Nordics Macro Daily(Beta Mode)

Nordic Yields Rise, Krona Softens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,035.49 | -0.82% |

| Oslo Bors | 2,030.03 | +0.56% |

| OMX Copenhagen 25 | 1,734.20 | -1.04% |

| OMX Helsinki 25 | 6,325.63 | -0.03% |

| USD/SEK | 9.31 | +1.09% |

| USD/NOK | 9.28 | +0.27% |

| EUR/SEK | 10.88 | +0.67% |

| EUR/NOK | 10.85 | -0.39% |

| Brent Crude | 113.04 | -1.22% |

| Gold | 4,541.00 | +0.48% |

| Bitcoin | 80,849.99 | +2.94% |

| Sweden 10Y Govt Yield | 2.76% | +4.55% |

| Norway 10Y Govt Yield | 4.25% | +1.99% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

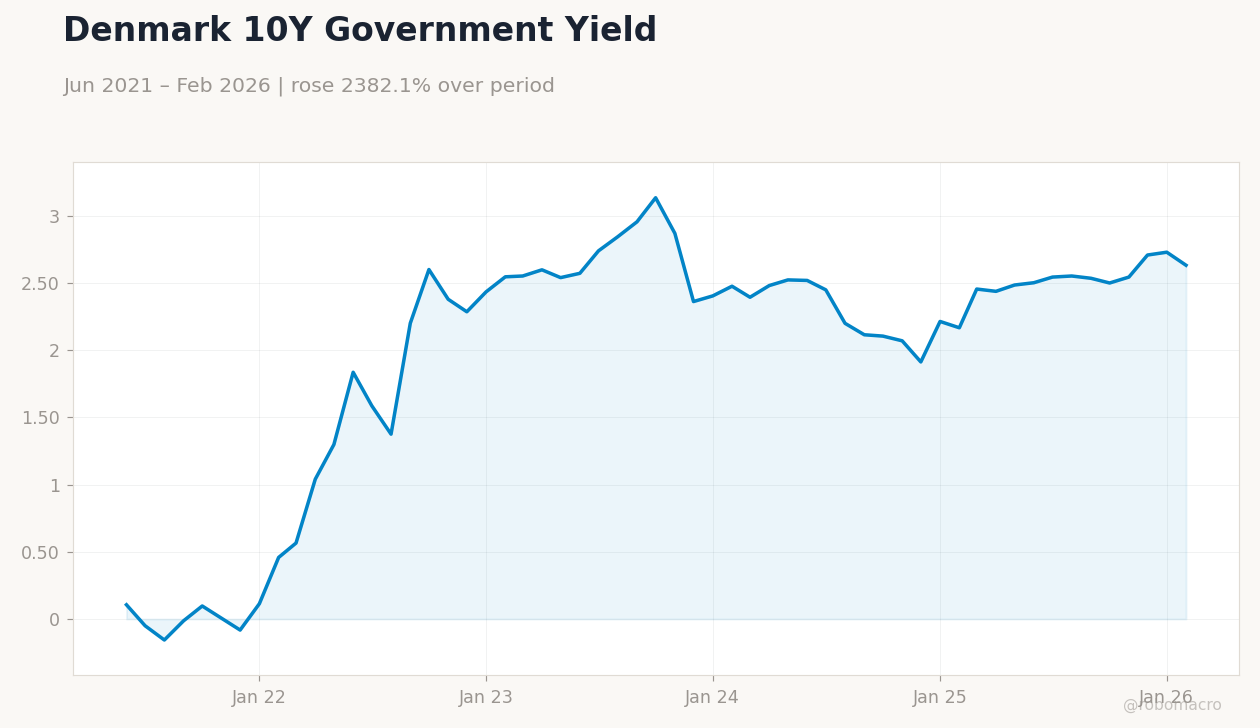

Nordic Yields Comparison | Type: macro_line | Norway 10Y Yield (%): 4.245 (2026-03-01) | Range: 1.23–4.245 | Trend(6pt): 1.47,3.336,3.967,3.599,4.162,4.245 | Denmark 10Y Yield (%): 2.631 (2026-02-01) | Range: -0.156–3.133 | Trend(5pt): 0.106,1.375,3.133,1.912,2.631

Nordic Yields Comparison | Type: macro_line | Norway 10Y Yield (%): 4.245 (2026-03-01) | Range: 1.23–4.245 | Trend(6pt): 1.47,3.336,3.967,3.599,4.162,4.245 | Denmark 10Y Yield (%): 2.631 (2026-02-01) | Range: -0.156–3.133 | Trend(5pt): 0.106,1.375,3.133,1.912,2.631

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Riksbank Rate Decision | 1.75 | - | 23:30 |

| Norges Bank Interest Rate Decision | 4 | - | 00:00 |

| Riksbank Press Conference | - | - | 01:00 |

- Nordic stocks mixed: Oslo up on energy, others dip amid risk-off.

- Krona weakens vs USD; Swedish yields jump on inflation concerns.

- Riksbank, Norges Bank decisions ahead, eyeing inflation and oil.

Yesterday's Recap

Nordic markets displayed mixed results on May 4, with the OMX Stockholm 30 declining 0.82% to 3,035.49 due to global risk aversion, while the Oslo Bors advanced 0.56% to 2,030.03, supported by energy stocks despite Brent crude falling 1.22% to $113.04. The OMX Copenhagen 25 decreased 1.04% to 1,734.20, pressured by export worries in Denmark's manufacturing sector, and the OMX Helsinki 25 slipped 0.03% to 6,325.63, constrained by eurozone linkages. Currencies reflected krona softening, with USD/SEK rising 1.09% to 9.31 and USD/NOK increasing 0.27% to 9.28, influenced by higher U.S.

yields. EUR/SEK gained 0.67% to 10.88, whereas EUR/NOK declined 0.39% to 10.85, indicating varied ECB impacts. Swedish 10-year government yields increased to 2.76% with a 4.55% change, reflecting bets on sustained inflation before the Riksbank meeting, and Norwegian 10-year yields rose to 4.25% with a 1.99% change, aided by oil prospects.

No key economic data was released, but positioning built for central bank events in Sweden and Norway. Gold advanced 0.48% to $4,541.00, providing haven support in volatile conditions, while Bitcoin climbed 2.94% to $80,849.99.

The Day Ahead

Focus shifts to the Riksbank rate decision at 23:30 on May 6, expected to maintain the repo rate at 1.75% given recent inflation signals. Norges Bank's rate announcement follows at 00:00 on May 7, anticipated to hold at 4% amid stable wage and GDP trends, though oil volatility may shape commentary. The Riksbank press conference at 01:00 on May 7 could offer clues on potential future adjustments, influencing SEK movements.

Denmark and Finland have no major releases, but ECB-related eurozone factors may affect DKK peg stability and Finnish markets indirectly. Expect subdued trading until these announcements, with emphasis on inflation guidance.

Other Economic Notes

Nordic economies grapple with ongoing services inflation hindering disinflation, especially in Sweden where export reliance and housing weakness pose risks. Norway gains from high Brent prices, bolstering fiscal positions and NOK resilience against energy disruptions. Denmark and Finland contend with eurozone challenges from energy impacts, with Finland's growth trailing due to ECB constraints.

Broader themes include oil-driven dynamics benefiting Norway while pressuring import-heavy peers like Sweden and Denmark.