Nordics Macro Daily(Beta Mode)

Riksbank to Hold at 1.75% on Soft Growth

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,106.76 | -0.31% |

| Oslo Bors | nan | +nan% |

| OMX Copenhagen 25 | 1,741.24 | -0.88% |

| OMX Helsinki 25 | 6,456.10 | -0.24% |

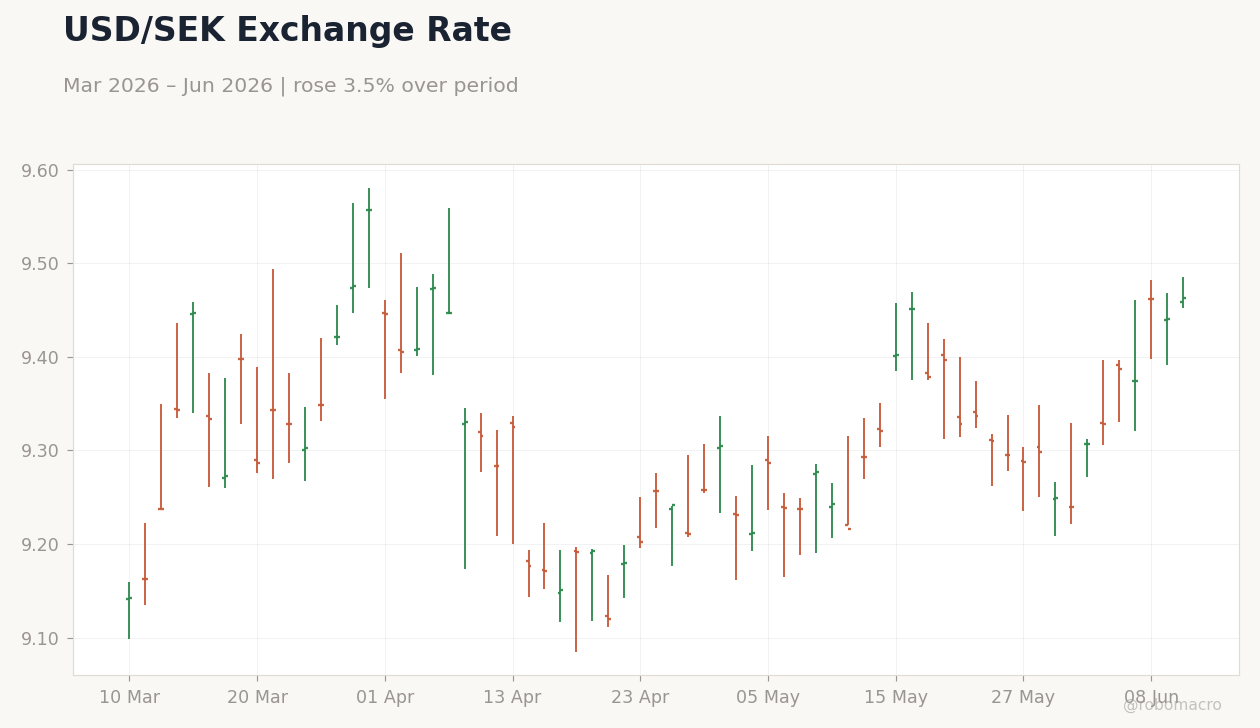

| USD/SEK | 9.46 | +0.18% |

| USD/NOK | 9.47 | +0.17% |

| EUR/SEK | 10.93 | +0.41% |

| EUR/NOK | 10.92 | +0.23% |

| Brent Crude | 91.27 | -0.20% |

| Gold | 4,233.70 | -0.62% |

| Bitcoin | 61,406.65 | -0.38% |

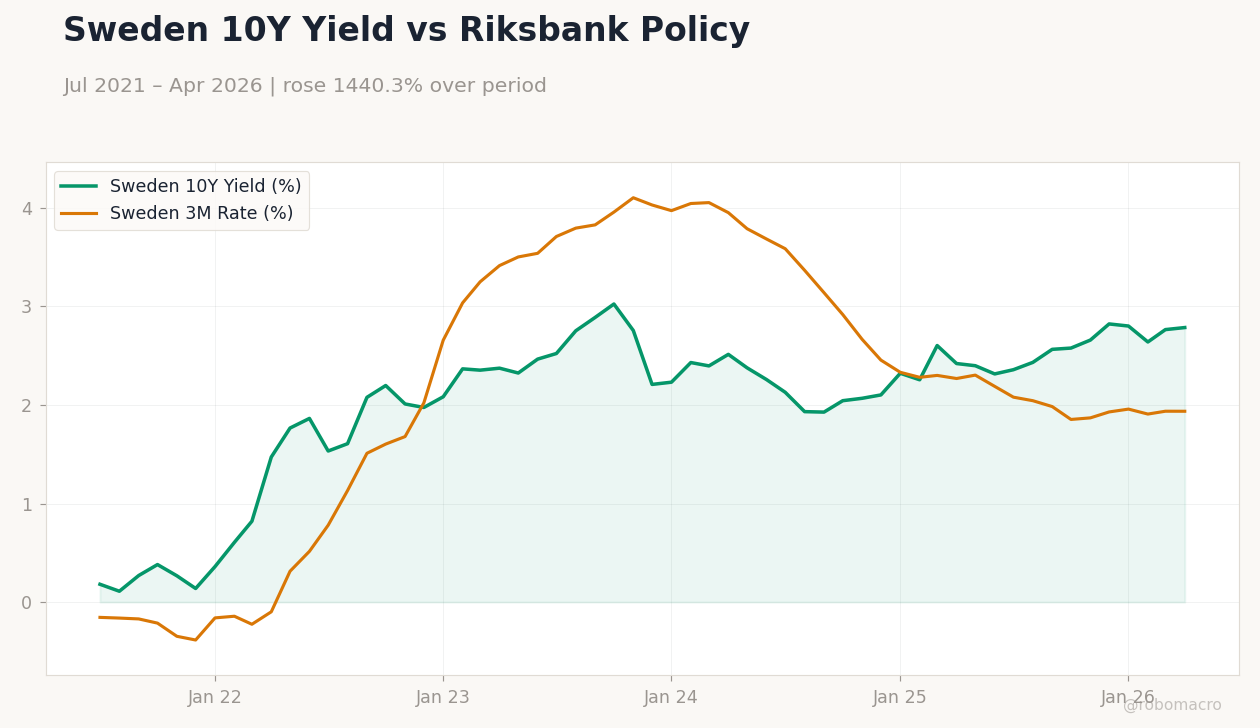

| Sweden 10Y Govt Yield | 2.78% | +0.75% |

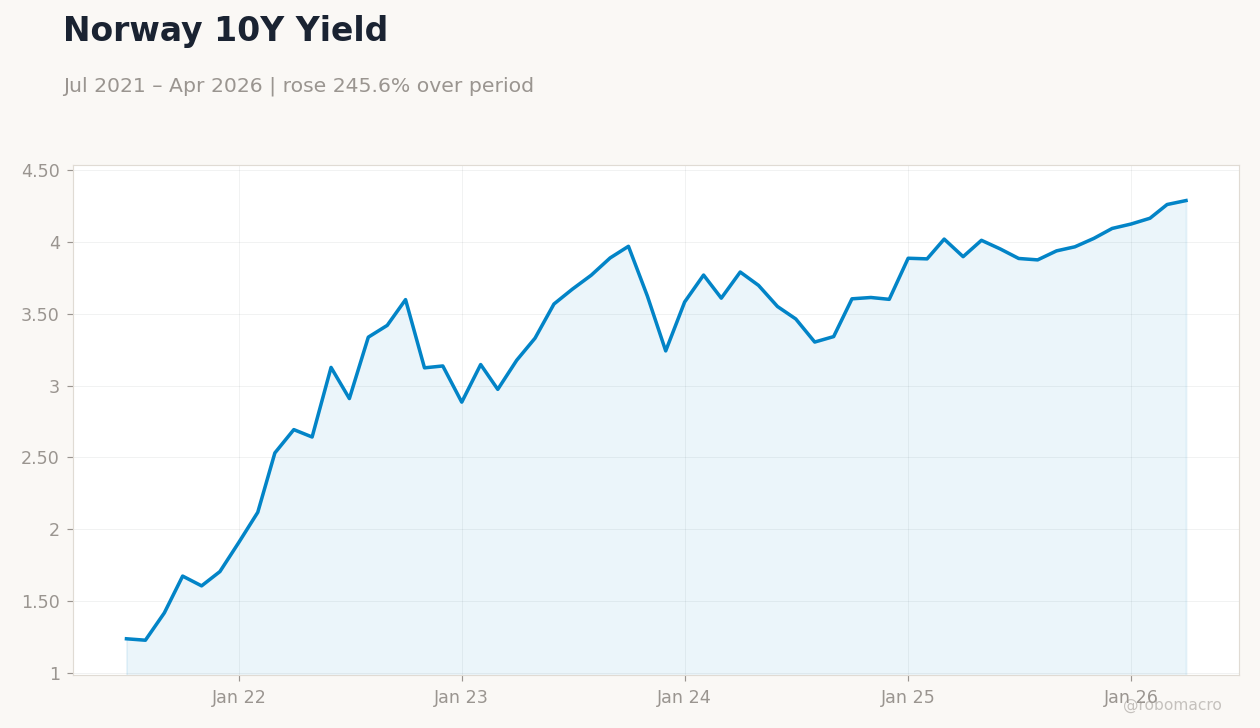

| Norway 10Y Govt Yield | 4.29% | +0.64% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Finland 10Y Yield | Type: macro_line | Finland 10Y Yield (%): 3.38 (2026-04-01) | Range: -0.2151–3.47 | Trend(6pt): -0.09563,2.421,3.2,2.945,3.322,3.38

Finland 10Y Yield | Type: macro_line | Finland 10Y Yield (%): 3.38 (2026-04-01) | Range: -0.2151–3.47 | Trend(6pt): -0.09563,2.421,3.2,2.945,3.322,3.38

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- UBS forecasts Riksbank pause at 1.75% amid slowing Swedish activity

- Nordic equities fall, Copenhagen 25 drops 0.88% while Stockholm 30 slips 0.31%

- SEK and NOK weaken versus USD as 10-year yields rise across the region

Yesterday's Recap

Equity markets closed lower across the Nordics with OMX Stockholm 30 falling 0.31% to 3,106.76 and OMX Copenhagen 25 declining 0.88% to 1,741.24. OMX Helsinki 25 edged down 0.24% to 6,456.10 while Oslo Bors data remained unavailable. Government bond yields increased, with Sweden’s 10-year yield rising 0.75% to 2.78% and Norway’s 10-year yield advancing 0.64% to 4.29%.

USD/SEK climbed 0.18% to 9.46 and USD/NOK gained 0.17% to 9.47, reflecting modest krona and krone depreciation. News centered on UBS analysis that the Riksbank will keep its policy rate at 1.75% given subdued Swedish growth, with no major data releases reported in any Nordic country. Brent crude eased 0.20% to 91.27, offering limited support to Norwegian fiscal revenues.

Eurozone unemployment stood at 6.70%, underscoring persistent slack that may keep ECB Deposit Rate at 2.00% for longer. Global risk sentiment stayed cautious, pressuring Nordic equities alongside broader European indices. Oil markets traded near 91 dollars, supporting Norwegian external balances while limiting upside for the krone.

Gold declined 0.62% to 4,233.70, reflecting reduced safe-haven demand. Bitcoin fell 0.38% to 61,406.65 amid ongoing regulatory scrutiny worldwide.

The Day Ahead

The calendar shows no scheduled releases across Sweden, Norway, Denmark or Finland. Attention will likely remain on Riksbank certificate operations and any follow-up commentary from Norges Bank officials. Market participants may monitor EUR/SEK and EUR/NOK moves for signs of further currency pressure ahead of summer.

Danish Nationalbank activity will stay focused on maintaining the EUR/DKK peg amid stable ECB policy. Quiet data flow should keep trading volumes light across Nordic assets.

Other Economic Notes

Swedish housing prices remained flat in recent prints, signaling a fragile recovery that could delay household spending momentum. Norway’s tight labor market continues to underpin Norges Bank’s cautious stance despite softer oil output. Export-oriented manufacturing in Sweden and Denmark faces headwinds from subdued euro-area demand.

Finland’s eurozone membership transmits ECB policy directly, limiting independent scope for stimulus. <i>↓ p.2</i>