Nordics Macro Daily(Beta Mode)

Nordic Equities Mixed as Krona Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,134.46 | -0.49% |

| Oslo Bors | 2,010.98 | +0.17% |

| OMX Copenhagen 25 | 1,734.74 | -1.01% |

| OMX Helsinki 25 | 6,602.84 | +0.61% |

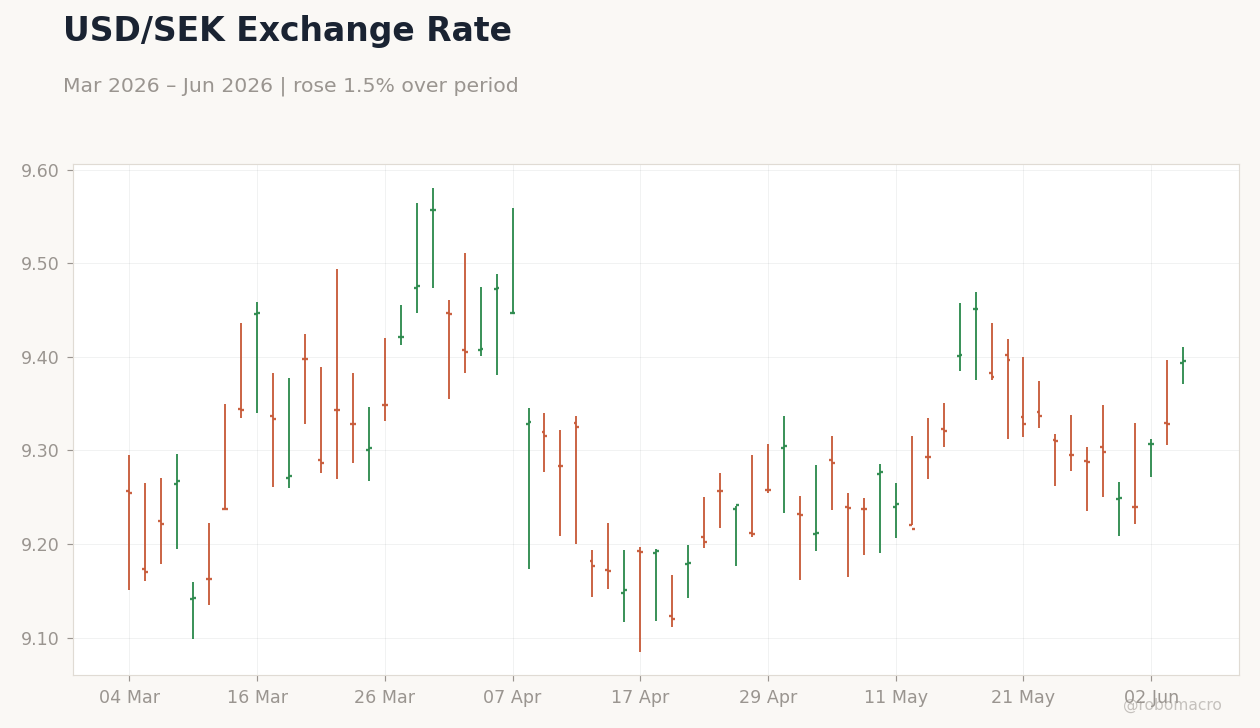

| USD/SEK | 9.39 | +0.70% |

| USD/NOK | 9.32 | +0.37% |

| EUR/SEK | 10.90 | +0.57% |

| EUR/NOK | 10.82 | +0.24% |

| Brent Crude | 97.06 | -0.77% |

| Gold | 4,503.90 | +1.51% |

| Bitcoin | 63,710.00 | -4.49% |

| Sweden 10Y Govt Yield | 2.78% | +0.75% |

| Norway 10Y Govt Yield | 4.29% | +0.64% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Sweden 10Y Government Yield | Type: macro_line | Yield %: 2.785 (2026-04-01) | Range: 0.1101–3.024 | Trend(6pt): 0.1808,2.077,2.755,2.321,2.764,2.785

Sweden 10Y Government Yield | Type: macro_line | Yield %: 2.785 (2026-04-01) | Range: 0.1101–3.024 | Trend(6pt): 0.1808,2.077,2.755,2.321,2.764,2.785

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Swedish and Danish equities declined while Norwegian and Finnish indices advanced modestly amid mixed Nordic equity performance.

- USD/SEK rose 0.70% to 9.39 and USD/NOK gained 0.37% to 9.32, reflecting krona and krone softening against the dollar.

- Sweden 10-year yields climbed 0.75% to 2.78% and Norway 10-year yields increased 0.64% to 4.29% as Brent crude fell 0.77% to 97.06.

Yesterday's Recap

Nordic equity markets closed mixed on June 3. OMX Stockholm 30 fell 0.49% to 3,134.46 while OMX Copenhagen 25 dropped 1.01% to 1,734.74. Oslo Bors rose 0.17% to 2,010.98 and OMX Helsinki 25 gained 0.61% to 6,602.84.

The Swedish krona weakened as USD/SEK climbed to 9.39 and EUR/SEK reached 10.90. USD/NOK advanced to 9.32 and EUR/NOK to 10.82. Brent crude declined to 97.06, weighing on energy-related sentiment in Norway.

Gold rose 1.51% to 4,503.90 while Bitcoin fell 4.49% to 63,710.00. No major data releases occurred across the Nordic bloc.

The Day Ahead

The calendar shows no scheduled economic releases for June 4 across Sweden, Norway, Denmark or Finland. Markets will monitor ongoing commentary from Riksbank and Norges Bank officials for policy signals. Danish retail sales and Finnish trade data are expected later in the week.

FX markets remain focused on krona and krone movements against the euro. Equity trading is likely to stay range-bound absent fresh catalysts.

Other Economic Notes

Sweden’s VAT-adjusted inflation continues to cloud growth assessments and keeps markets pricing limited Riksbank easing. Denmark’s economy benefits from strong Novo Nordisk exports, supporting a raised 2026 GDP forecast of 3.7%. The Danish krone tested record lows against the euro, pressuring Danmarks Nationalbank’s ERM II peg defense.

Norway’s oil fund maintains steady inflows from energy revenues despite the Brent pullback. Finnish activity remains aligned with broader euro-area conditions.

Global Macro News

The Federal Reserve transition to Chair Warsh occurs against persistent US inflation pressures that may delay global rate cuts. Eurozone unemployment stands at 6.70%, providing a stable external backdrop for Nordic exporters. IMF forecasts highlight resilient but slower growth in key trading partners such as Saudi Arabia.

Brazilian economic weakness adds to emerging-market volatility that can spill into Nordic FX. <i>↓ p.2</i>