Yesterday's Recap

Nordic markets exhibited varied movements on April 29, with the OMX Stockholm 30 declining 0.51% to 3,040.54 amid broader risk aversion, while Oslo Bors rose 0.19% to 1,997.11 buoyed by energy sector resilience. OMX Copenhagen 25 fell 1.24% to 1,717.44, reflecting export-oriented pressures in Denmark, whereas OMX Helsinki 25 advanced 0.94% to 6,238.59 on positive sentiment in Finland's eurozone-linked economy. Currency dynamics highlighted SEK weakness, with USD/SEK up 0.75% to 9.33 and EUR/SEK rising 0.25% to 10.88, contrasting with NOK's relative stability as USD/NOK edged up 0.12% to 9.32 but EUR/NOK declined 0.40% to 10.87.

Brent crude dropped 3.74% to 113.61, pressuring Norway's oil-dependent revenues, though the krone gained strength per local reports. Sweden's parliament passed a sweeping citizenship reform bill on April 29, rejecting opposition calls for transitional rules, which tightens requirements and could affect long-term workforce integration in the export-heavy economy. Bond yields climbed, with Sweden's 10Y government yield up 4.55 basis points to 2.76% and Norway's rising 1.99 basis points to 4.25%, signaling hawkish policy expectations.

No major macro data releases occurred across the Nordics, keeping focus on these market shifts and policy news.

The Day Ahead

The Nordic calendar remains quiet on April 30 with no scheduled economic releases or events across Sweden, Norway, Denmark, or Finland, allowing markets to digest recent global developments. Investors will monitor any spillover from international news, such as Brazil's rate cut amid resilient growth, which could influence commodity prices affecting Norway's oil sector. Attention may turn to broader eurozone indicators given Finland's ECB ties and Denmark's peg, though no direct Nordic data is due.

Potential forest fire risks in Sweden around Valborg celebrations could indirectly impact local sentiment, but macro focus stays subdued. Markets anticipate continued volatility in FX pairs like EUR/SEK and EUR/NOK amid global rate divergence. Overall, a light day positions Nordic assets to track external cues like Brent movements and equity trends.

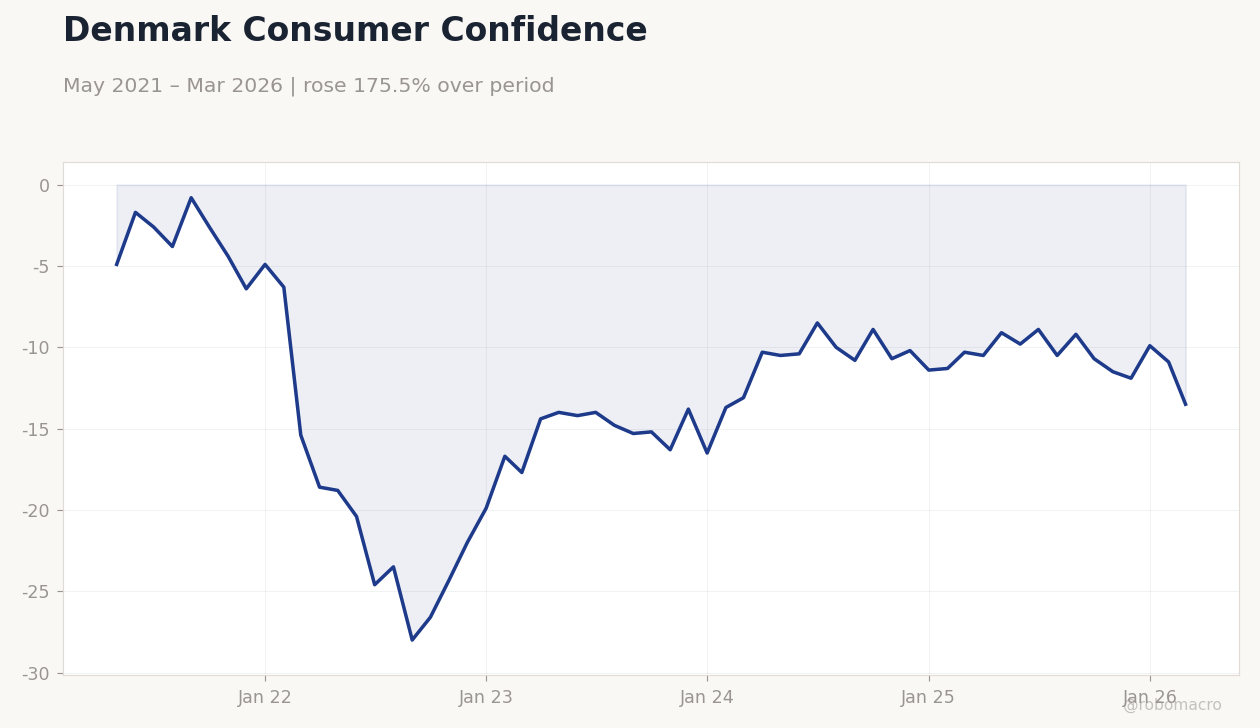

Denmark Consumer Confidence | Type: macro_line | Denmark Confidence Index: -13.5 (2026-03-01) | Range: -28–-0.8 | Trend(6pt): -4.9,-24.6,-15.3,-10.7,-9.9,-13.5

Denmark Consumer Confidence | Type: macro_line | Denmark Confidence Index: -13.5 (2026-03-01) | Range: -28–-0.8 | Trend(6pt): -4.9,-24.6,-15.3,-10.7,-9.9,-13.5