Nordics Macro Daily(Beta Mode)

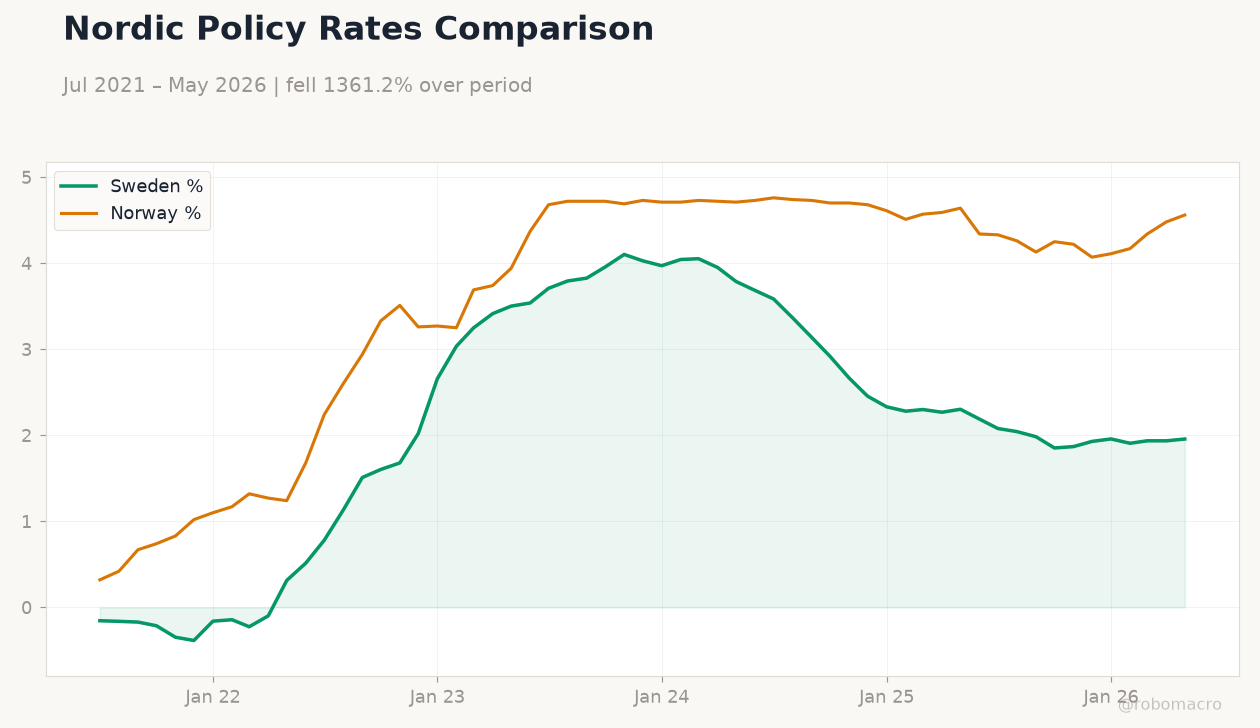

Riksbank Holds Rate, Signals Hike Risk

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,180.67 | +0.61% |

| Oslo Bors | 1,951.81 | +0.03% |

| OMX Copenhagen 25 | 1,759.18 | -0.13% |

| OMX Helsinki 25 | 6,317.02 | -0.11% |

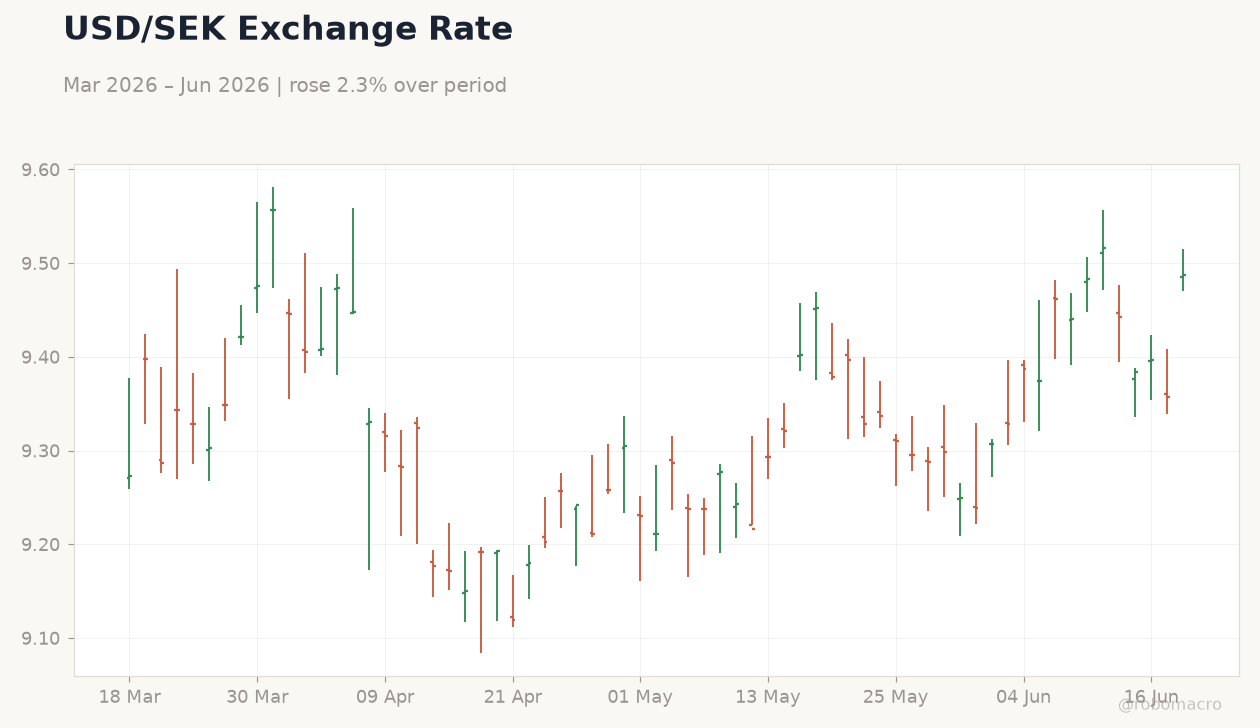

| USD/SEK | 9.49 | +1.37% |

| USD/NOK | 9.59 | +1.29% |

| EUR/SEK | 10.92 | +0.57% |

| EUR/NOK | 11.04 | +0.46% |

| Brent Crude | 77.88 | -2.10% |

| Gold | 4,326.50 | -0.74% |

| Bitcoin | 64,003.99 | -2.43% |

| Sweden 10Y Govt Yield | 2.74% | -1.45% |

| Norway 10Y Govt Yield | 4.33% | +1.01% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Riksbank Rate Decision | 1.75 | 1.75 | 1.75 |

| Riksbank Press Conference | - | - | - |

Sweden 10Y Yield | Type: macro_line | 10Y Yield %: 2.745 (2026-05-01) | Range: 0.1101–3.024 | Trend(6pt): 0.1808,2.077,2.755,2.321,2.764,2.745

Sweden 10Y Yield | Type: macro_line | 10Y Yield %: 2.745 (2026-05-01) | Range: 0.1101–3.024 | Trend(6pt): 0.1808,2.077,2.755,2.321,2.764,2.745

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Norges Bank Interest Rate Decision | 4.25 | 4.25 | 00:00 |

- Riksbank holds policy rate at 1.75% and signals elevated probability of a hike this year after cutting its inflation outlook.

- OMX Stockholm 30 rises 0.61% while USD/SEK jumps 1.37% and Sweden 10Y yield falls 1.45% to 2.74%.

- Norges Bank set to announce rate decision today with consensus pointing to a hold at 4.25%.

Yesterday's Recap

Sweden’s Riksbank kept its policy rate unchanged at 1.75% and delivered a mildly hawkish message by raising the odds of a hike later this year even as it lowered its inflation forecast. The decision followed softer Swedish inflation prints that had previously supported cut expectations. OMX Stockholm 30 advanced 0.61% to 3,180.67 while Oslo Bors edged 0.03% higher to 1,951.81.

OMX Copenhagen 25 slipped 0.13% and OMX Helsinki 25 fell 0.11%. USD/SEK climbed 1.37% to 9.49 and EUR/SEK rose 0.57% to 10.92, reflecting krona weakness. Sweden’s 10Y government yield declined 1.45% to 2.74% while Norway’s 10Y yield increased 1.01% to 4.33%.

Brent crude dropped 2.10% to 77.88, weighing on NOK which saw USD/NOK rise 1.29% to 9.59.

The Day Ahead

Norges Bank is scheduled to announce its interest rate decision at midnight ET with markets pricing a hold at 4.25%. No other high-impact Nordic data releases are listed for the session. Attention will center on any updated signals regarding the timing of future cuts given recent oil-price volatility.

Danish and Finnish markets will take cues from the ECB path and any EUR/DKK intervention commentary. Equity and FX trading desks will monitor NOK reaction for clues on oil-fund rebalancing flows.

Other Economic Notes

OECD called on Norway to lower its wealth tax as part of broader tax reform aimed at improving competitiveness. Swedish housing starts continued their multi-year decline, keeping pressure on domestic banks’ mortgage portfolios. Export-oriented manufacturing sectors in Sweden and Denmark remain sensitive to global demand shifts and EUR/SEK levels.

Finland’s eurozone membership keeps its policy transmission aligned with ECB actions rather than independent Nordic moves.

Global Macro News

ECB President Lagarde noted that energy-price increases are spreading through the eurozone economy, with the deposit rate steady at 2.25%. Eurozone unemployment stood at 6.70%. China’s export surge contrasted with weakening domestic demand, raising questions about external demand for Nordic machinery and vehicles.

<i>↓ p.2</i>