Nordics Macro Daily(Beta Mode)

Swedish Inflation Risks Lift Riksbank Odds

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,149.92 | +1.79% |

| Oslo Bors | 2,007.62 | -0.08% |

| OMX Copenhagen 25 | 1,752.52 | -0.62% |

| OMX Helsinki 25 | 6,562.83 | +1.55% |

| USD/SEK | 9.33 | +0.28% |

| USD/NOK | 9.30 | +0.30% |

| EUR/SEK | 10.85 | +0.16% |

| EUR/NOK | 10.81 | +0.19% |

| Brent Crude | 97.01 | +1.05% |

| Gold | 4,500.50 | +0.25% |

| Bitcoin | 66,911.58 | -6.18% |

| Sweden 10Y Govt Yield | 2.78% | +0.75% |

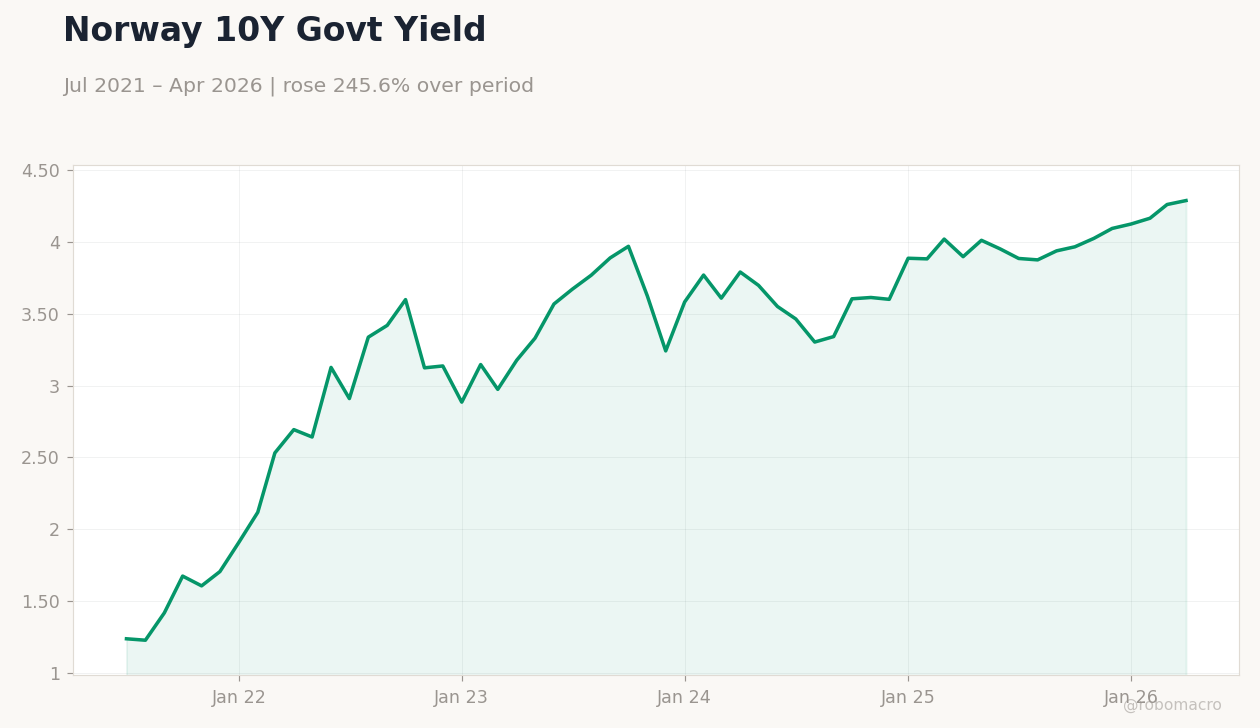

| Norway 10Y Govt Yield | 4.29% | +0.64% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Sweden 10Y Govt Yield | Type: macro_line | Yield %: 2.785 (2026-04-01) | Range: 0.1101–3.024 | Trend(6pt): 0.1808,2.077,2.755,2.321,2.764,2.785

Sweden 10Y Govt Yield | Type: macro_line | Yield %: 2.785 (2026-04-01) | Range: 0.1101–3.024 | Trend(6pt): 0.1808,2.077,2.755,2.321,2.764,2.785

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Sweden’s hotter inflation print raises Riksbank tightening probabilities while markets price limited near-term action.

- Nordic equities diverged, with Stockholm and Helsinki advancing on local buying while Copenhagen and Oslo eased.

- Norges Bank equity purchases continued across U.S. names as Brent crude climbed above $97.

Yesterday's Recap

Swedish equity benchmark OMX Stockholm 30 rose 1.79 percent to 3,149.92 as investors digested Rabobank analysis that flagged upside risks to inflation and potential Riksbank policy adjustment. Oslo Bors slipped 0.08 percent to 2,007.62 despite Brent crude advancing 1.05 percent to 97.01 dollars per barrel, which supports Norway’s fiscal position. Copenhagen’s OMX 25 fell 0.62 percent to 1,752.52 while Helsinki’s OMX 25 gained 1.55 percent to 6,562.83.

USD/SEK climbed 0.28 percent to 9.33 and USD/NOK rose 0.30 percent to 9.30, reflecting modest Nordic currency softening. Swedish ten-year yields increased 0.75 percent to 2.78 percent and Norwegian ten-year yields rose 0.64 percent to 4.29 percent. Rabobank noted that VAT effects cloud Sweden’s inflation signal yet still see growth and Riksbank risks tilted higher.

Norges Bank added positions in several U.S. equities without altering its domestic policy stance.

The Day Ahead

No major Nordic data releases are scheduled for the coming session, leaving markets to focus on ongoing inflation commentary from Sweden. Riksbank certificate operations will continue without altering liquidity conditions. Norwegian oil revenue flows remain supportive for the krone while Brent holds near current levels.

Danish exporters tied to Novo Nordisk will continue to drive GDP outperformance relative to euro-area peers. Finnish indicators stay aligned with ECB-wide trends given the absence of independent policy tools. Investors will monitor any follow-up remarks from Rabobank or Riksbank officials on the latest inflation assessment.

Other Economic Notes

Sweden’s housing market weakness persists and continues to weigh on household spending despite stable unemployment. Denmark’s economy benefits from strong pharmaceutical exports that offset softer domestic demand elsewhere in the region. Norway’s oil-funded fiscal framework gains from elevated energy prices, reducing pressure on Norges Bank to ease.

Finland remains fully exposed to euro-area growth and inflation dynamics under ECB control. Regional credit spreads showed no material widening amid the mixed equity session.