Mexico Macro Daily(Beta Mode)

Inflation Eases Ahead of Banxico Hold

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 66,278.01 | -0.85% |

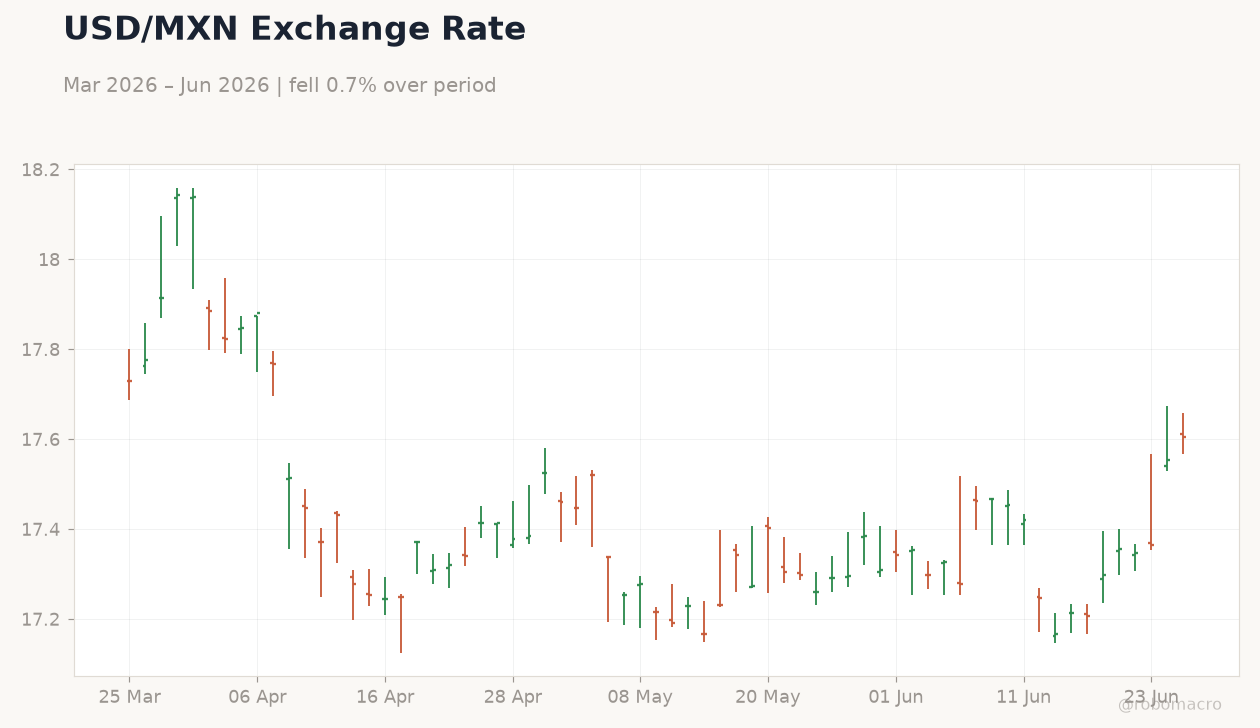

| USD/MXN | 17.61 | +0.31% |

| EUR/MXN | 19.97 | +0.65% |

| WTI Crude | 69.87 | -0.67% |

| Silver | 57.99 | -0.12% |

| Gold | 4,031.40 | +1.03% |

| Brent Crude | 73.60 | -0.19% |

| Bitcoin | 60,004.82 | -1.62% |

| Mexico Short-term Rate | 5.36% | -1.29% |

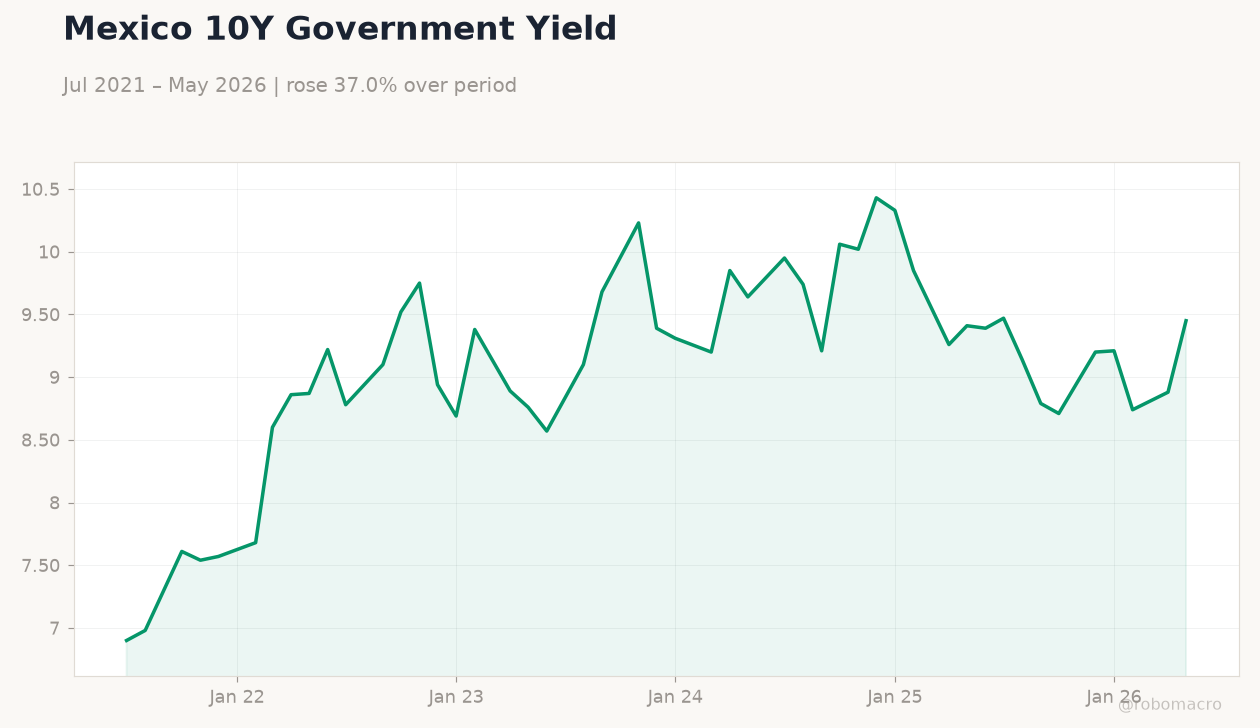

| Mexico Long-term Rate | 9.45% | +6.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

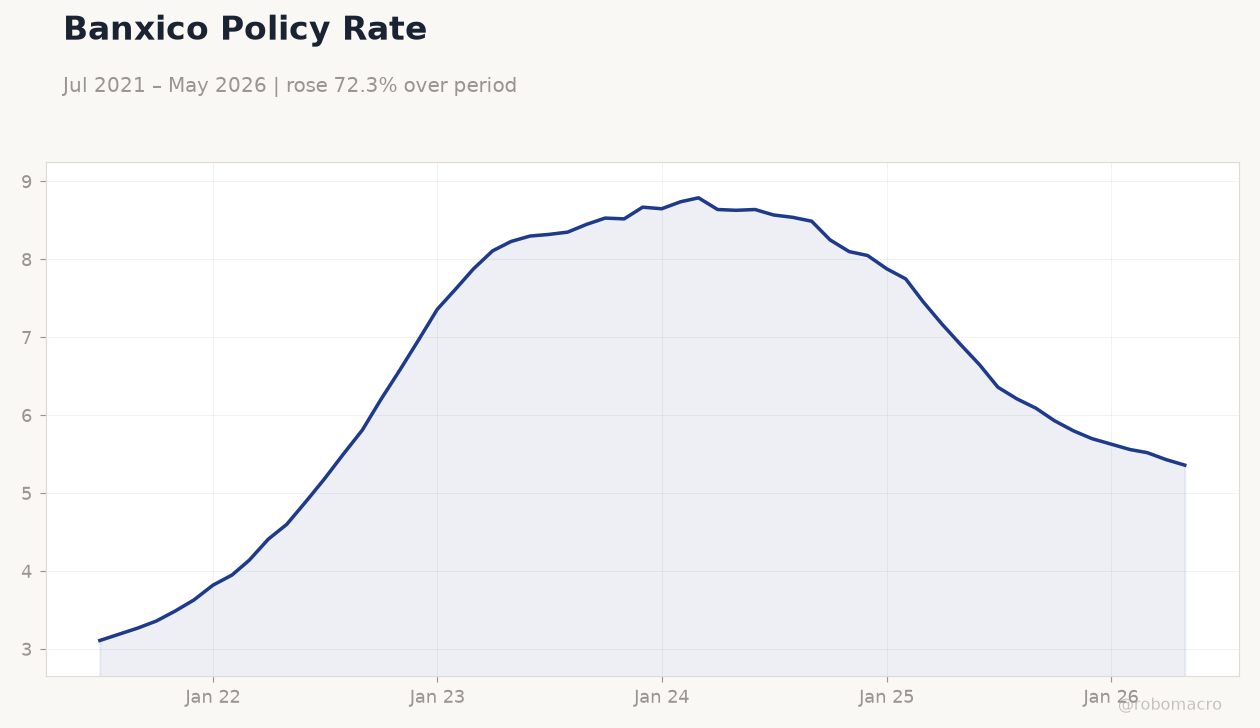

Banxico Policy Rate | Type: macro_line | Policy Rate %: 5.36 (2026-05-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.36

Banxico Policy Rate | Type: macro_line | Policy Rate %: 5.36 (2026-05-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.36

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Central Bank Interest Rate Decision | 6.50 | 6.50 | 11:00 |

| Friday (2026-06-26) | |||

| Trade Balance | 4,520m | - | 04:00 |

- Mexico annual inflation eased more than expected in early June, supporting a steady policy rate.

- Banxico is expected to hold the benchmark rate at today’s decision amid cooling price pressures.

- IPC Bolsa fell 0.85% while USD/MXN rose 0.31% to 17.61 as markets priced limited easing.

Yesterday's Recap

Mexico’s annual inflation print surprised to the downside, arriving one day before the central bank meeting and reinforcing expectations for no change in the policy rate. Equity markets reacted with the IPC Bolsa declining 0.85% to 66,278.01 amid profit-taking after recent gains. The peso weakened modestly, with USD/MXN advancing 0.31% to 17.61 and EUR/MXN rising 0.65% to 19.97.

Short-term Mexican rates eased 1.29% to 5.36% while long-term yields climbed 6.42% to 9.45%, reflecting a steepening curve. Commodity moves offered limited support, with WTI crude falling 0.67% to 69.87 and gold rising 1.03% to 4,031.40. No major data releases occurred on June 24, leaving the inflation report as the dominant domestic driver.

The Day Ahead

Banxico will announce its interest rate decision at 11:00 ET, with consensus pointing to a hold at the current level following the softer inflation outcome. Tomorrow morning brings the May trade balance, which posted a 4.52 billion USD surplus in the prior month and will update views on external demand. Market participants will scrutinize the accompanying statement for any shifts in forward guidance on inflation convergence.

Attention will also turn to any references to nearshoring investment flows and USMCA trade dynamics. Volatility in USD/MXN is likely around the announcement as positioning adjusts.

Other Economic Notes

Cooling inflation broadens the window for Banxico to maintain its restrictive stance without risking growth. Nearshoring continues to underpin manufacturing exports and foreign direct investment under the USMCA framework. The combination of lower price pressures and steady external demand supports a soft-landing scenario for the Mexican economy.

Fiscal accounts remain stable, limiting upside risks to long-term yields despite the recent steepening.

Global Macro News

The Federal Reserve is projected to deliver two rate cuts by May 2027, keeping external financial conditions supportive for emerging-market assets including the peso. <i>↓ p.2</i>