Nordics Macro Daily(Beta Mode)

Norway's Oil Exports Hit Record

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,118.41 | -0.41% |

| Oslo Bors | 2,019.49 | -0.66% |

| OMX Copenhagen 25 | 1,774.28 | +0.40% |

| OMX Helsinki 25 | 6,214.27 | -1.09% |

| USD/SEK | 9.15 | -0.27% |

| USD/NOK | 9.38 | -0.61% |

| EUR/SEK | 10.82 | +0.20% |

| EUR/NOK | 11.07 | -0.58% |

| Brent Crude | 94.98 | +0.05% |

| Gold | 4,844.60 | +0.93% |

| Bitcoin | 75,009.19 | +0.27% |

| Sweden 10Y Govt Yield | 2.76% | +4.55% |

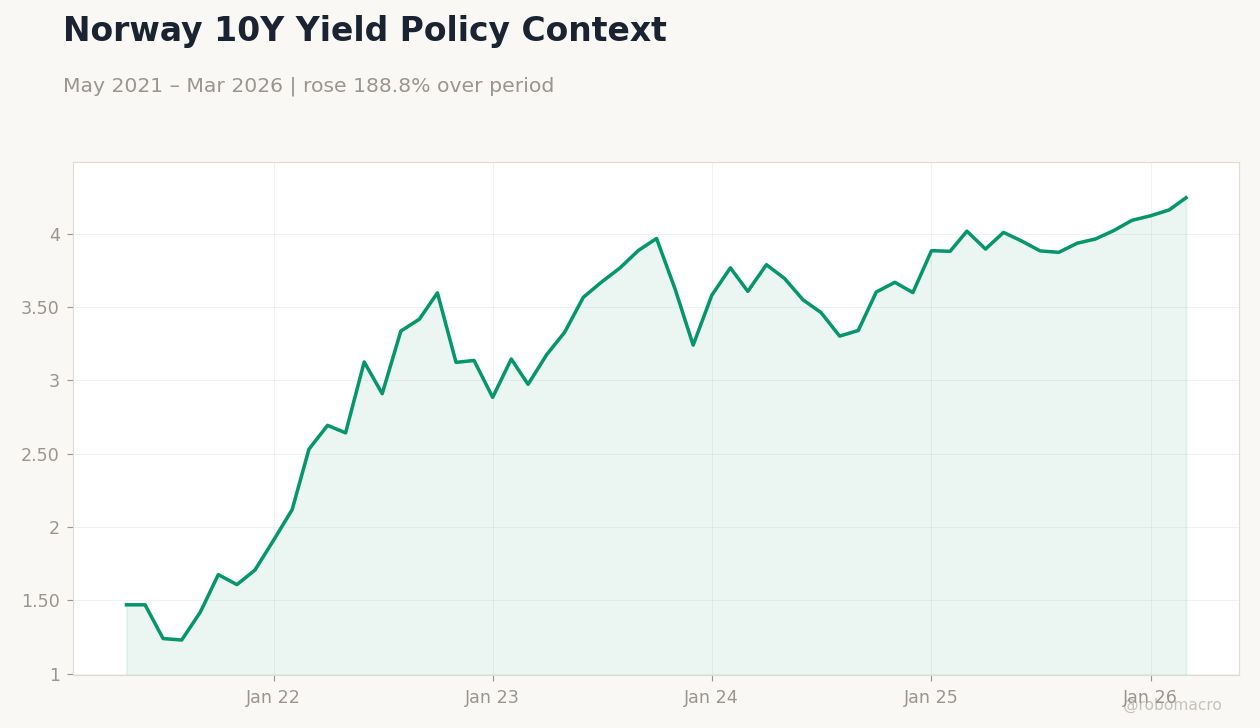

| Norway 10Y Govt Yield | 4.25% | +1.99% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Sweden 10Y Yield vs CPI | Type: macro_line | Sweden 10Y Yield %: 2.76 (2026-03-01) | Range: 0.1101–3.024 | Trend(6pt): 0.4212,1.533,2.888,2.067,2.8,2.76

Sweden 10Y Yield vs CPI | Type: macro_line | Sweden 10Y Yield %: 2.76 (2026-03-01) | Range: 0.1101–3.024 | Trend(6pt): 0.4212,1.533,2.888,2.067,2.8,2.76

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Norway's crude exports reached all-time high amid Iran war-driven price surge, boosting fiscal outlook.

- Swedish unemployment dips, equities mixed across Nordics with Finland lagging.

- Global risks rise as UK growth surprises, oil steady near $95/bbl.

Yesterday's Recap

Nordic markets displayed mixed performance amid stable oil prices and limited data flow, with the OMX Stockholm 30 closing at 3,118.41 after a -0.41% drop, pressured by broader risk aversion. Oslo Bors fell -0.66% to 2,019.49, despite Norway's record-high crude exports in March fueled by the Iran war and Strait of Hormuz disruptions, which propelled export values to unprecedented levels per SSB data. OMX Copenhagen 25 bucked the trend with a +0.40% gain to 1,774.28, supported by export-oriented firms, while OMX Helsinki 25 declined -1.09% to 6,214.27 on weak sentiment in tech and manufacturing sectors.

In Sweden, unemployment fell notably, providing a positive labor market signal amid coalition government criticism from the Council on Legislation. Currencies weakened against the USD, with USD/SEK at 9.15 (-0.27%) and USD/NOK at 9.38 (-0.61%), reflecting oil dynamics and global caution. Brent crude held steady at 94.98 (+0.05%), aiding Norway's trade surplus but offering little lift to regional equities.

No major data releases occurred across Denmark or Finland, though Sweden's heating plant faced an attempted pro-Russian attack, highlighting geopolitical vulnerabilities.

The Day Ahead

The Nordic calendar remains light with no scheduled data releases or events for Sweden, Norway, Denmark, or Finland, allowing markets to digest recent oil export highs and global developments. Attention may shift to potential commentary from Riksbank officials on inflation trends, given Sweden's improving unemployment figures. In Norway, traders will monitor any updates on oil production amid the Iran conflict's impact on Brent prices.

Denmark's Nationalbank could see minor FX interventions to maintain the EUR/DKK peg if euro volatility persists. Finland, under ECB oversight, might react to broader eurozone signals, though no local prints are due. Overall, expect quiet trading unless global macro news, such as US Treasury growth forecasts, influences sentiment.

Other Economic Notes

Broader economic themes in the Nordics emphasize resilience amid geopolitical tensions, with Norway benefiting from elevated oil prices due to the Iran war, potentially trimming fiscal deficits. Sweden's export-oriented manufacturing faces headwinds from bond market volatility, as seen in UK parallels, which could raise borrowing costs and slow investment. (cont...)