Nordics Macro Daily(Beta Mode)

Nordics Mixed on Oil, Bond Moves

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,079.31 | -0.48% |

| Oslo Bors | 2,060.64 | +1.86% |

| OMX Copenhagen 25 | 1,732.46 | +0.04% |

| OMX Helsinki 25 | 6,164.37 | -0.01% |

| USD/SEK | 9.29 | -0.28% |

| USD/NOK | 9.49 | -0.80% |

| EUR/SEK | 10.86 | +0.01% |

| EUR/NOK | 11.09 | -0.57% |

| Brent Crude | 96.53 | +0.64% |

| Gold | 4,782.70 | -0.20% |

| Bitcoin | 72,145.55 | +1.44% |

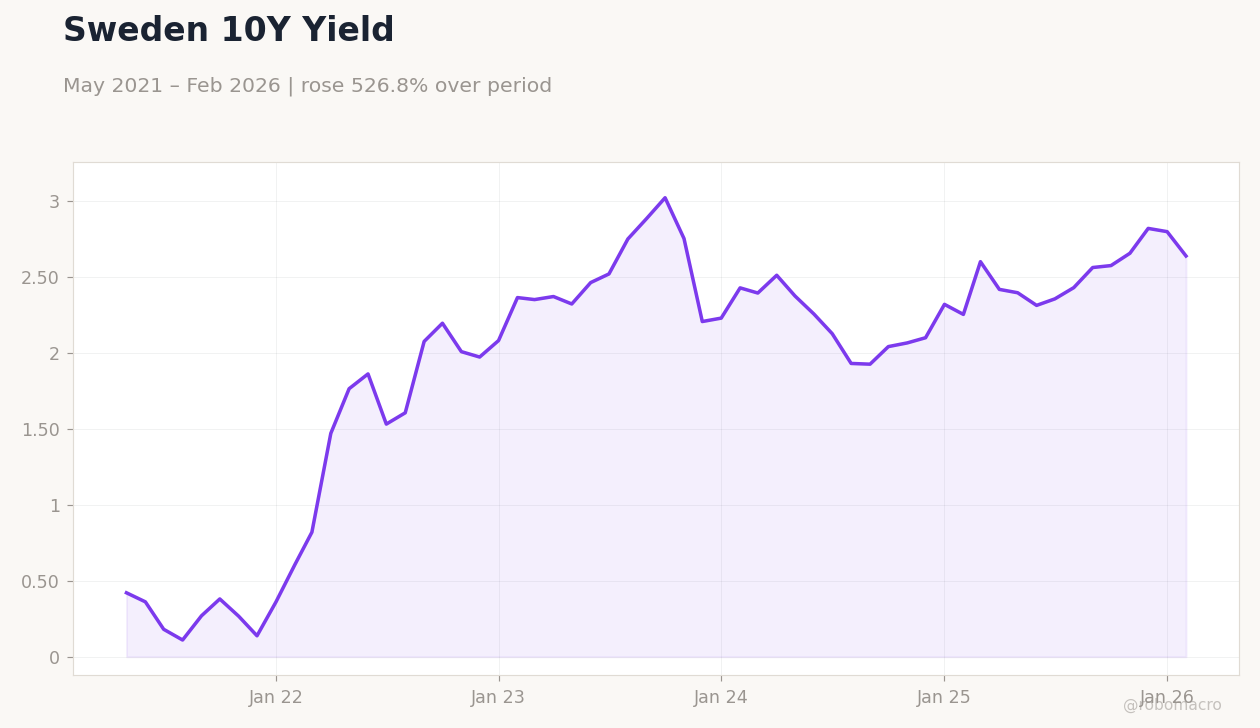

| Sweden 10Y Govt Yield | 2.64% | -5.73% |

| Norway 10Y Govt Yield | 4.16% | +0.98% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Norway 10Y Yield | Type: macro_line | Norway 10Y Yield (%): 4.162 (2026-02-01) | Range: 1.23–4.162 | Trend(6pt): 1.47,2.909,3.887,3.669,4.122,4.162

Norway 10Y Yield | Type: macro_line | Norway 10Y Yield (%): 4.162 (2026-02-01) | Range: 1.23–4.162 | Trend(6pt): 1.47,2.909,3.887,3.669,4.122,4.162

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Nordic equities diverged, with Oslo Børs up on Brent gains while Stockholm fell amid bond yield drop.

- Riksbank likely to hold rates steady despite soft Swedish CPI, aiding SEK.

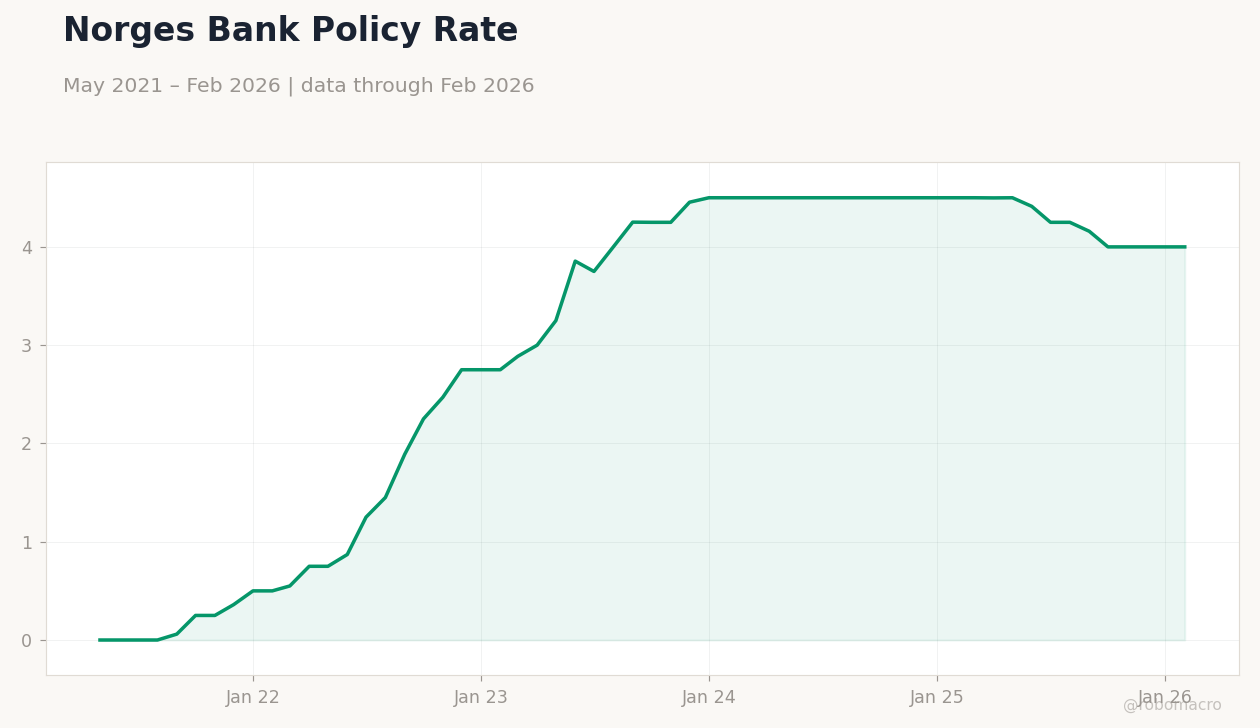

- Norges Bank policy risks pressure NOK amid global stagflation concerns.

Yesterday's Recap

Nordic markets showed mixed results on April 9, with the OMX Stockholm 30 down 0.48% to 3,079.31, weighed by risk aversion despite a bond rally where the Sweden 10Y government yield dropped 5.73% to 2.64%. Conversely, Oslo Børs rose 1.86% to 2,060.64, supported by Brent crude at $96.53 (+0.64%), boosting Norway's energy sector. OMX Copenhagen 25 inched up 0.04% to 1,732.46, indicating steady manufacturing sentiment, while OMX Helsinki 25 slipped 0.01% to 6,164.37 due to eurozone linkages.

Currencies leaned toward krona strength, with USD/SEK off 0.28% to 9.29 and USD/NOK down 0.80% to 9.49 on dollar softness. EUR/SEK was flat at 10.86 (+0.01%), but EUR/NOK fell 0.57% to 11.09, reflecting NOK's oil sensitivity. No key data emerged, though recent Swedish CPI softness lingered in bond pricing.

The day highlighted policy contrasts, with Sweden's disinflation backing dovish views and Norway's oil buffer aiding resilience.

The Day Ahead

April 10 lacks scheduled releases, directing focus to central bank remarks, especially Norges Bank on krone risks tied to oil volatility. Riksbank may offer insights post-soft CPI, shaping rate outlooks. Denmark's EUR/DKK peg via Danmarks Nationalbank could see subtle FX adjustments for stability.

Finland, aligned with ECB, might react to eurozone cues, with traders watching EU indicators. Informal Nordic housing or trade updates could sway equities. A light calendar emphasizes global sentiment influencing FX and bonds.

Other Economic Notes

Nordic exports demonstrate strength, with Sweden and Denmark gaining from manufacturing upticks in global demand, though Finland contends with eurozone issues including unemployment at 6.70% as of January 2023. Norway's oil economy benefits from Brent at $96.53, aiding fiscal health and krone support despite risks. Swedish housing shows early recovery from lower yields, but regional affordability hurdles remain.

Global Macro News

Stagflation worries grow globally, with U.S. reports citing low growth and high inflation, potentially hitting Nordic exports. Japan's BoJ official rejected stagflation, upholding steady policy that may steady Asian trade for Nordic firms.

(cont...)