Nordics Macro Daily(Beta Mode)

Nordic Stocks Mixed, Brent Plunges

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,079.76 | -0.69% |

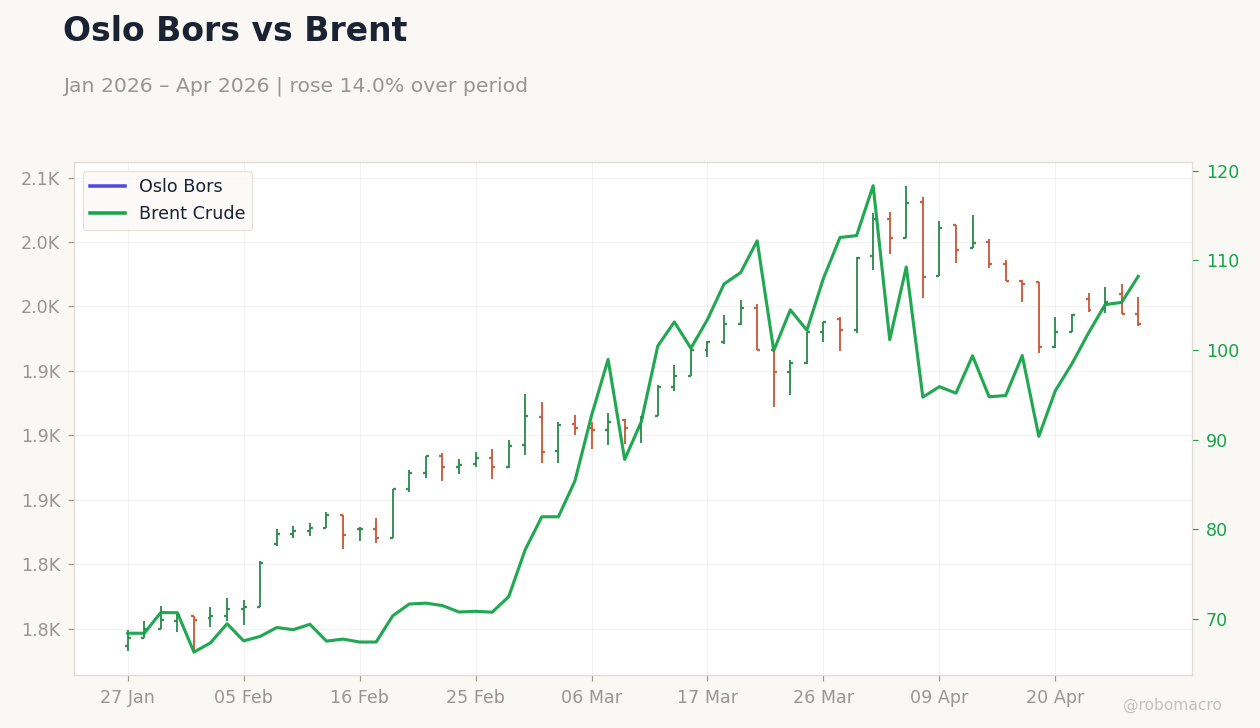

| Oslo Bors | 1,986.63 | -0.38% |

| OMX Copenhagen 25 | 1,736.06 | +0.18% |

| OMX Helsinki 25 | 6,239.09 | +0.18% |

| USD/SEK | 9.24 | -0.16% |

| USD/NOK | 9.31 | +0.28% |

| EUR/SEK | 10.83 | +0.14% |

| EUR/NOK | 10.90 | +0.15% |

| Brent Crude | 102.69 | -5.12% |

| Gold | 4,672.00 | -0.07% |

| Bitcoin | 76,888.25 | -2.25% |

| Sweden 10Y Govt Yield | 2.76% | +4.55% |

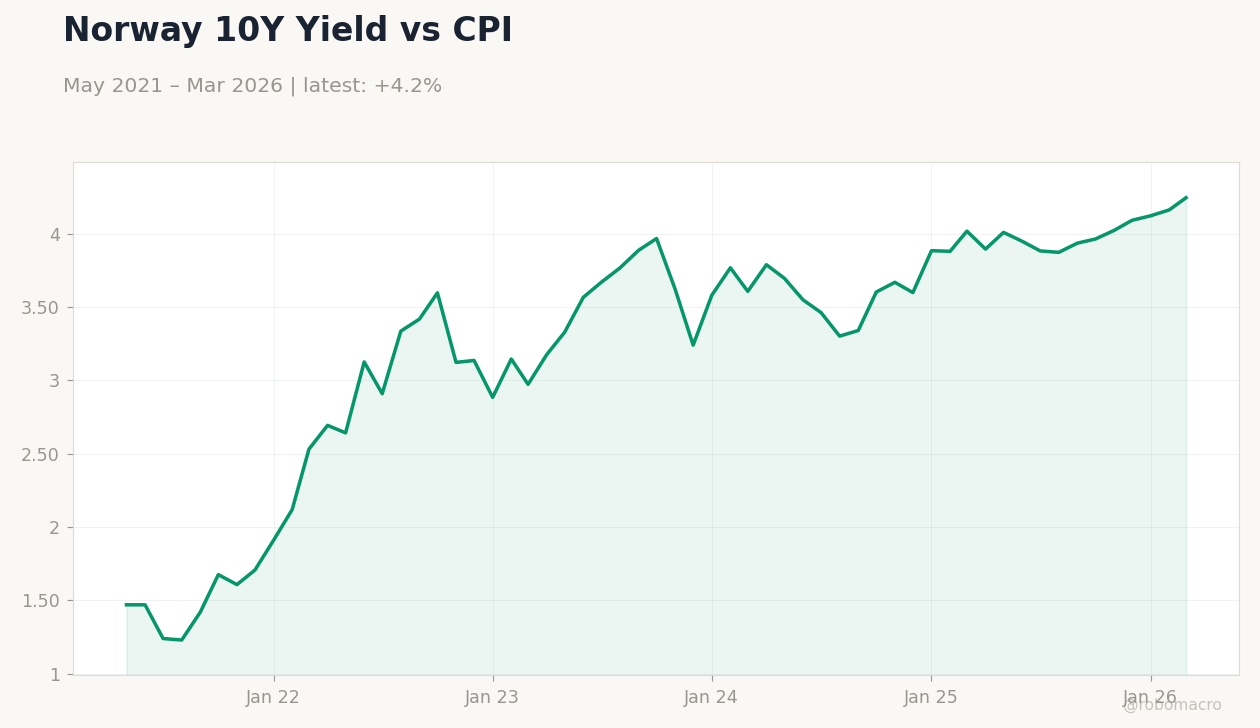

| Norway 10Y Govt Yield | 4.25% | +1.99% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Sweden 10Y Yield vs CPI | Type: macro_line | Sweden 10Y Yield %: 2.76 (2026-03-01) | Range: 0.1101–3.024 | Trend(6pt): 0.4212,1.533,2.888,2.067,2.8,2.76

Sweden 10Y Yield vs CPI | Type: macro_line | Sweden 10Y Yield %: 2.76 (2026-03-01) | Range: 0.1101–3.024 | Trend(6pt): 0.4212,1.533,2.888,2.067,2.8,2.76

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Nordic equities displayed mixed results, with Sweden and Norway declining amid Brent crude's sharp fall, while Denmark and Finland saw slight gains.

- Currencies showed modest shifts, with SEK strengthening slightly against USD and NOK weakening, alongside rising bond yields reflecting inflation worries.

- Global oil shocks and geopolitical tensions weighed on energy-dependent Nordic economies, amplifying risks to inflation and exports.

Yesterday's Recap

Nordic markets ended mixed on April 27, as falling oil prices pressured energy-exposed sectors. Sweden's OMX Stockholm 30 dropped 0.69% to 3,079.76, driven by risk aversion linked to commodity weakness. Norway's Oslo Bors fell 0.38% to 1,986.63, hit by Brent crude's 5.12% decline to 102.69, which strained oil stocks and revenue expectations.

Denmark's OMX Copenhagen 25 increased 0.18% to 1,736.06, aided by resilient exports despite global volatility. Finland's OMX Helsinki 25 rose 0.18% to 6,239.09, supported by eurozone connections and stable ECB policy. Currency movements were limited: USD/SEK decreased 0.16% to 9.24, USD/NOK rose 0.28% to 9.31, EUR/SEK climbed 0.14% to 10.83, and EUR/NOK advanced 0.15% to 10.90.

Bond yields rose, with Sweden's 10Y government yield up 4.55% to 2.76% and Norway's up 1.99% to 4.25%, indicating persistent inflation signals. Commodities weakened broadly: Gold slipped 0.07% to 4,672.00, and Bitcoin fell 2.25% to 76,888.25. No significant economic data was released, directing attention to oil dynamics and global risks.

The Day Ahead

April 29 features a sparse Nordic calendar, with no key data releases for Sweden, Norway, Denmark, or Finland. Sweden's parliament will vote on stricter citizenship rules, potentially impacting labor supply in its export-oriented economy if transitional provisions are excluded. In Norway, anticipation builds for May changes, including tax rebates and national budget updates, which could shape fiscal views.

Investors will track Brent crude fluctuations, as ongoing drops may erode Norway's oil income and krone value. ECB developments could influence Denmark's currency peg and Finland's borrowing costs. Without major indicators, emphasis shifts to geopolitical factors, such as Middle East tensions affecting energy markets.

Other Economic Notes

Oil price volatility from global conflicts threatens Nordic inflation and currency stability, especially for Norway as a major exporter. Sweden's industries contend with higher energy expenses, risking slower export expansion amid eurozone softness. Norway plans measures to curb elevated sick leave rates, aiming to enhance workforce efficiency post-pandemic.

(cont...)