Mexico Macro Daily(Beta Mode)

Peso Holds Steady as Banxico Anchors Rate at 5.36%

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 67,226.01 | -0.28% |

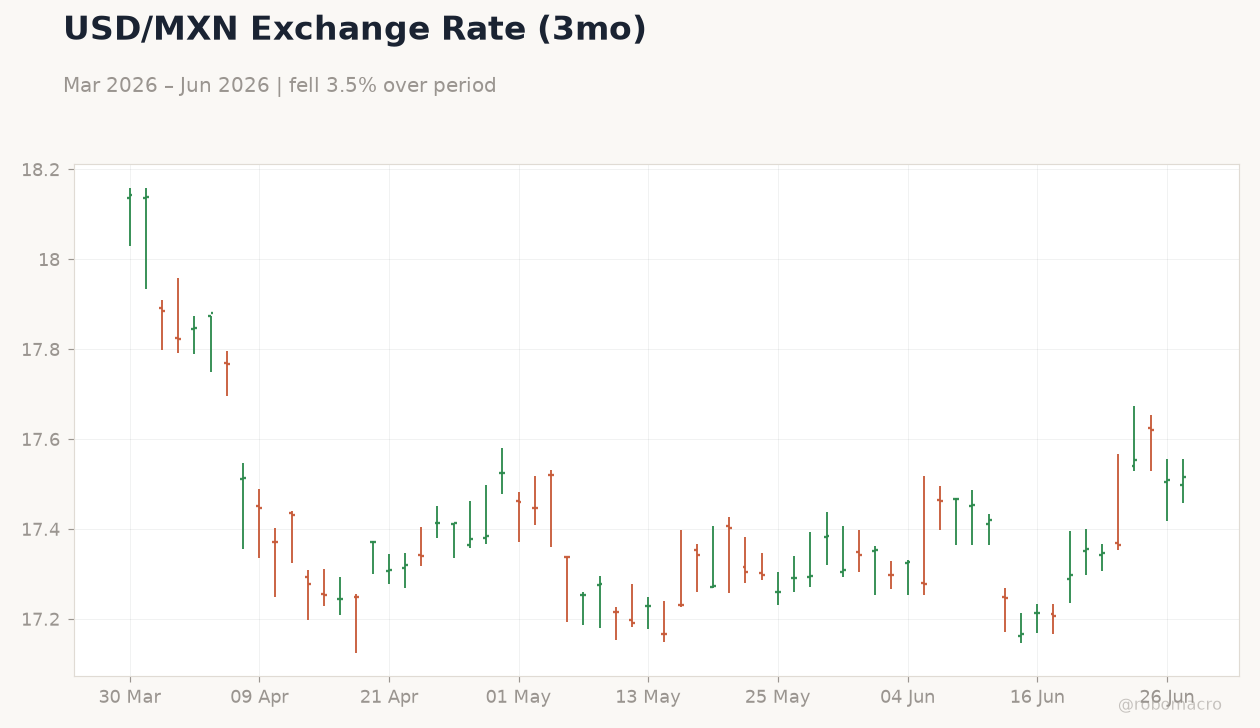

| USD/MXN | 17.51 | -0.63% |

| EUR/MXN | 19.97 | +0.39% |

| WTI Crude | 70.26 | +1.49% |

| Silver | 58.90 | -0.54% |

| Gold | 4,056.80 | -0.54% |

| Brent Crude | 73.47 | +2.06% |

| Bitcoin | 59,932.57 | +0.67% |

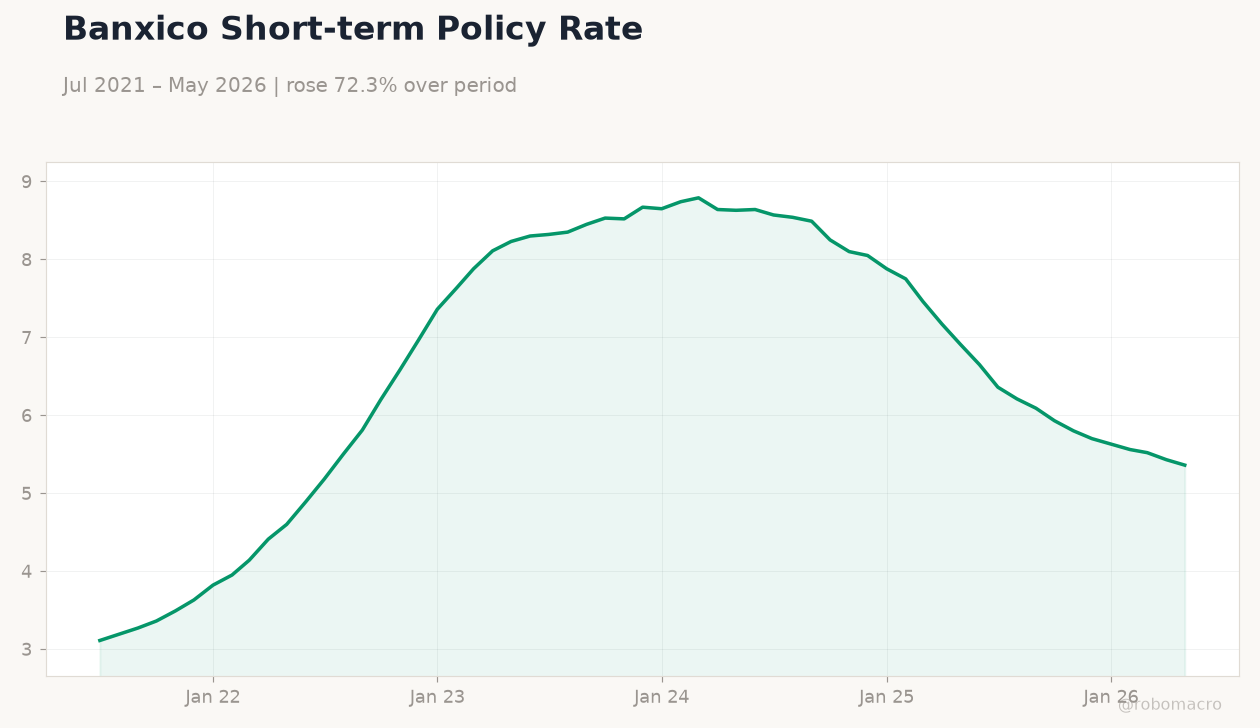

| Mexico Short-term Rate | 5.36% | -1.29% |

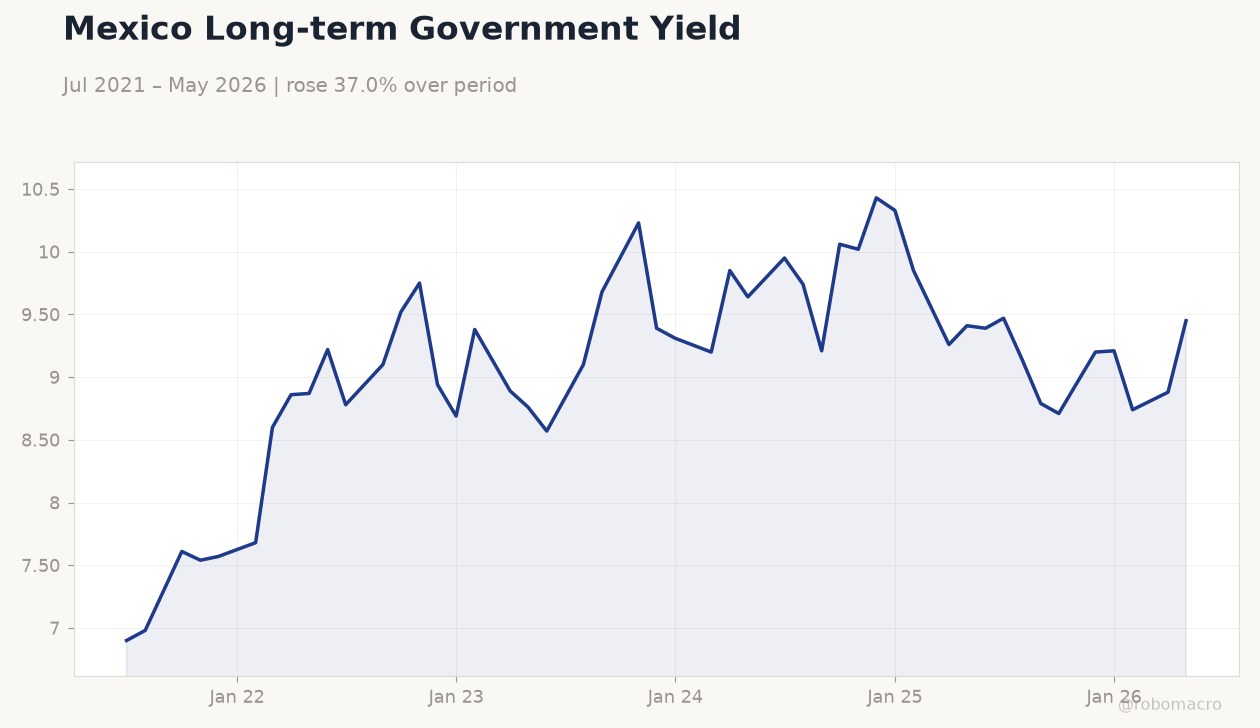

| Mexico Long-term Rate | 9.45% | +6.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Long-term Government Yield | Type: macro_line | Percent: 9.45 (2026-05-01) | Range: 6.9–10.43 | Trend(5pt): 6.9,9.52,9.31,9.26,9.45

Mexico Long-term Government Yield | Type: macro_line | Percent: 9.45 (2026-05-01) | Range: 6.9–10.43 | Trend(5pt): 6.9,9.52,9.31,9.26,9.45

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-07-01) | |||

| Business Confidence Index | 47.50 | - | 04:00 |

| Friday (2026-07-03) | |||

| Consumer Confidence Index | 43.50 | - | 04:00 |

- USD/MXN falls 0.63% to 17.51 on thin positioning and steady Banxico policy

- IPC Bolsa slips 0.28% while Mexico long-term rate jumps 6.42% to 9.45%

- Business Confidence Index due 1 July offers next local data signal

Yesterday's Recap

Mexico markets closed the session with the peso outperforming regional peers as USD/MXN declined to 17.51. The IPC Bolsa index finished at 67,226.01, pressured by a sharp 6.42% rise in the long-term rate to 9.45%. Short-term rates remained anchored at 5.36%, reflecting unchanged Banxico policy.

WTI crude advanced 1.49% to 70.26, providing modest support to energy-linked names, while silver and gold both declined 0.54%. EUR/MXN rose 0.39% to 19.97, highlighting selective strength in the peso against the dollar only. No economic releases occurred on 28 June, leaving price action driven by external flows and positioning ahead of the long weekend.

Bitcoin gained 0.67% but showed limited correlation with MXN moves.

The Day Ahead

Markets will focus on the 1 July Business Confidence Index release, the first material Mexican data point since late May. The print arrives alongside the 3 July Consumer Confidence Index, both carrying medium impact. No Banxico speakers or minutes are scheduled before the long weekend.

A stronger-than-expected business reading would likely compress long-term Mbono yields and support further MXN outperformance. Conversely, a downside surprise could reopen questions about the durability of the 5.36% short-term rate. Traders will also monitor USMCA-related headlines for any fresh tariff signals.

Other Economic Notes

Nearshoring momentum persists as Chinese vehicle makers expand assembly capacity in Mexico and Canada, raising USMCA compliance risks. Remittance inflows continue to underpin the current-account surplus and MXN carry trades. Private-sector energy permits in Tamaulipas signal gradual implementation of recent reforms.

Tourism inflows tied to the 2026 World Cup are boosting service-sector activity in northern states. These trends collectively reinforce Mexico’s external resilience despite global rate volatility.

Global Macro News

Global central-bank commentary turned cautious, with RBA and SARB signals pointing to extended holds that limit pressure on emerging-market currencies. Philippine and Vietnamese rate paths remain higher for longer, supporting carry differentials versus Mexico. <i>↓ p.2</i>