Nordics Macro Daily(Beta Mode)

Nordic Stocks Slip as Krone Weakens Despite Oil Rally

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,106.76 | -0.31% |

| Oslo Bors | 1,993.13 | -0.54% |

| OMX Copenhagen 25 | 1,741.24 | -0.88% |

| OMX Helsinki 25 | 6,456.10 | -0.24% |

| USD/SEK | 9.37 | -0.14% |

| USD/NOK | 9.46 | +1.35% |

| EUR/SEK | 10.88 | -0.09% |

| EUR/NOK | 10.92 | +0.75% |

| Brent Crude | 94.70 | +1.73% |

| Gold | 4,365.10 | +0.65% |

| Bitcoin | 63,549.11 | +0.49% |

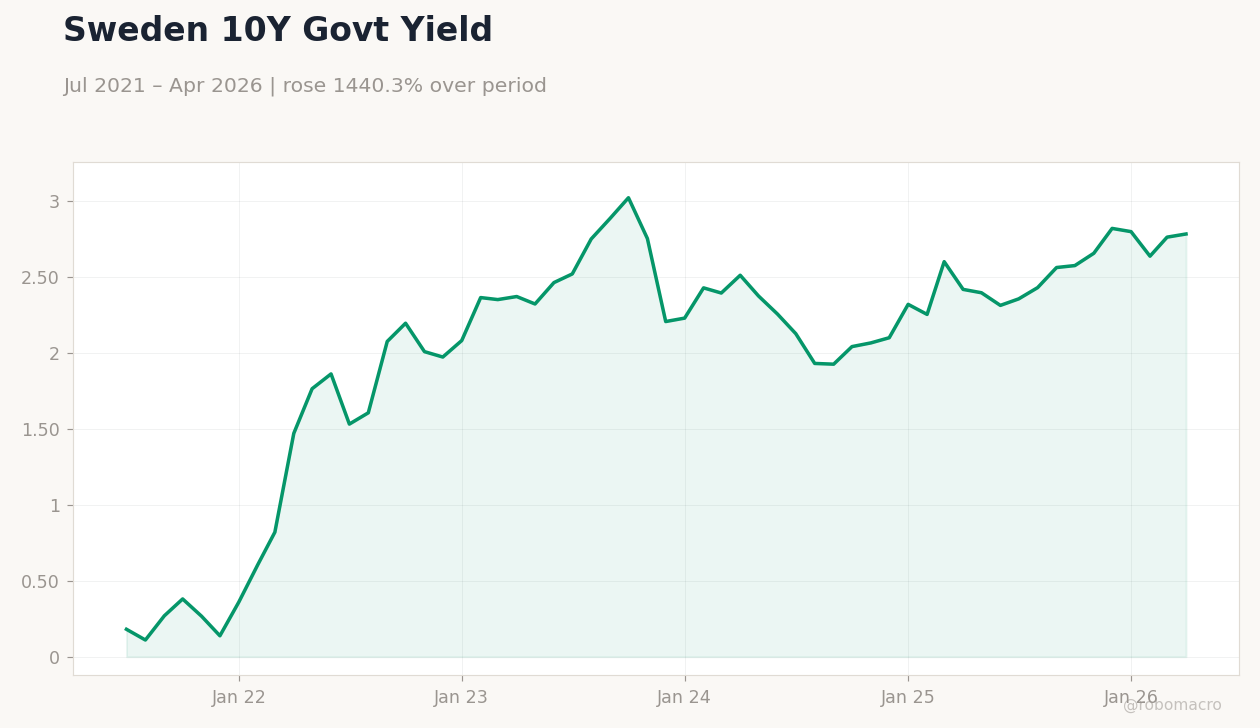

| Sweden 10Y Govt Yield | 2.78% | +0.75% |

| Norway 10Y Govt Yield | 4.29% | +0.64% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Sweden 3M Interbank Rate | Type: macro_line | Percent: 1.936 (2026-04-01) | Range: -0.3847–4.102 | Trend(6pt): -0.1551,1.51,4.102,2.331,1.936,1.936

Sweden 3M Interbank Rate | Type: macro_line | Percent: 1.936 (2026-04-01) | Range: -0.3847–4.102 | Trend(6pt): -0.1551,1.51,4.102,2.331,1.936,1.936

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Nordic equity indices declined across the board, with OMX Copenhagen 25 falling 0.88% and Oslo Bors down 0.54% amid thin volumes.

- USD/NOK rose 1.35% to 9.46 while Brent crude gained 1.73% to $94.70, supporting Norway’s fiscal position but pressuring the krone.

- Sweden 10-year yields climbed 0.75% to 2.78% and Norway 10-year yields rose 0.64% to 4.29% as Riksbank conducted routine government bond auctions.

Yesterday's Recap

Nordic equity markets posted broad-based losses on June 7 despite the absence of major data releases. OMX Stockholm 30 fell 0.31% to 3,106.76 while OMX Helsinki 25 declined 0.24%. The Norwegian krone weakened notably, with USD/NOK climbing 1.35% to 9.46 and EUR/NOK rising 0.75% to 10.92, even as Brent crude advanced 1.73%.

Riksbank bond auctions proceeded without incident, providing steady liquidity to the Swedish government curve. USD/SEK eased 0.14% to 9.37 and EUR/SEK slipped 0.09% to 10.88. Gold rose 0.65% to $4,365.10 while Bitcoin added 0.49%.

Denmark’s OMX Copenhagen 25 led the downside with a 0.88% drop.

The Day Ahead

No major Nordic data releases or central bank events are scheduled for June 8. Markets will focus on any follow-through from the Riksbank’s bond operations and ongoing oil price momentum. Norway’s krone will remain sensitive to Brent moves above $94.

Sweden’s housing market and labor data from earlier weeks continue to shape rate expectations. Thin summer liquidity may amplify any external equity or FX flows into Nordic assets. Denmark and Finland remain quiet ahead of euro-area developments later in the week.

Other Economic Notes

Sweden’s export-oriented manufacturing sector faces headwinds from softer euro-area demand while Norway benefits directly from elevated Brent prices through higher petroleum revenue. Danish growth remains tied to euro-area cycles given the ERM II peg. Finland’s outlook is shaped by ECB policy and eurozone unemployment at 6.70%.

Housing markets in Sweden show tentative stabilization after earlier rate cuts, though mortgage-rate relief has yet to generate sustained price momentum.

Global Macro News

Brent’s advance above $94 supports Norway’s structural non-oil deficit room and fiscal buffers. Global risk sentiment stayed cautious, weighing on Nordic equities despite the commodity tailwind. The ECB deposit rate remains at 2.00%, anchoring policy for Finland and limiting divergence for Denmark’s Nationalbank.

<i>↓ p.2</i>