Mexico Macro Daily(Beta Mode)

Peso Gains as USMCA Renewal Stalls

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 67,135.06 | +0.10% |

| USD/MXN | 17.46 | -0.54% |

| EUR/MXN | 19.98 | +0.04% |

| WTI Crude | 68.88 | +0.28% |

| Silver | 62.69 | +3.38% |

| Gold | 4,176.00 | +1.54% |

| Brent Crude | 72.17 | +0.52% |

| Bitcoin | 61,769.30 | +0.46% |

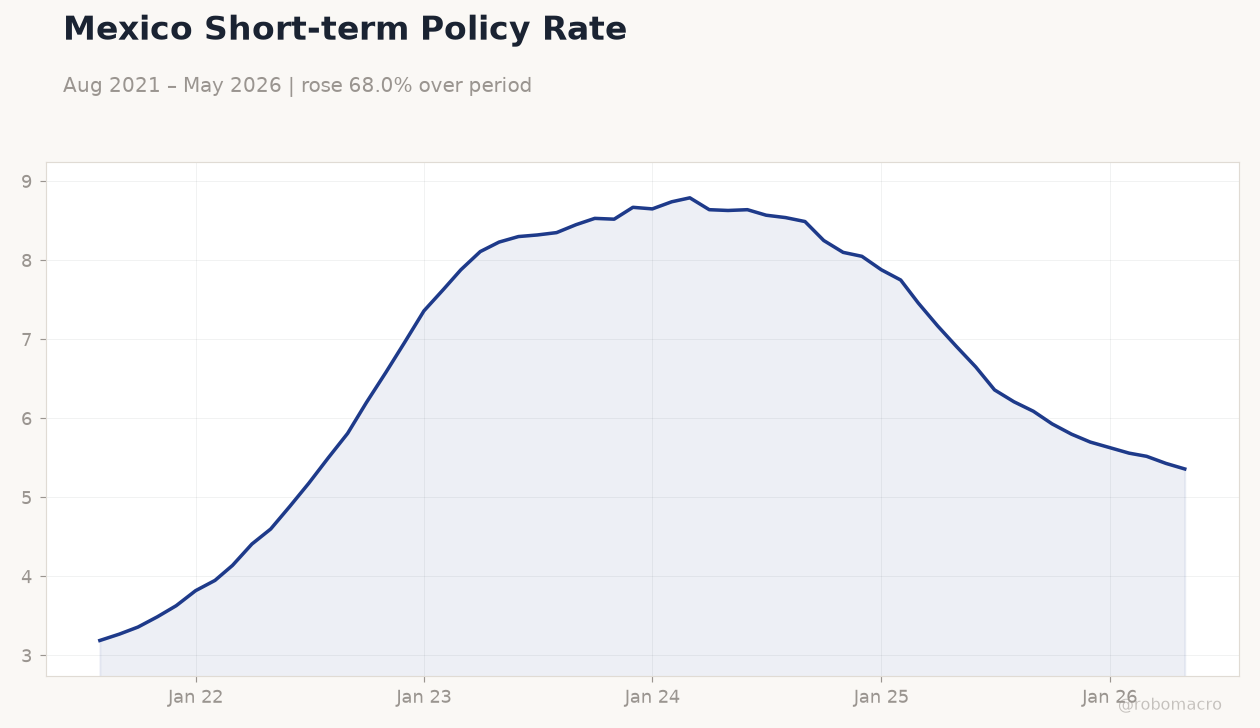

| Mexico Short-term Rate | 5.36% | -1.29% |

| Mexico Long-term Rate | 9.45% | +6.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Business Confidence Index | 47.50 | - | 48 |

| Consumer Confidence Index | 43.50 | - | 43.80 |

Mexico Short-term Policy Rate | Type: macro_line | Short-term Rate (%): 5.36 (2026-05-01) | Range: 3.19–8.79 | Trend(6pt): 3.19,6.2,8.67,7.75,5.43,5.36

Mexico Short-term Policy Rate | Type: macro_line | Short-term Rate (%): 5.36 (2026-05-01) | Range: 3.19–8.79 | Trend(6pt): 3.19,6.2,8.67,7.75,5.43,5.36

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Business Confidence Index rose to 48.0 in June while Consumer Confidence edged up to 43.8, both above prior readings.

- USD/MXN fell 0.54% to 17.46 as investors positioned for prolonged USMCA uncertainty.

- Mexico long-term rates jumped 6.42% to 9.45% while the short-term rate eased to 5.36%.

Yesterday's Recap

Mexico’s Business Confidence Index improved to 48.0 from 47.5, signaling modest resilience in manufacturing sentiment despite external trade pressure. Consumer Confidence ticked up to 43.8 from 43.5, reflecting stable household views ahead of the summer slowdown. The peso strengthened notably against the dollar, closing at 17.46 after a 0.54% gain as markets priced in delayed USMCA renewal.

IPC Bolsa advanced 0.10% to 67,135.06, supported by selective buying in export-oriented names. Long-term Mexican yields rose sharply to 9.45%, widening the spread over short-term rates that settled at 5.36%. WTI crude held near 68.88 while gold and silver posted gains that offered limited peso support.

Trade headlines dominated, with reports that US officials declined immediate USMCA renewal, prompting fresh nearshoring concerns.

The Day Ahead

No major Mexican data releases are scheduled for today or tomorrow, leaving markets to digest ongoing USMCA developments. Investors will monitor any statements from Mexican trade officials seeking alternative solutions with Canada. Peso flows may remain sensitive to US commentary on automotive rules of origin and potential Chinese investment screening.

Equity participants are expected to focus on IPC constituents with heavy US exposure. Rate markets will watch for any shifts in long-term yield direction after yesterday’s steep move.

Other Economic Notes

Mexico’s export-led model faces renewed scrutiny as annual USMCA reviews gain prominence in Washington. Nearshoring inflows remain at risk if stricter origin rules or investment reviews are adopted. The combination of firmer confidence readings and rising long-term yields points to a market balancing domestic resilience against external policy threats.

Silver and gold strength offered some commodity-linked currency support but did not offset trade-related peso volatility.