Nordics Macro Daily(Beta Mode)

Nordic Stocks Slide, Brent Drops

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 2,863.92 | -0.90% |

| Oslo Bors | 1,981.56 | -0.33% |

| OMX Copenhagen 25 | 1,638.13 | -1.46% |

| OMX Helsinki 25 | 5,763.57 | -2.05% |

| USD/SEK | 9.46 | +0.36% |

| USD/NOK | 9.69 | +0.11% |

| EUR/SEK | 10.89 | +0.17% |

| EUR/NOK | 11.21 | +0.24% |

| Brent Crude | 107.94 | -4.11% |

| Gold | 4,524.60 | +0.73% |

| Bitcoin | 67,588.58 | +1.91% |

| Sweden 10Y Govt Yield | 2.64% | -5.73% |

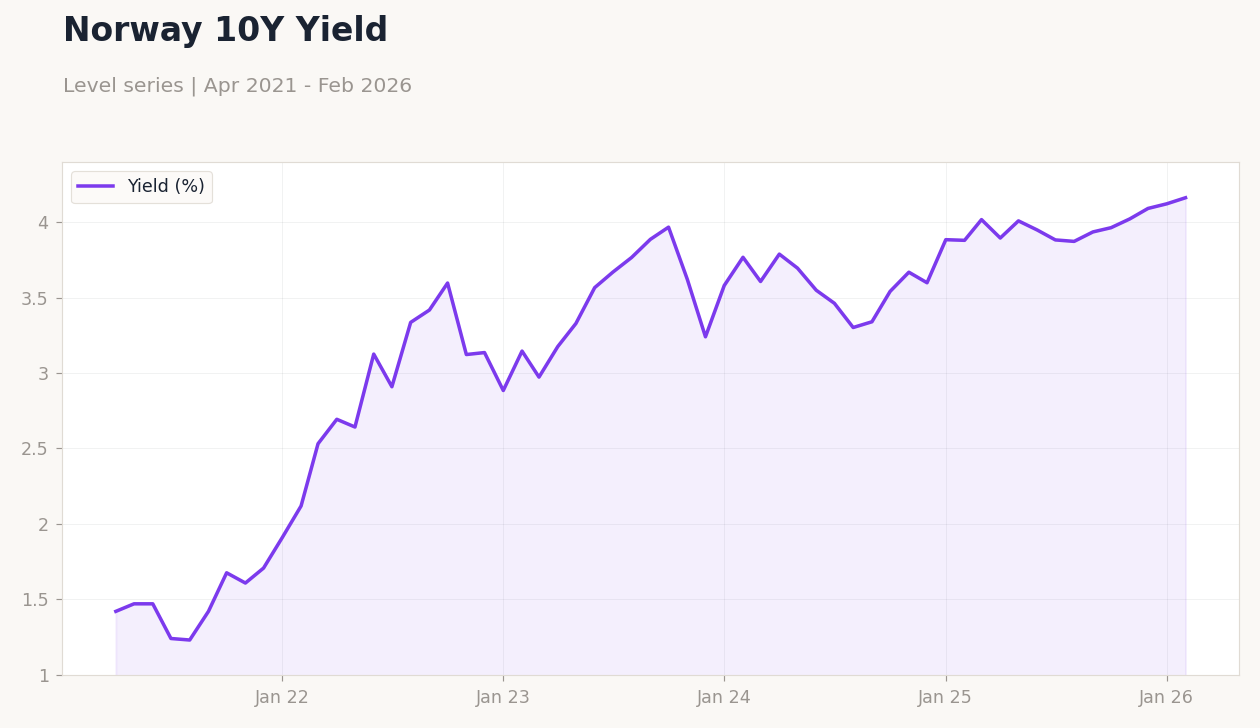

| Norway 10Y Govt Yield | 4.16% | +0.98% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

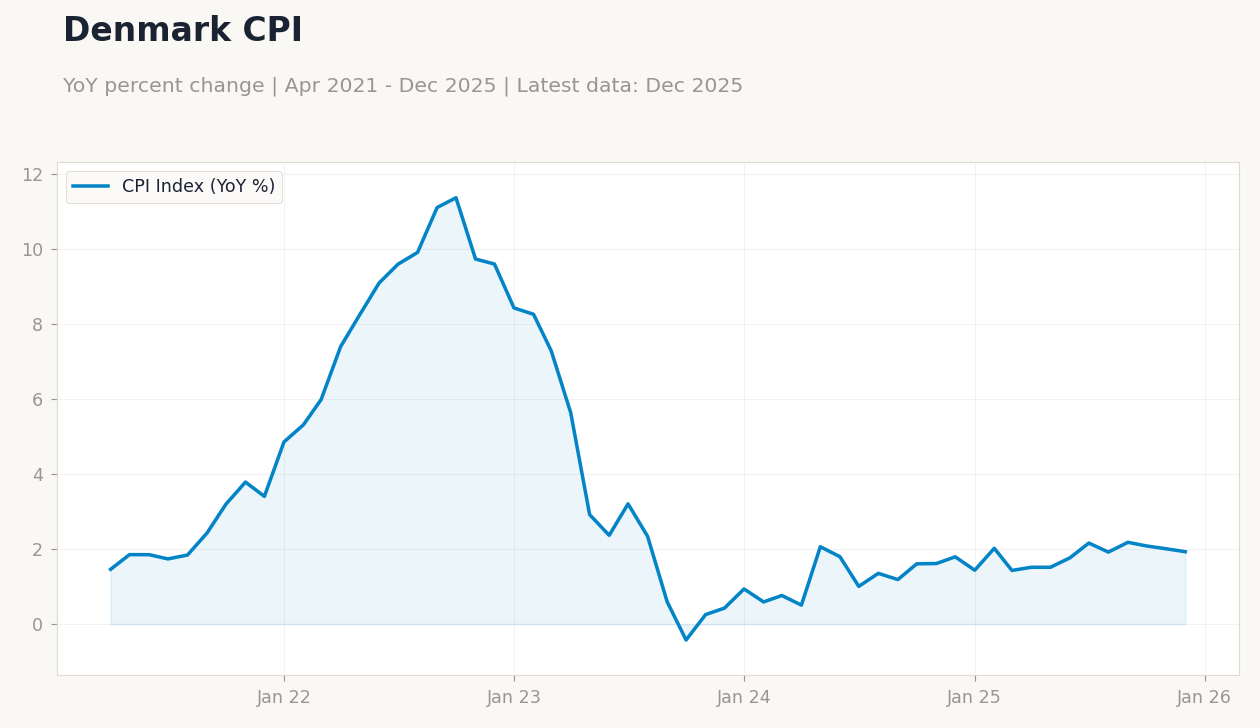

Brent vs Norway CPI | Type: macro_line | Brent Price ($): 17.16 (2026-03-23) | Range: -21.02–52.89 | Trend(6pt): -7.648,-5.948,5.578,-1.995,45.19,17.16

Brent vs Norway CPI | Type: macro_line | Brent Price ($): 17.16 (2026-03-23) | Range: -21.02–52.89 | Trend(6pt): -7.648,-5.948,5.578,-1.995,45.19,17.16

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Nordic equities declined amid falling oil prices, with Finland's OMX Helsinki 25 down 2.05% and Denmark's OMX Copenhagen 25 off 1.46%.

- Brent crude fell 4.11% to $107.94, pressuring Norway's fiscal outlook, while Sweden's 10Y yield dropped 5.73% to 2.64%.

- Currencies mixed: USD/SEK up 0.36% to 9.46, USD/NOK rose 0.11% to 9.69, reflecting cautious market sentiment.

Yesterday's Recap

Nordic markets closed lower on March 29, with Sweden's OMX Stockholm 30 falling 0.90% to 2,863.92 amid broader risk-off sentiment. Norway's Oslo Bors index dipped 0.33% to 1,981.56, weighed down by energy sector weakness as Brent crude tumbled 4.11%. Denmark's OMX Copenhagen 25 declined 1.46% to 1,638.13, reflecting export-oriented manufacturing concerns.

Finland's OMX Helsinki 25 saw the steepest drop at 2.05% to 5,763.57, pressured by eurozone ties and global slowdown fears. Sweden's government proposed temporary fuel tax cuts to mitigate inflationary pressures from the Iran war, supporting voter sentiment ahead of elections. Currency moves were modest, with USD/SEK strengthening 0.36% and USD/NOK up 0.11%, while bond yields diverged: Sweden's 10Y fell sharply by 5.73% to 2.64%, signaling easing expectations, versus Norway's 10Y rising 0.98% to 4.16%.

No major data releases occurred across the bloc, keeping focus on market dynamics.

The Day Ahead

March 30 brings a quiet calendar for Nordic macro data, with no scheduled releases from Sweden, Norway, Denmark, or Finland. Investors will monitor any follow-up announcements on Sweden's proposed fuel tax reductions, which could influence inflation expectations. Attention may shift to global oil price movements, given Norway's exposure as an exporter.

In Finland, eurozone-aligned indicators could indirectly affect sentiment via ECB channels. Broader market trading is expected to remain cautious ahead of potential end-of-quarter adjustments. No central bank events are slated, allowing focus on currency and equity flows.

Other Economic Notes

Sweden's housing market remains a key watchpoint, with recent price stability amid high interest rates, though the fuel tax cut proposal could ease household burdens and support consumption. Norway's oil-dependent economy faces headwinds from Brent's decline, potentially trimming petroleum fund inflows and pressuring the krone. Broader Nordic trade dynamics show resilience in manufacturing exports, but Denmark and Finland grapple with euro peg and ECB policy constraints amid global slowdown risks.