Nordics Macro Daily(Beta Mode)

Sweden PPI Surge Tests Riksbank Cut Bets

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,162.19 | -0.96% |

| Oslo Bors | 2,045.90 | +0.12% |

| OMX Copenhagen 25 | 1,788.63 | +0.13% |

| OMX Helsinki 25 | 6,556.86 | +0.36% |

| USD/SEK | 9.29 | -0.01% |

| USD/NOK | 9.27 | +0.28% |

| EUR/SEK | 10.82 | +0.04% |

| EUR/NOK | 10.79 | +0.34% |

| Brent Crude | 95.16 | -4.44% |

| Gold | 4,510.00 | +0.21% |

| Bitcoin | 75,506.07 | -2.30% |

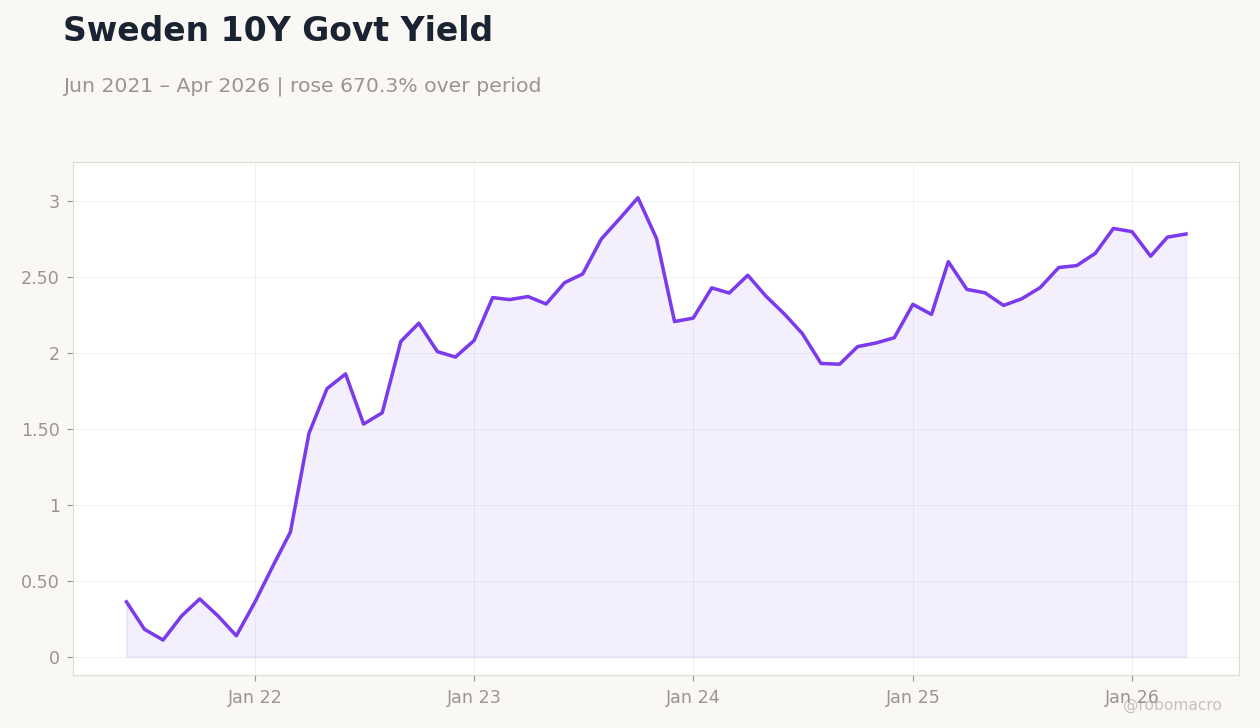

| Sweden 10Y Govt Yield | 2.78% | +0.75% |

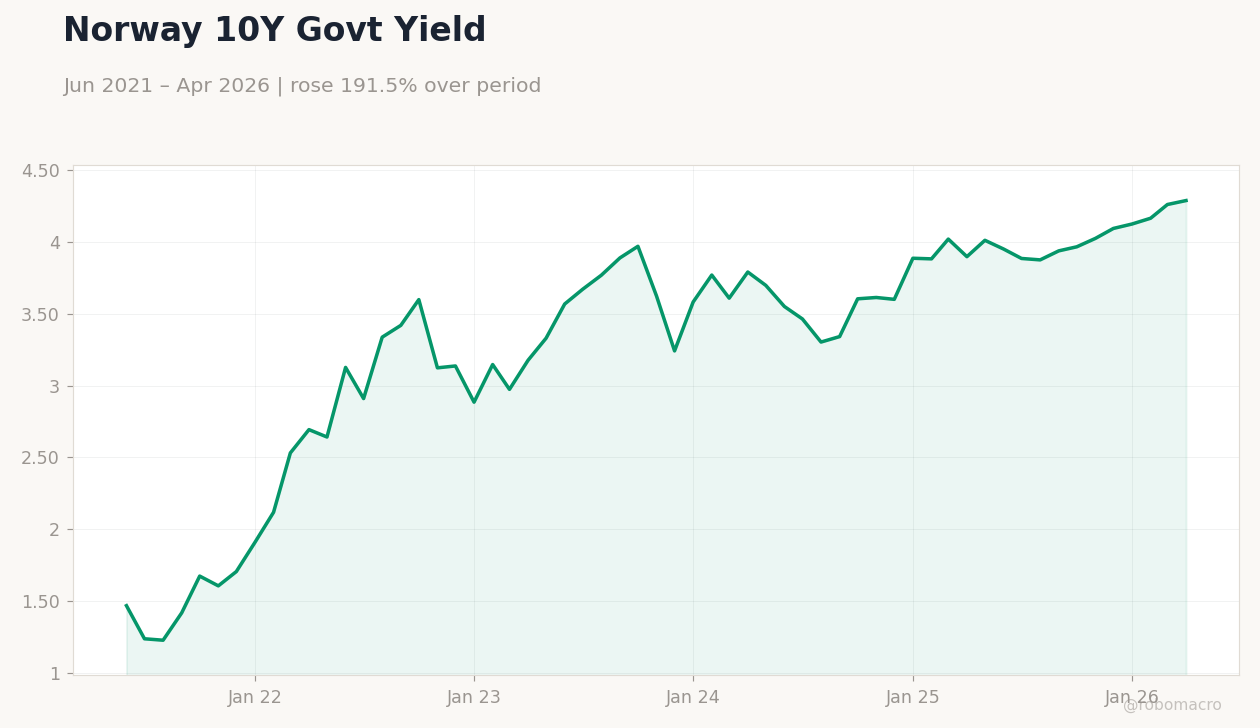

| Norway 10Y Govt Yield | 4.29% | +0.64% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Finland 10Y Govt Yield | Type: macro_line | Yield %: 3.38 (2026-04-01) | Range: -0.2151–3.47 | Trend(6pt): -0.01767,1.625,3.47,2.645,3.16,3.38

Finland 10Y Govt Yield | Type: macro_line | Yield %: 3.38 (2026-04-01) | Range: -0.2151–3.47 | Trend(6pt): -0.01767,1.625,3.47,2.645,3.16,3.38

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Sweden PPI jump challenges Riksbank summer rate-cut expectations and supports the krona.

- Nordic equities closed mixed with OMX Stockholm 30 falling 0.96% while Oslo Bors rose 0.12%.

- Brent crude dropped 4.44% to $95.16, weighing on Norway’s fiscal outlook while Nordic yields edged higher.

Yesterday's Recap

Sweden’s producer price index rose more than expected, lifting inflation concerns and reducing odds of a near-term Riksbank easing move. The OMX Stockholm 30 declined 0.96% to 3,162.19 as rate-sensitive shares sold off. Oslo Bors advanced 0.12% to 2,045.90, supported by energy names despite the Brent decline.

OMX Copenhagen 25 gained 0.13% to 1,788.63 while OMX Helsinki 25 rose 0.36% to 6,556.86. USD/SEK held near 9.29 and USD/NOK climbed 0.28% to 9.27. Sweden’s 10-year yield increased 0.75% to 2.78% and Norway’s 10-year yield rose 0.64% to 4.29%.

The krona firmed on the back of firmer Swedish inflation prints while the krone showed modest resilience.

The Day Ahead

Nordic markets face a data-light session with no major releases scheduled across the four economies. Traders will monitor any follow-through from Sweden’s PPI print and oil-price volatility. Equity flows may remain cautious ahead of month-end positioning.

Currency markets are expected to track global risk sentiment and any ECB-related comments. Bond markets should stay focused on yield differentials between Sweden and Norway.

Other Economic Notes

Sweden’s export-oriented manufacturing sector faces headwinds from higher domestic costs after the PPI increase. Norway’s oil revenue outlook remains supported by Brent near $95 despite the daily drop, helping underpin the government’s fiscal balance. Denmark’s manufacturing exports continue to benefit from euro-area demand while the krone stays anchored to the euro via the ERM II peg.

Finland’s industrial output stays tied to eurozone growth and ECB policy settings.

Global Macro News

Brent’s sharp decline transmitted immediate pressure to Norway’s external accounts and NOK valuation. Global equity weakness weighed on rate-sensitive Nordic shares, particularly in Sweden. Oil shocks elsewhere raised imported inflation risks that could spill into Danish and Finnish price data.

Central banks outside the Nordics signaled tighter policy in response to energy prices, reinforcing the Riksbank’s cautious stance. <i>↓ p.2</i>