Mexico Macro Daily(Beta Mode)

Peso Rises on Firmer Business Sentiment

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 67,247.79 | +0.42% |

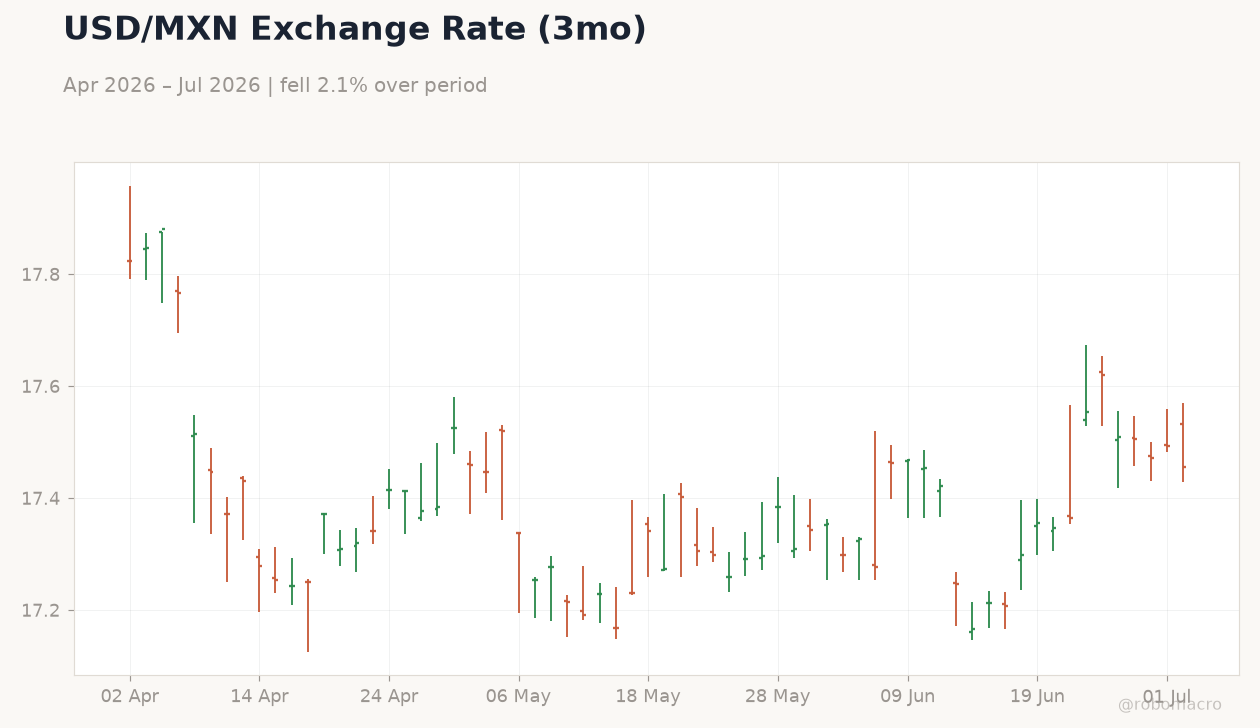

| USD/MXN | 17.45 | -0.22% |

| EUR/MXN | 19.98 | +0.08% |

| WTI Crude | 67.59 | -1.44% |

| Silver | 61.43 | +2.24% |

| Gold | 4,129.60 | +1.51% |

| Brent Crude | 70.61 | -1.34% |

| Bitcoin | 61,590.74 | +2.64% |

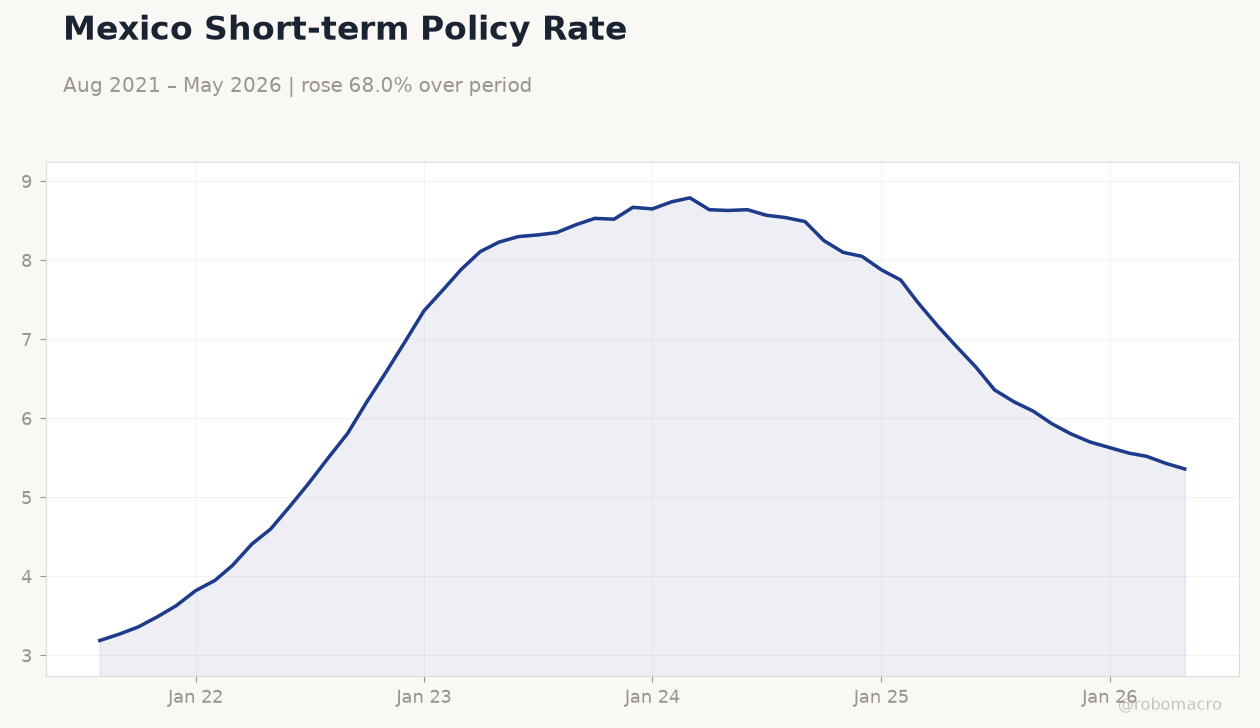

| Mexico Short-term Rate | 5.36% | -1.29% |

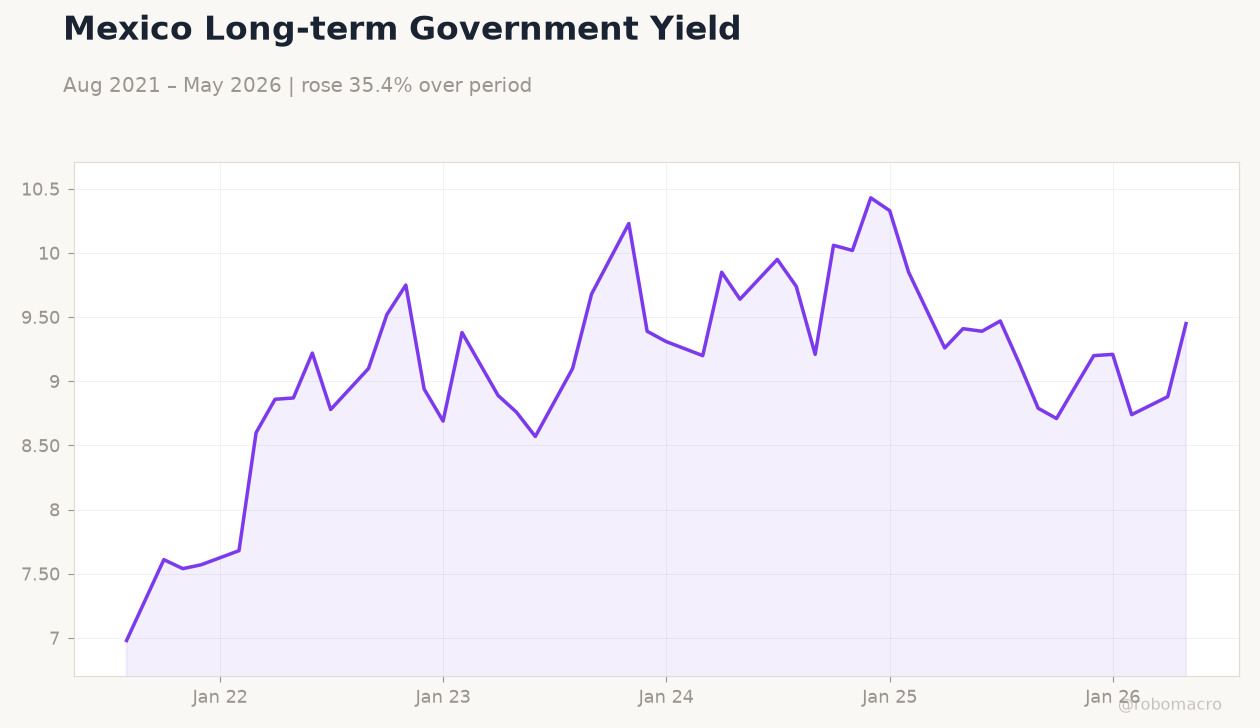

| Mexico Long-term Rate | 9.45% | +6.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

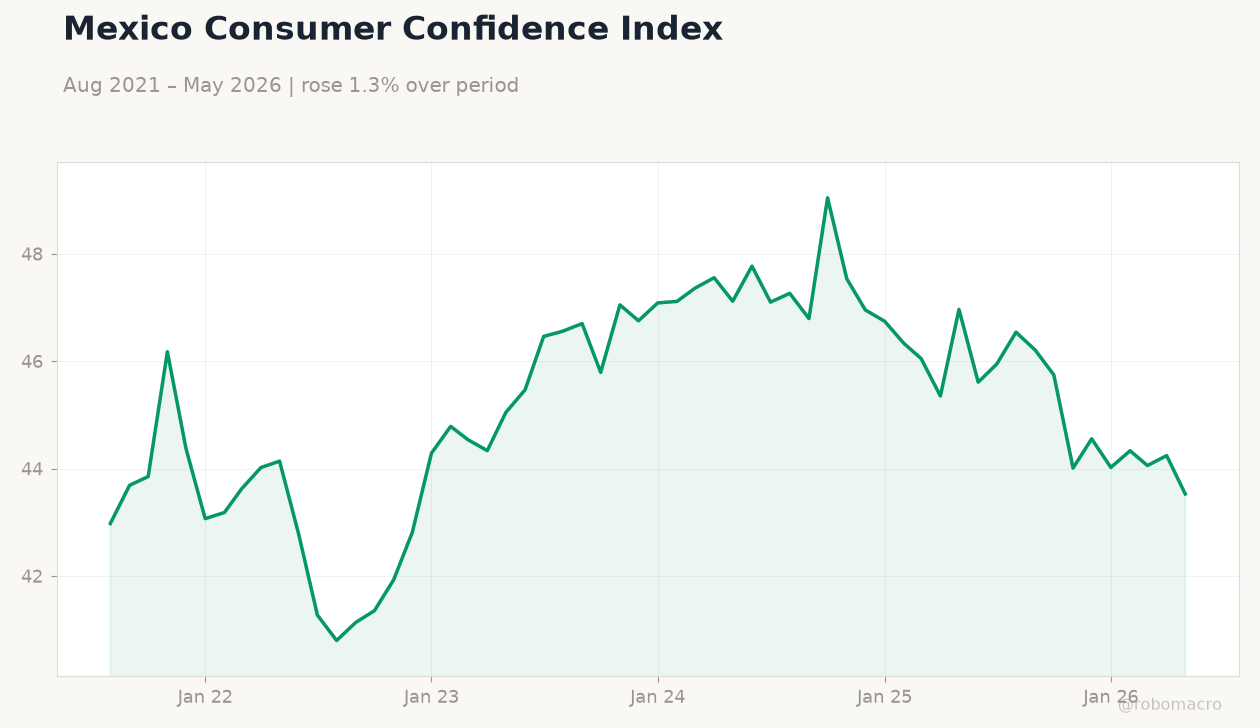

| Business Confidence Index | 47.50 | - | 48 |

Mexico Short-term Policy Rate | Type: macro_line | Percent: 5.36 (2026-05-01) | Range: 3.19–8.79 | Trend(6pt): 3.19,6.2,8.67,7.75,5.43,5.36

Mexico Short-term Policy Rate | Type: macro_line | Percent: 5.36 (2026-05-01) | Range: 3.19–8.79 | Trend(6pt): 3.19,6.2,8.67,7.75,5.43,5.36

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-07-03) | |||

| Consumer Confidence Index | 43.50 | - | 04:00 |

- Mexico's Business Confidence Index climbed to 48.0 in June from 47.5, signaling modest improvement in sentiment ahead of World Cup-related disruptions.

- USD/MXN fell 0.22% to 17.45 while IPC Bolsa gained 0.42% to 67,247.79, reflecting peso resilience amid softer U.S. rate expectations.

- Short-term Mexican rates held at 5.36% as officials courted BlackRock and KKR to revive stalled infrastructure projects.

Yesterday's Recap

Mexico's Business Confidence Index rose to 48.0 on July 1, beating the prior 47.5 reading and pointing to steady private-sector optimism. Equity markets responded positively, with IPC Bolsa advancing 0.42% to close at 67,247.79. The peso strengthened, driving USD/MXN down 0.22% to 17.45 despite heavy World Cup celebrations that claimed four lives in Mexico City.

Long-term yields jumped 6.42% to 9.45%, widening the curve as investors priced in fiscal spending needs. Nearshoring flows remained supportive, with automotive and infrastructure projects drawing fresh interest from global asset managers. Oil prices slipped, with WTI falling 1.44% to $67.59, trimming energy export revenues.

Overall, markets absorbed the social events without material volatility in currency or equities.

The Day Ahead

Consumer Confidence Index data are scheduled for release on July 3 at 04:00 ET, with the prior print at 43.5. Traders will monitor any spillover from yesterday's World Cup festivities into retail and services sentiment. Banxico officials are expected to maintain the 5.36% policy rate amid contained inflation pressures.

USMCA renewal talks continue to draw attention after the U.S. signaled annual reviews rather than multi-year extension. Market participants will also track silver and gold prices, which rose 2.24% and 1.51% respectively, for clues on safe-haven demand affecting the peso.

Other Economic Notes

President Sheinbaum's government met BlackRock, KKR and Macquarie to accelerate stalled infrastructure projects critical for nearshoring competitiveness. Fiscal authorities face pressure to fund these initiatives while keeping debt issuance in check. The widening long-term yield spread to 9.45% highlights investor concerns over spending plans versus revenue from energy exports.

Sustained peso strength at 17.45 supports import cost stability but may challenge manufacturing margins if it persists.