Nordics Macro Daily(Beta Mode)

Nordics Mixed as Yields Climb, NOK Firms

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,061.49 | +0.20% |

| Oslo Bors | 2,057.35 | +0.85% |

| OMX Copenhagen 25 | 1,755.52 | -0.32% |

| OMX Helsinki 25 | 6,345.26 | +0.18% |

| USD/SEK | 9.41 | +0.36% |

| USD/NOK | 9.28 | +0.25% |

| EUR/SEK | 10.92 | -0.13% |

| EUR/NOK | 10.76 | -0.24% |

| Brent Crude | 110.79 | -0.44% |

| Gold | 4,472.10 | -0.76% |

| Bitcoin | 77,079.99 | +0.16% |

| Sweden 10Y Govt Yield | 2.78% | +0.75% |

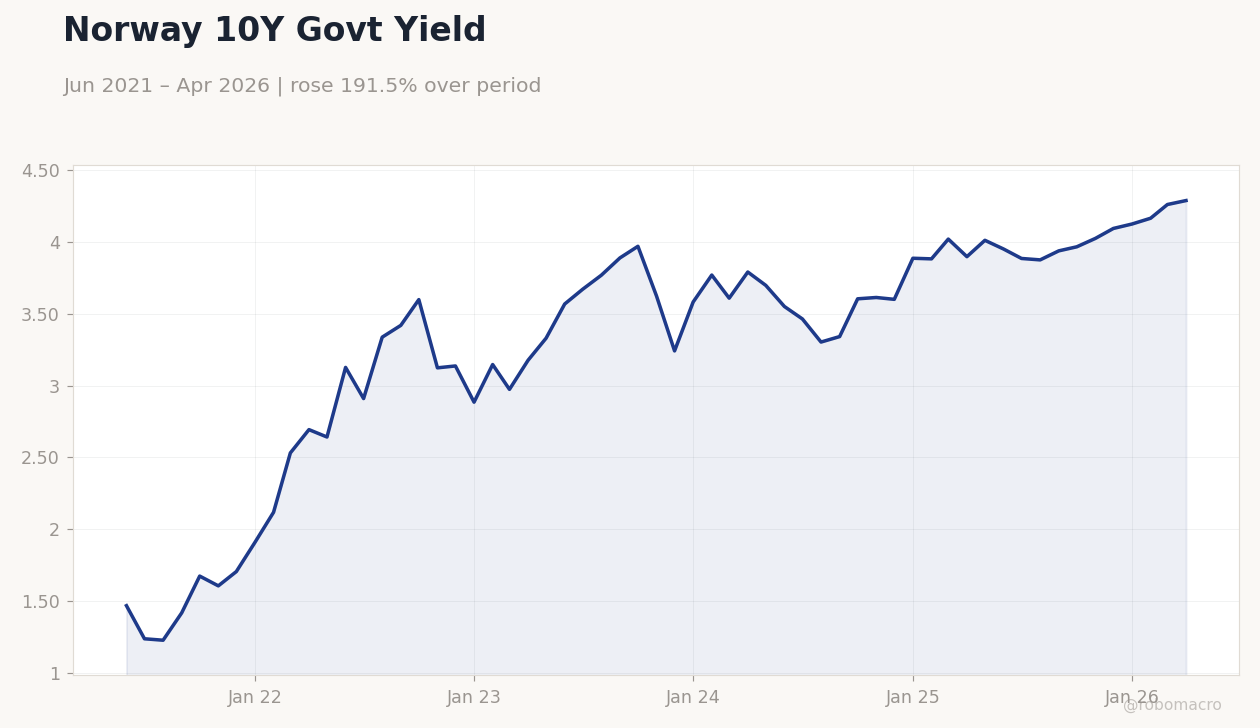

| Norway 10Y Govt Yield | 4.29% | +0.64% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Norway 10Y Govt Yield | Type: macro_line | Percent: 4.285 (2026-04-01) | Range: 1.23–4.285 | Trend(6pt): 1.47,3.336,3.967,3.599,4.162,4.285

Norway 10Y Govt Yield | Type: macro_line | Percent: 4.285 (2026-04-01) | Range: 1.23–4.285 | Trend(6pt): 1.47,3.336,3.967,3.599,4.162,4.285

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Nordic stock indices posted modest gains led by Oslo Bors, while government yields rose across Sweden and Norway amid thin data flow.

- Norges Bank trimmed holdings in UK equities and the krone strengthened on energy price support, while Riksbank conducted routine certificate operations.

- ECB deposit rate held at 2.00% with eurozone unemployment at 6.70%, anchoring Danish and Finnish policy expectations via the ERM II peg and ECB membership.

Yesterday's Recap

Nordic equity markets closed mixed on May 19. OMX Stockholm 30 advanced 0.20% to 3,061.49 while Oslo Bors surged 0.85% to 2,057.35, buoyed by energy exposure. OMX Copenhagen 25 slipped 0.32% to 1,755.52 and OMX Helsinki 25 edged 0.18% higher to 6,345.26.

USD/SEK rose 0.36% to 9.41 and USD/NOK gained 0.25% to 9.28, whereas EUR/SEK eased 0.13% to 10.92. Sweden’s 10-year yield climbed to 2.78% and Norway’s 10-year yield reached 4.29%. Riksbank completed certificate sales and Norges Bank reduced its stake in Spirax Group below 4%, with Brent crude at 110.79 supporting Norwegian fiscal balances.

The Day Ahead

No major economic releases are scheduled for Nordic markets on May 21. Attention will center on any follow-up commentary from Riksbank officials after recent certificate operations. Norges Bank may issue routine foreign-exchange transaction updates tied to oil revenue.

Danish and Finnish markets will track ECB communications for signals on the 2.00% deposit rate. Equity trading is expected to remain range-bound absent fresh inflation or labor data from Sweden or Norway.

Other Economic Notes

Sweden’s export-oriented manufacturing sector continues to benefit from stable euro-area demand despite the stronger krona. Norway’s oil production remains above forecast levels, sustaining a comfortable current-account surplus and limiting krone depreciation pressure. Danish shipping firms face elevated rerouting costs but maintain solid volume trends.

Finnish tech exports show resilience within the eurozone framework, while housing markets across the region remain subdued with limited price momentum.

Global Macro News

Elevated Brent prices at 110.79 continue to support commodity-linked currencies and fiscal positions in oil-exporting economies. US economic sentiment surveys signal rising pessimism, weighing on global risk appetite and indirectly supporting safe-haven flows into Nordic government bonds. Asian manufacturing PMIs point to contraction in several economies, curbing external demand for Swedish and Danish exports.

<i>↓ p.2</i>