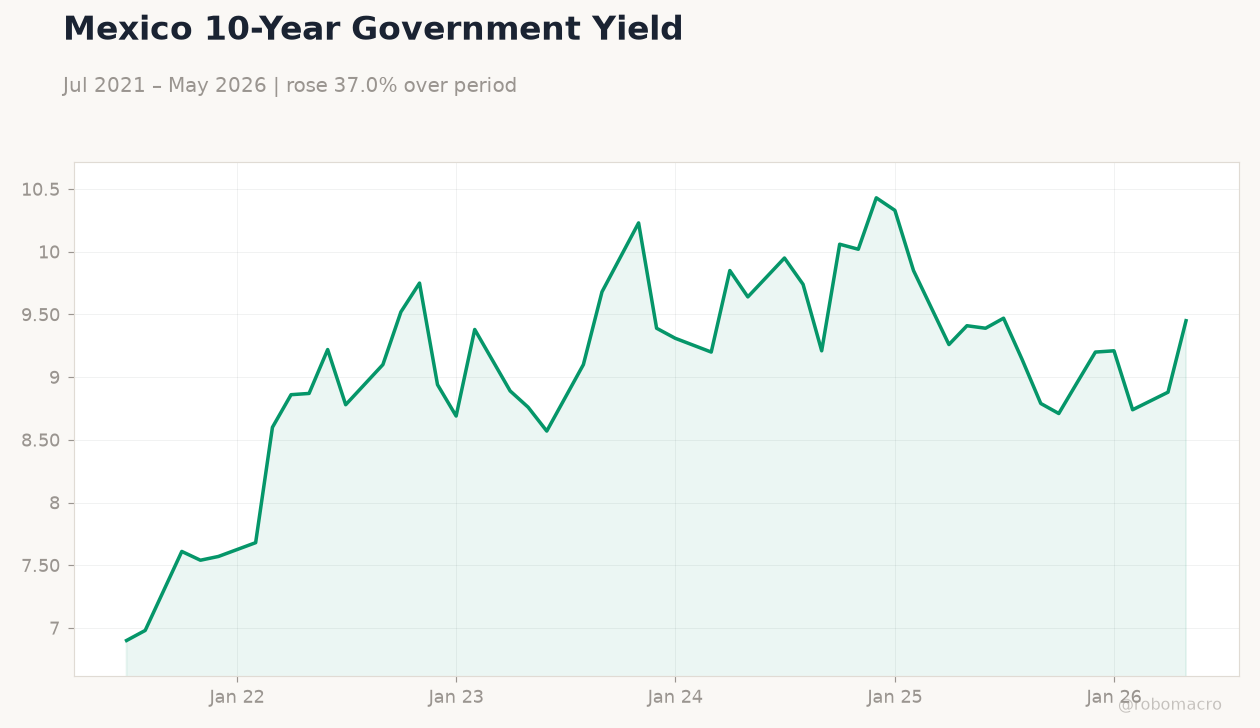

| Mexico Long-term Rate | 9.45% | +6.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Policy Rate | Type: macro_line | Policy Rate %: 5.36 (2026-05-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.36

Mexico Policy Rate | Type: macro_line | Policy Rate %: 5.36 (2026-05-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.36

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-06-25) | |||

| Central Bank Interest Rate Decision | 6.50 | 6.50 | 11:00 |

| Friday (2026-06-26) | |||

| Trade Balance | 4,520m | - | 04:00 |

- Banxico expected to hold policy rate at 6.5% tomorrow with markets pricing limited easing ahead.

- USD/MXN jumps 1.42% to 17.61 while IPC Bolsa falls 0.41% to 66,848.42 on risk-off flows.

- Pemex-Petrobras accord signals fresh nearshoring push in energy amid stable remittances.

Yesterday's Recap

Mexican markets closed mixed on June 23 with no major data releases. IPC Bolsa declined 0.41% to 66,848.42 as financials lagged. USD/MXN rose 1.42% to 17.61 while EUR/MXN eased 0.20% to 19.84.

WTI Crude dropped 2.94% to 71.06 and Brent fell 3.00% to 74.77. Mexico short-term rate stood at 5.36% and long-term rate climbed to 9.45%. Heavy rains triggered alerts in Mexico City but caused no immediate market disruption.

The peso underperformed regional peers on broad dollar strength.

The Day Ahead

Banxico will announce its interest rate decision at 11:00 ET on June 25 with consensus pointing to a hold at 6.5%. Traders will parse the statement for any shift in forward guidance on inflation. Mexico trade balance for May follows on June 26 at 04:00 ET.

No other high-impact local releases are scheduled. Markets will also monitor USMCA-related comments from officials in Washington. The decision and any accompanying tone on nearshoring will set the tone for Mbono yields and USD/MXN.

Other Economic Notes

Pemex and Petrobras signed a memorandum to expand joint projects in exploration, refining and petrochemicals, extending nearshoring momentum into energy. Record remittances continue to underpin the current account and provide a floor for the peso. Energy-reform discussions in Congress remain stalled, keeping private power investment on hold.

USMCA automotive rules-of-origin talks stay in technical consultations without immediate tariff risks. These factors support a constructive medium-term view for Mexican growth despite near-term FX volatility.

Global Macro News

The Bank of England cut its main rate by 25 bp to 4.50% as UK growth stagnates. Thailand’s central bank held rates steady while Switzerland’s SNB kept policy unchanged amid currency concerns. A Bank of England rate-setter called for an extended hold, echoing caution seen in other advanced economies.

<i>↓ p.2</i>