Mexico Macro Daily(Beta Mode)

USMCA Deadline Clouds Peso Resilience

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 67,640.59 | +0.62% |

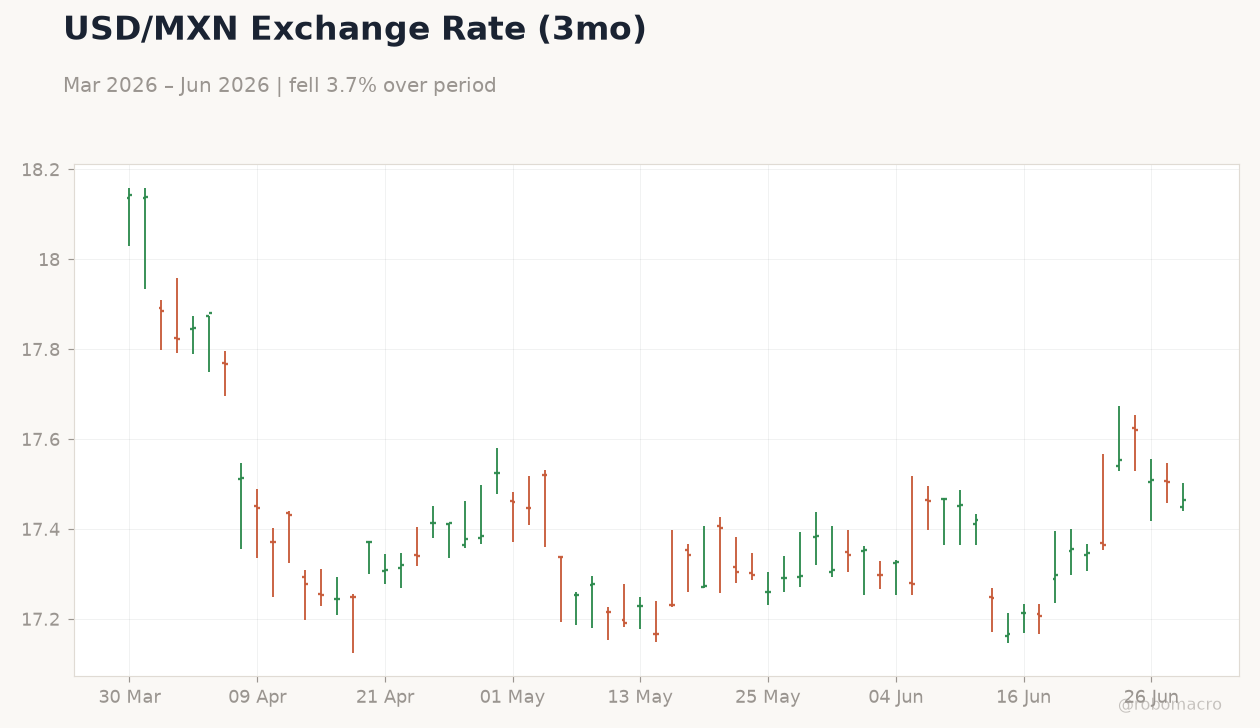

| USD/MXN | 17.46 | -0.26% |

| EUR/MXN | 19.89 | -0.18% |

| WTI Crude | 70.99 | +0.34% |

| Silver | 59.44 | +2.17% |

| Gold | 4,045.00 | +0.56% |

| Brent Crude | 74.23 | +1.48% |

| Bitcoin | 59,042.55 | -1.82% |

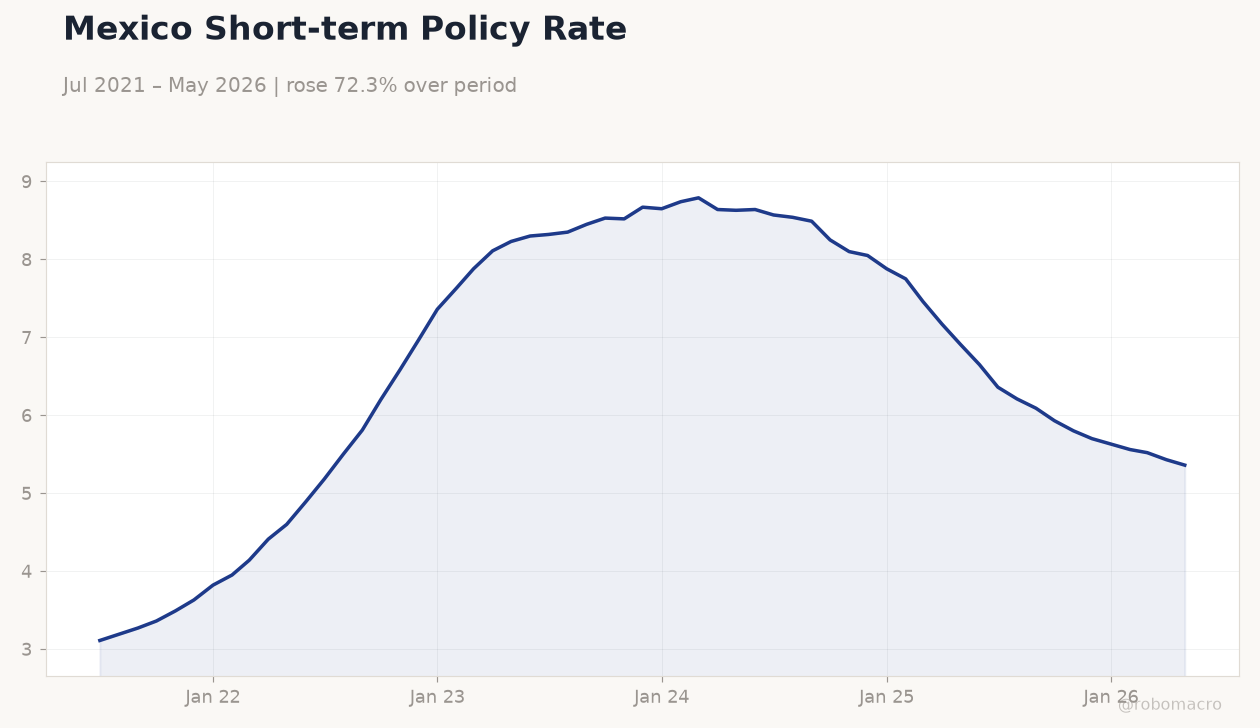

| Mexico Short-term Rate | 5.36% | -1.29% |

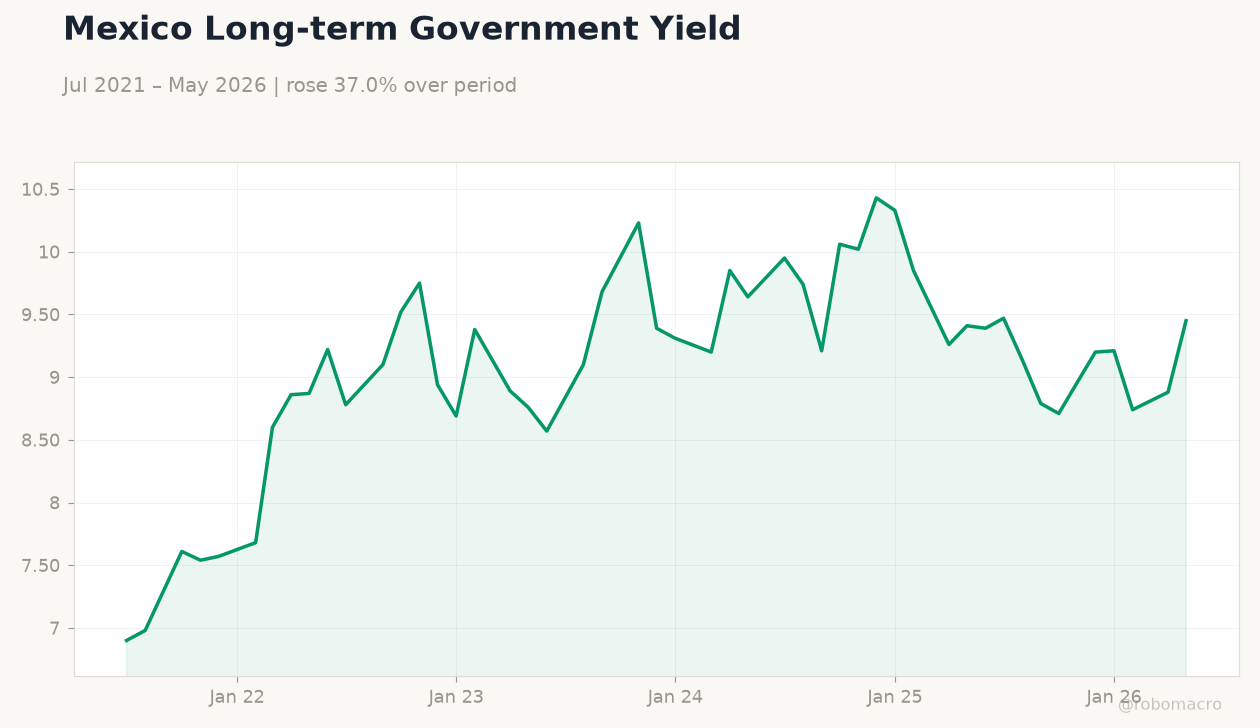

| Mexico Long-term Rate | 9.45% | +6.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Short-term Policy Rate | Type: macro_line | Short-term Rate (%): 5.36 (2026-05-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.36

Mexico Short-term Policy Rate | Type: macro_line | Short-term Rate (%): 5.36 (2026-05-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.36

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-07-01) | |||

| Business Confidence Index | 47.50 | - | 04:00 |

| Friday (2026-07-03) | |||

| Consumer Confidence Index | 43.50 | - | 04:00 |

- IPC Bolsa rises 0.62% to 67,640.59 while USD/MXN drops 0.26% to 17.46 on nearshoring inflows.

- Mexico short-term rate holds at 5.36% as long-term yields climb 6.42% to 9.45%.

- USMCA extension talks miss July 1 target, raising trade uncertainty for Mexican exports.

Yesterday's Recap

Mexico markets posted modest gains on June 29 with no major data releases. The IPC Bolsa advanced 0.62% to close at 67,640.59 amid continued foreign buying tied to industrial relocation projects. USD/MXN eased 0.26% to 17.46 while EUR/MXN fell 0.18% to 19.89, reflecting peso support from portfolio inflows.

WTI Crude rose 0.34% to 70.99 and Brent Crude gained 1.48% to 74.23, providing a mild tailwind for Mexican energy exports. Silver jumped 2.17% to 59.44 and gold added 0.56% to 4,045.00 on softer global risk sentiment. The short-term rate remained at 5.36% while the long-term rate surged 6.42% to 9.45%, steepening the curve.

Bitcoin fell 1.82% to 59,042.55 with limited spillover to local assets.

The Day Ahead

The calendar stays light through early July. Business Confidence Index prints at 04:00 ET on July 1, following the prior 47.5 reading. Consumer Confidence Index follows on July 3 after the last 43.5 print.

Both releases carry medium impact and will inform second-quarter domestic demand trends. Markets will also monitor any fresh statements on USMCA consultations ahead of the missed July 1 extension deadline. No Banxico speakers are scheduled.

Other Economic Notes

Private capital flows are accelerating via the strengthened Fund of Funds, targeting nearshoring and artificial intelligence projects. Industrial relocation continues to anchor foreign direct investment despite USMCA frictions. Remittance inflows remain supportive for household consumption and peso stability.

Energy-reform clarity has improved transmission participation rules without altering CFE offtake structures. These factors collectively sustain Mexico’s external financing position.

Global Macro News

USMCA renewal talks have stalled past the July 1 deadline, threatening tariff stability on Mexican manufactured goods. Broader global rate paths show mixed signals, with several emerging-market central banks facing currency pressure that could spill into MXN volatility. <i>↓ p.2</i>