Mexico Macro Daily(Beta Mode)

Business Confidence Rises as Peso Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 66,888.76 | -0.12% |

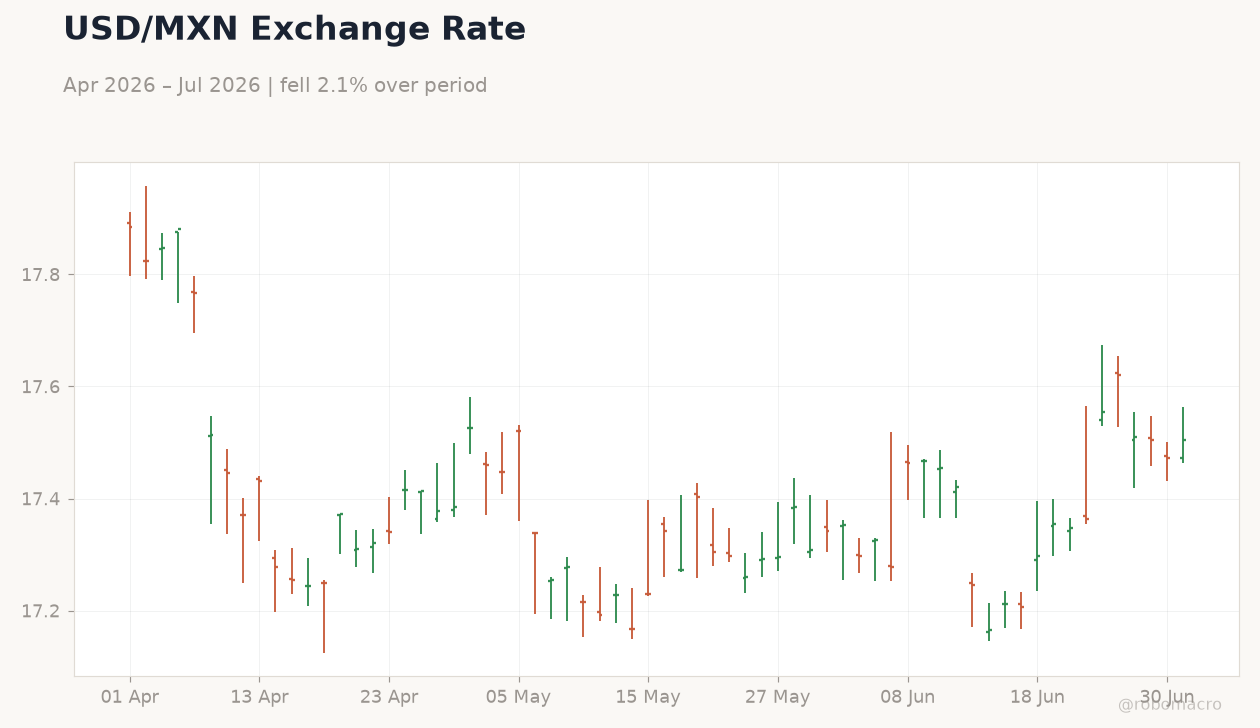

| USD/MXN | 17.51 | +0.22% |

| EUR/MXN | 19.95 | +0.11% |

| WTI Crude | 68.91 | -0.85% |

| Silver | 60.31 | +1.40% |

| Gold | 4,093.00 | +1.74% |

| Brent Crude | 71.99 | -1.28% |

| Bitcoin | 59,330.84 | +1.32% |

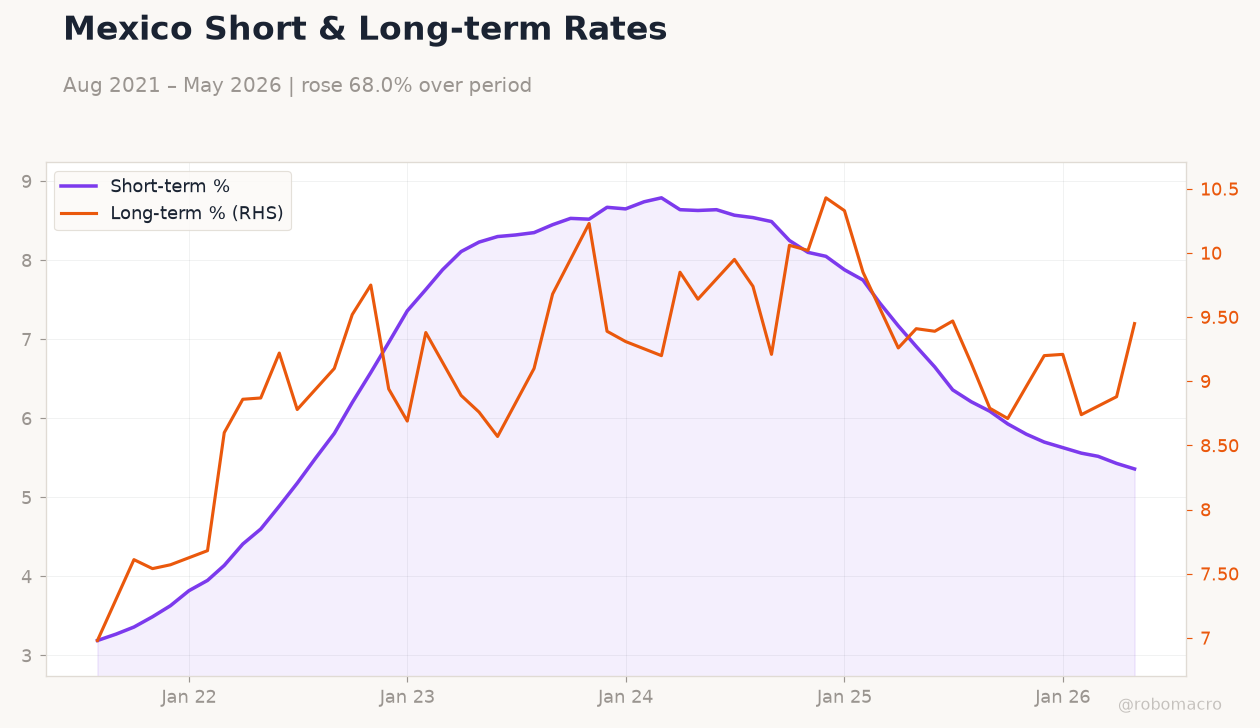

| Mexico Short-term Rate | 5.36% | -1.29% |

| Mexico Long-term Rate | 9.45% | +6.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

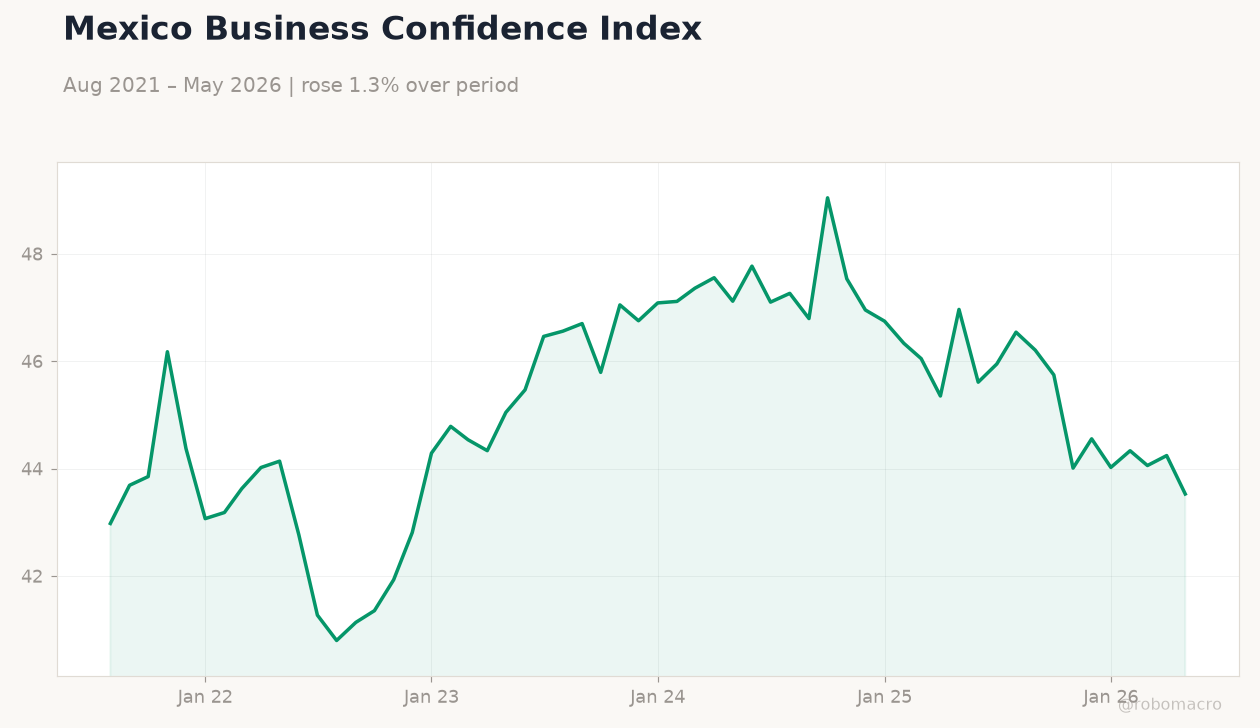

| Business Confidence Index | 47.50 | - | 48 |

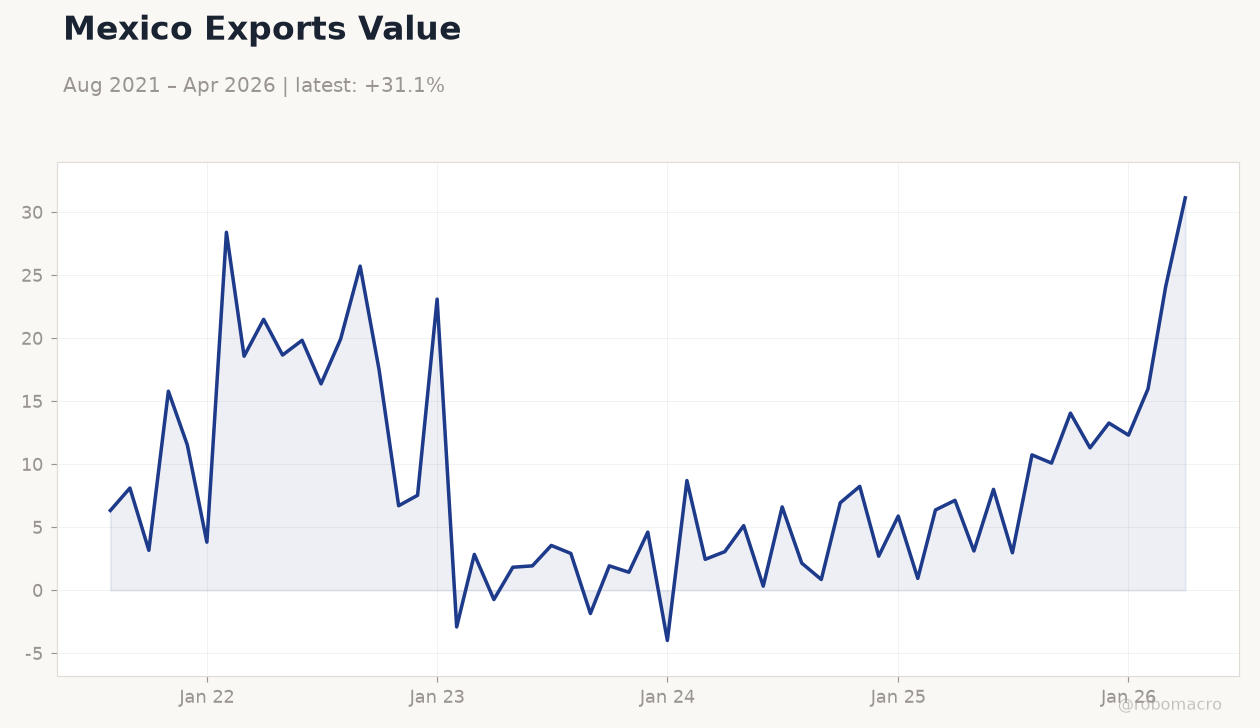

Mexico Exports Value | Type: macro_line | USD mn: 31.13 (2026-04-01) | Range: -3.988–31.13 | Trend(5pt): 6.328,17.5,4.612,0.937,31.13

Mexico Exports Value | Type: macro_line | USD mn: 31.13 (2026-04-01) | Range: -3.988–31.13 | Trend(5pt): 6.328,17.5,4.612,0.937,31.13

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-07-03) | |||

| Consumer Confidence Index | 43.50 | - | 04:00 |

- Mexico's Business Confidence Index rose to 48.0 in June from 47.5 prior, signaling modest improvement in corporate sentiment.

- USD/MXN climbed 0.22% to 17.51 while the IPC Bolsa slipped 0.12% to 66,888.76 amid mixed commodity moves.

- Mexico's short-term rate held at 5.36% as the long-term rate jumped 6.42% to 9.45%, steepening the curve.

Yesterday's Recap

Mexico reported a Business Confidence Index reading of 48.0 for June, up from 47.5 in the prior month and reflecting incremental gains in manufacturing and services outlooks. Equity markets closed lower with the IPC Bolsa declining 0.12% to 66,888.76 as foreign flows rotated toward higher-yielding assets elsewhere. The peso weakened modestly, sending USD/MXN 0.22% higher to 17.51 while EUR/MXN advanced 0.11% to 19.95.

Short-term Mexican rates eased 1.29% to 5.36%, but the long-term rate surged 6.42% to 9.45%, widening the spread and signaling investor caution on duration. WTI crude fell 0.85% to 68.91 and Brent dropped 1.28% to 71.99, weighing on energy-linked names within the index. Gold and silver posted strong gains of 1.74% and 1.40% respectively, providing limited support to precious-metals exposure in Mexican portfolios.

No Banxico speakers appeared and markets interpreted the data as neutral for near-term policy.

The Day Ahead

The next Mexican data point arrives on 3 July with the Consumer Confidence Index release, expected to show whether household sentiment has kept pace with the modest business improvement. Traders will monitor any revisions to June inflation prints and peso positioning ahead of the long weekend. USMCA review discussions continue in Washington with officials from all three nations assessing extension options before the July deadline passes without formal action.

Infrastructure financing talks between the Sheinbaum administration and BlackRock, KKR and Macquarie remain active, potentially unlocking new project pipelines later this quarter. No Banxico speakers are scheduled through the holiday period.

Other Economic Notes

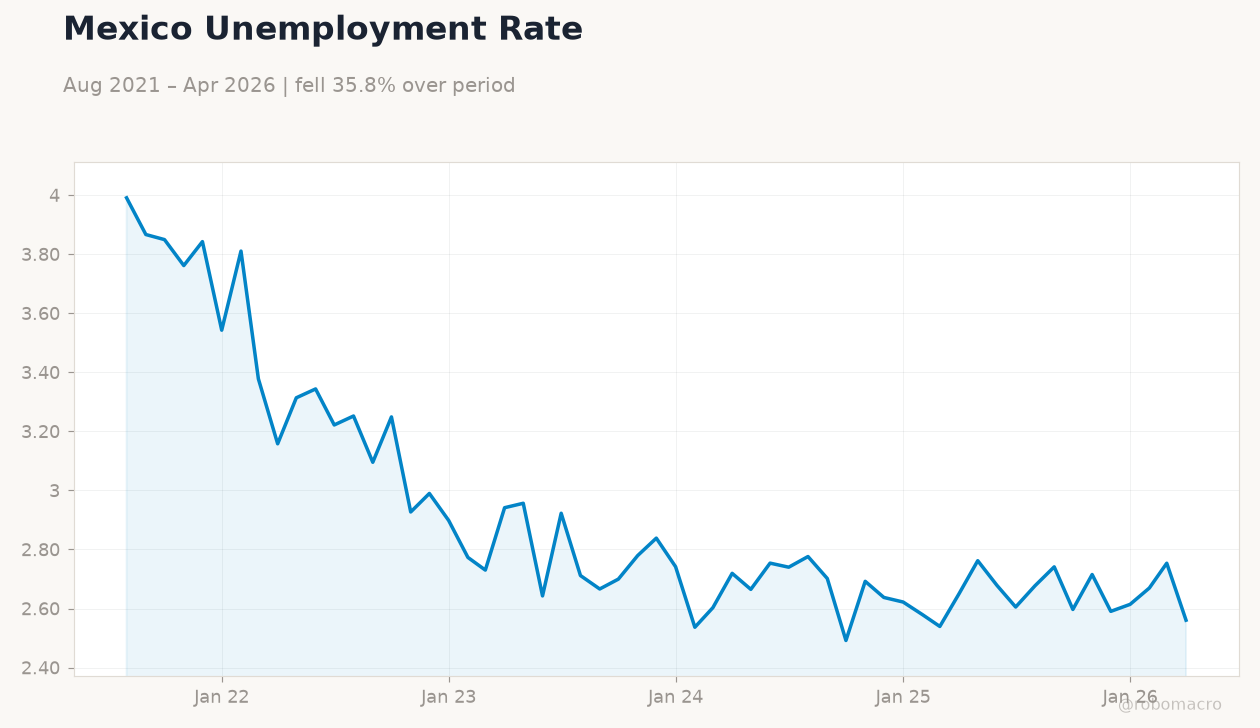

Nearshoring momentum persists with additional semiconductor suppliers expanding capacity in Chihuahua, supporting industrial output and formal employment. Remittances reached a fresh record of $6.1 billion in May, up 4.8% year-over-year and providing a steady current-account buffer. Energy-reform legislation remains stalled in Congress with little prospect of material progress before year-end.

<i>↓ p.2</i>