Mexico Macro Daily(Beta Mode)

Banxico Holds at 6.5%, Trade Surplus Shrinks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 67,416.22 | +1.72% |

| USD/MXN | 17.48 | -0.81% |

| EUR/MXN | 19.96 | -0.20% |

| WTI Crude | 69.64 | -3.17% |

| Silver | 58.67 | +0.56% |

| Gold | 4,065.00 | +0.86% |

| Brent Crude | 72.99 | -3.02% |

| Bitcoin | 59,282.27 | -0.74% |

| Mexico Short-term Rate | 5.36% | -1.29% |

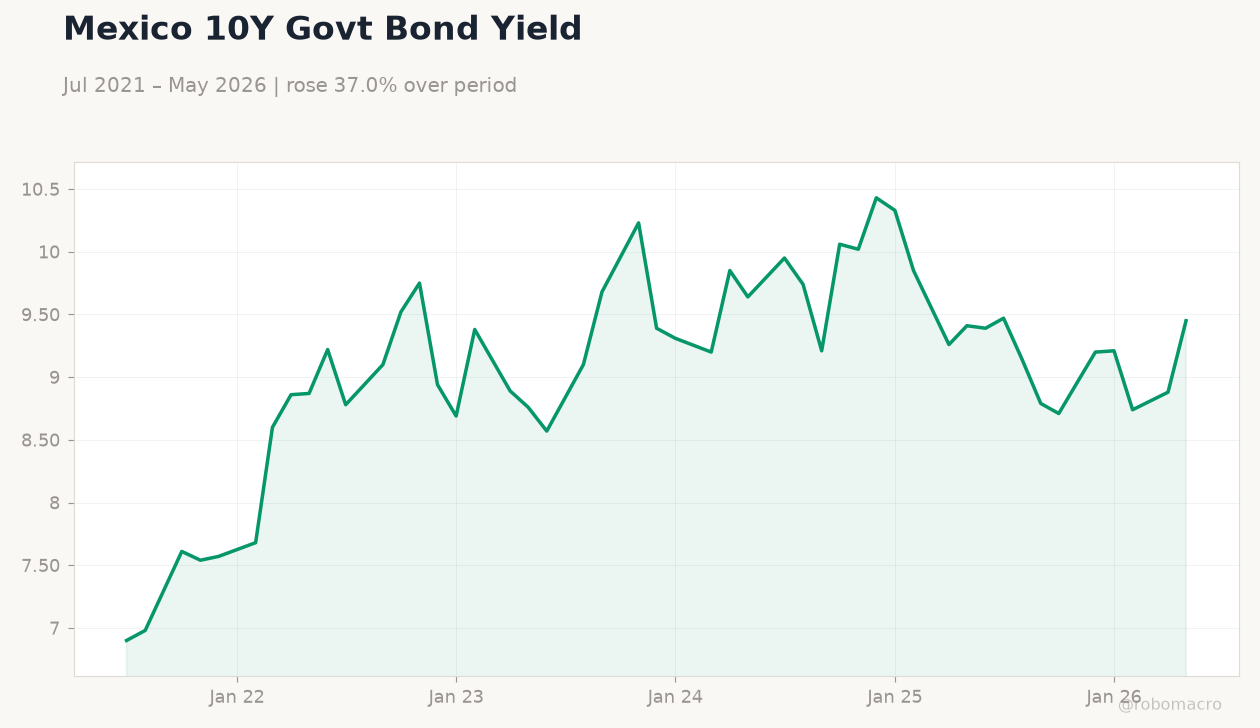

| Mexico Long-term Rate | 9.45% | +6.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

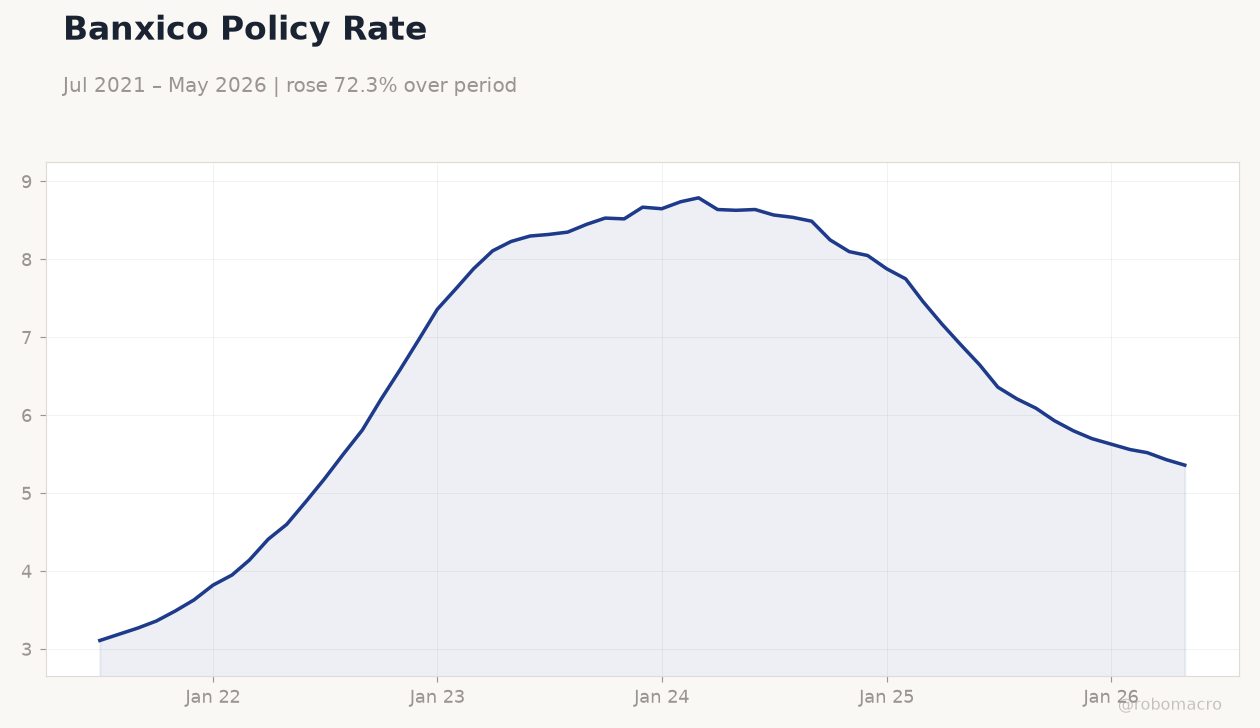

| Central Bank Interest Rate Decision | 6.50 | 6.50 | 6.50 |

| Trade Balance | 4,520m | - | 2,259m |

Banxico Policy Rate | Type: macro_line | Policy Rate %: 5.36 (2026-05-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.36

Banxico Policy Rate | Type: macro_line | Policy Rate %: 5.36 (2026-05-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.36

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Banxico kept the policy rate at 6.5% and signaled a prolonged hold amid softening growth.

- Mexico’s trade surplus narrowed to 2.259 billion USD from 4.52 billion USD previously.

- IPC rose 1.72% while USD/MXN fell 0.81% to 17.48 on the steady policy stance.

Yesterday's Recap

Banxico held its benchmark rate at 6.5% and indicated the level would remain in place for longer while monitoring economic weakness. The trade balance printed a 2.259 billion USD surplus, down sharply from the prior 4.52 billion USD reading. The IPC Bolsa advanced 1.72% to close at 67,416.22, led by industrial names.

USD/MXN declined 0.81% to 17.48 and EUR/MXN eased 0.20% to 19.96. Mexico’s short-term rate stood at 5.36% while the long-term rate climbed 6.42% to 9.45%. WTI crude fell 3.17% to 69.64, weighing on energy-linked pesos.

The peso outperformed regional peers after the central bank’s steady message.

The Day Ahead

No Mexico-specific data releases are scheduled for 26 June. Markets will monitor US initial jobless claims and durable-goods orders for any spillover into MXN volatility. OIS pricing continues to embed limited Banxico easing this year after yesterday’s hold.

Equity desks await corporate updates on nearshoring projects in northern states. The absence of local prints leaves USD/MXN and Mbono curves sensitive to US data surprises.

Other Economic Notes

Nearshoring inflows remain supportive of manufacturing exports and formal employment despite softer domestic demand signals. USMCA rules-of-origin disputes have yet to disrupt announced auto-supplier investments in Nuevo León. Remittance inflows continue above 5 billion USD monthly, providing a steady current-account buffer.

Energy-reform delays until September leave Pemex credit metrics unchanged in the near term.

Global Macro News

The IMF noted solid US momentum and endorsed the Fed’s decision to hold rates steady, reducing immediate pressure on emerging-market currencies. The RBA left Australian rates unchanged, reinforcing a cautious global policy backdrop. Brazil’s inclusion in extended-stay tourism trends highlights regional competition for investment flows that Mexico also targets via nearshoring.

<i>↓ p.2</i>