Nordics Macro Daily(Beta Mode)

Nordic Stocks Dip as Brent Slumps

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,101.08 | -0.97% |

| Oslo Bors | 1,994.27 | -0.48% |

| OMX Copenhagen 25 | 1,732.91 | +0.05% |

| OMX Helsinki 25 | 6,227.83 | -1.37% |

| USD/SEK | 9.26 | +0.59% |

| USD/NOK | 9.30 | -0.32% |

| EUR/SEK | 10.81 | -0.09% |

| EUR/NOK | 10.90 | +0.00% |

| Brent Crude | 101.06 | -4.05% |

| Gold | 4,735.20 | +0.27% |

| Bitcoin | 77,665.09 | +0.07% |

| Sweden 10Y Govt Yield | 2.76% | +4.55% |

| Norway 10Y Govt Yield | 4.25% | +1.99% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

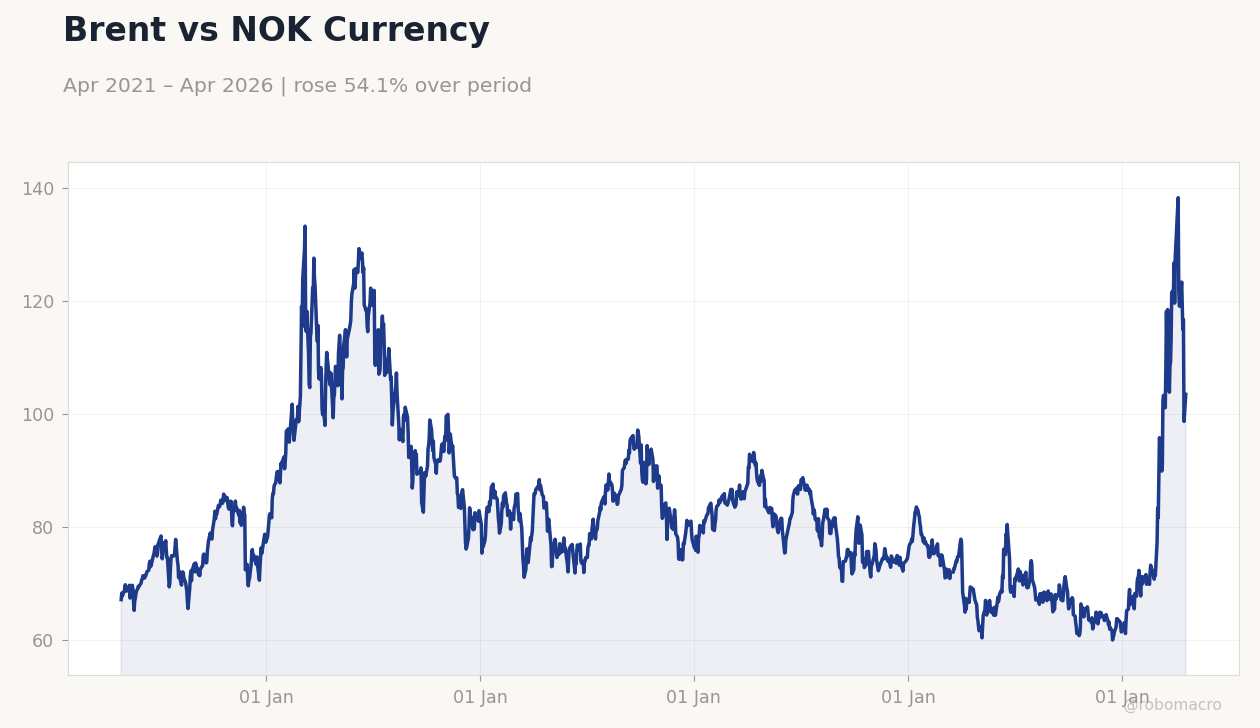

Brent vs NOK Currency | Type: macro_line | Brent USD/bbl: 103.4 (2026-04-20) | Range: 59.93–138.2 | Trend(6pt): 67.08,108.2,91.88,81.68,98.63,103.4

Brent vs NOK Currency | Type: macro_line | Brent USD/bbl: 103.4 (2026-04-20) | Range: 59.93–138.2 | Trend(6pt): 67.08,108.2,91.88,81.68,98.63,103.4

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Nordic equities declined amid falling oil prices, with Finland's OMX Helsinki 25 dropping 1.37% and Sweden's OMX Stockholm 30 down 0.97%.

- Brent crude slumped 4.05% to $101.06, pressuring Norway's export-dependent economy and weakening the NOK slightly.

- Government bond yields rose, with Sweden's 10Y up 4.55% to 2.76%, reflecting broader market caution on inflation risks.

Yesterday's Recap

Nordic markets closed lower on April 26, driven by a sharp drop in Brent crude prices that hit Norway hardest as an oil exporter. Sweden's OMX Stockholm 30 fell 0.97% to 3,101.08, weighed down by export sectors sensitive to global demand slowdowns, while the USD/SEK rose 0.59% to 9.26 amid krona weakness. Norway's Oslo Bors index dipped 0.48% to 1,994.27, reflecting oil price pressures, though the USD/NOK eased 0.32% to 9.30 on minor krone resilience.

Denmark's OMX Copenhagen 25 edged up marginally by 0.05% to 1,732.91, bucking the trend with gains in defensive stocks, supported by the EUR/DKK peg stability. Finland's OMX Helsinki 25 declined 1.37% to 6,227.83, impacted by eurozone contraction signals and supply chain issues. No major macro data releases occurred across the Nordics, leaving markets to react to global commodity shifts and broader economic uncertainty.

Bond markets saw yields climb, with Norway's 10Y up 1.99% to 4.25%, signaling investor concerns over persistent inflation.

The Day Ahead

April 27 brings a quiet calendar for Nordic macro releases, with no scheduled data from Sweden, Norway, Denmark, or Finland, allowing focus on global influences like oil market volatility. Investors will monitor any updates on Middle East tensions, given Norway's oil exposure and potential spillover to Swedish and Danish export chains. In Finland, as part of the eurozone, attention turns to ECB-related commentary amid ongoing supply disruptions.

Broader Nordic events could include corporate earnings from key firms in Stockholm and Oslo, potentially driving equity moves. Expect currency traders to watch EUR/SEK and EUR/NOK for peg-related stability in Denmark. Overall, the day may see subdued trading unless external shocks emerge.

Other Economic Notes

Broader Nordic themes highlight resilience in export-oriented manufacturing for Sweden and Denmark, though global supply chain disruptions pose risks to growth. Norway's fiscal outlook benefits from high oil revenues but faces headwinds from Brent's recent decline, impacting the sovereign wealth fund's inflows. Finland contends with eurozone contraction, with unemployment at 6.70% adding pressure on domestic demand.