Nordics Macro Daily(Beta Mode)

Riksbank, Norges Bank Hold Rates; NOK Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,178.64 | +0.55% |

| Oslo Bors | 1,927.39 | -1.25% |

| OMX Copenhagen 25 | 1,744.07 | -0.99% |

| OMX Helsinki 25 | 6,238.40 | -1.35% |

| USD/SEK | 9.60 | +0.97% |

| USD/NOK | 9.76 | +1.50% |

| EUR/SEK | 10.98 | +0.39% |

| EUR/NOK | 11.16 | +0.92% |

| Brent Crude | 80.29 | +0.55% |

| Gold | 4,156.00 | -1.61% |

| Bitcoin | 62,852.69 | -0.07% |

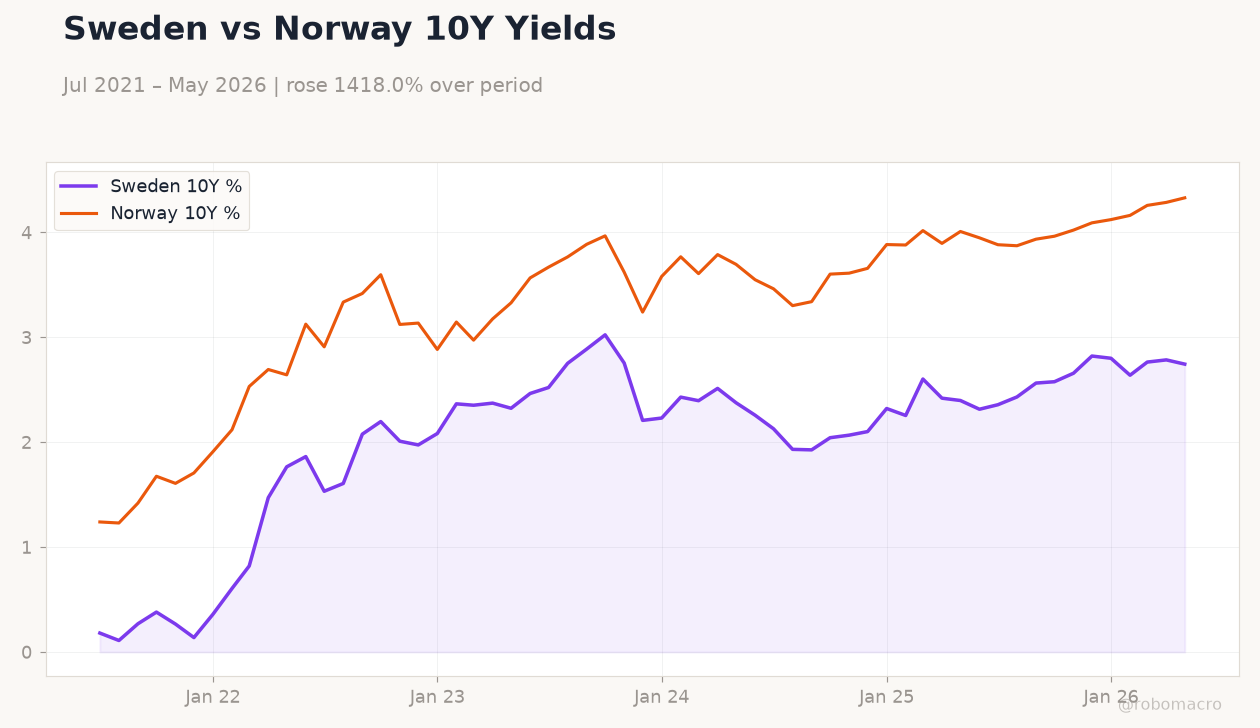

| Sweden 10Y Govt Yield | 2.74% | -1.45% |

| Norway 10Y Govt Yield | 4.33% | +1.01% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

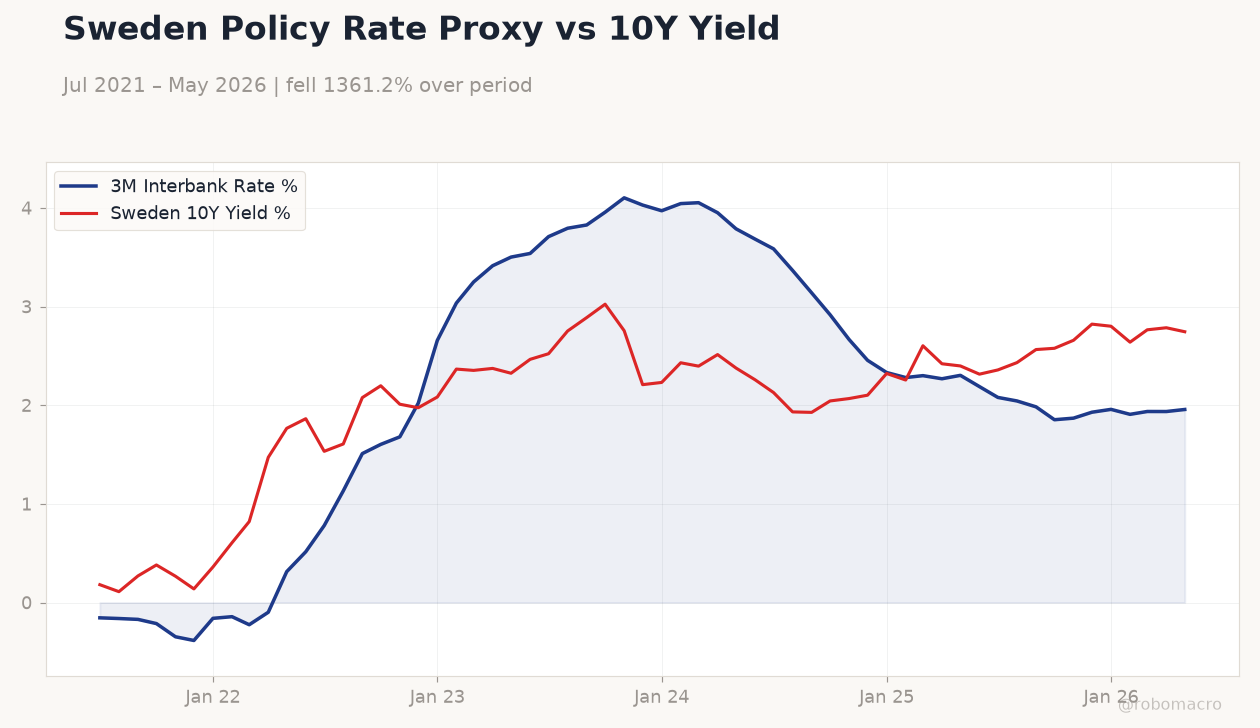

| Riksbank Rate Decision | 1.75 | 1.75 | 1.75 |

| Riksbank Press Conference | - | - | - |

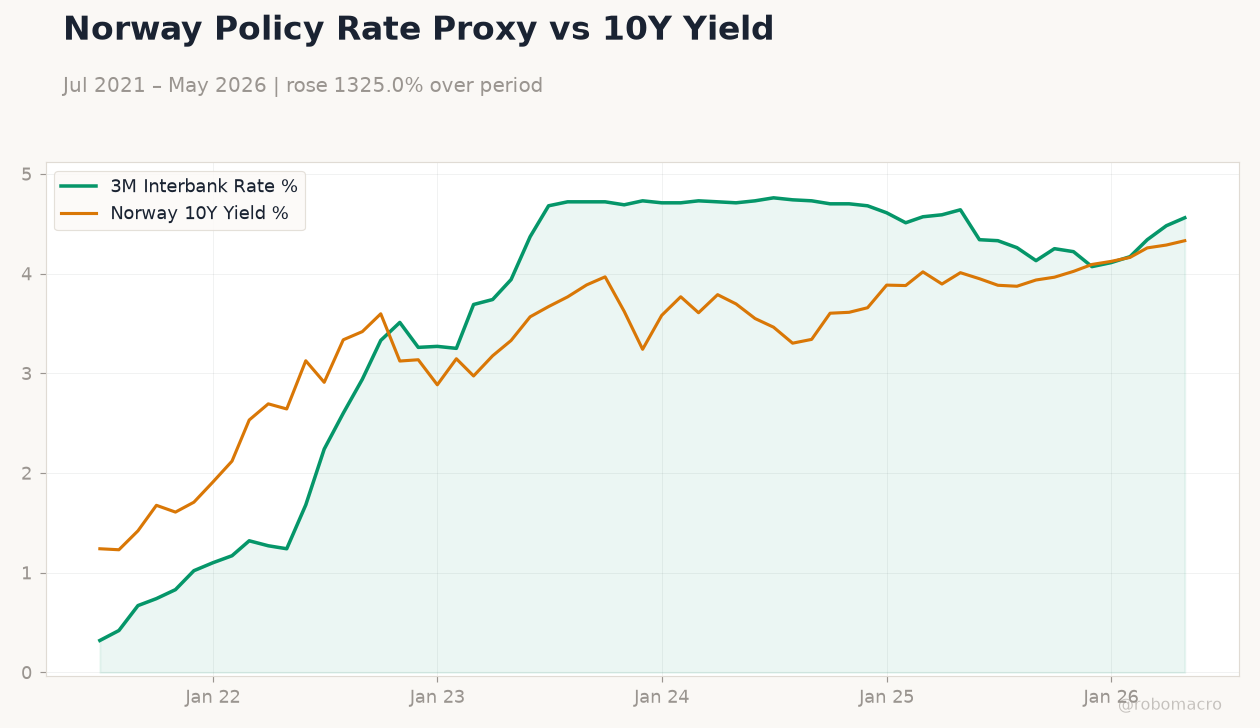

| Norges Bank Interest Rate Decision | 4.25 | 4.25 | 4.25 |

Sweden Policy Rate Proxy vs 10Y Yield | Type: macro_line | 3M Interbank Rate %: 1.957 (2026-05-01) | Range: -0.3847–4.102 | Trend(6pt): -0.1551,1.51,4.102,2.331,1.936,1.957 | Sweden 10Y Yield %: 2.745 (2026-05-01) | Range: 0.1101–3.024 | Trend(6pt): 0.1808,2.077,2.755,2.321,2.764,2.745

Sweden Policy Rate Proxy vs 10Y Yield | Type: macro_line | 3M Interbank Rate %: 1.957 (2026-05-01) | Range: -0.3847–4.102 | Trend(6pt): -0.1551,1.51,4.102,2.331,1.936,1.957 | Sweden 10Y Yield %: 2.745 (2026-05-01) | Range: 0.1101–3.024 | Trend(6pt): 0.1808,2.077,2.755,2.321,2.764,2.745

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Riksbank holds policy rate at 1.75% while Norges Bank keeps rate at 4.25% with hawkish guidance.

- OMX Stockholm rises 0.55% but Oslo Bors falls 1.25% as USD/NOK jumps 1.50% to 9.76.

- Swedish finance minister defends growth outlook amid Riksbank comments on possible future hike.

Yesterday's Recap

The Riksbank left its policy rate unchanged at 1.75% and held a press conference that highlighted risks of a later hike. Norges Bank also kept its rate at 4.25%, delivering a hawkish hold that analysts linked to August tightening prospects. OMX Stockholm 30 closed at 3,178.64 after a 0.55% gain while Oslo Bors fell 1.25% to 1,927.39.

USD/SEK rose 0.97% to 9.60 and USD/NOK climbed 1.50% to 9.76 amid broader dollar strength. Sweden’s 10-year yield fell 1.45% to 2.74% while Norway’s 10-year yield rose 1.01% to 4.33%. The Swedish finance minister reiterated the government’s 2.3% GDP forecast despite softer inflation prints.

Brent crude edged up 0.55% to 80.29, providing limited support to the Norwegian krone.

The Day Ahead

No tier-1 Nordic data releases are scheduled for today or tomorrow. Markets will monitor any follow-up comments from Riksbank or Norges Bank officials. Equity trading is expected to remain thin ahead of the weekend.

Currency traders will watch USD/SEK and USD/NOK for continuation of yesterday’s moves. Oil price developments will remain key for NOK direction given Norway’s export exposure.

Other Economic Notes

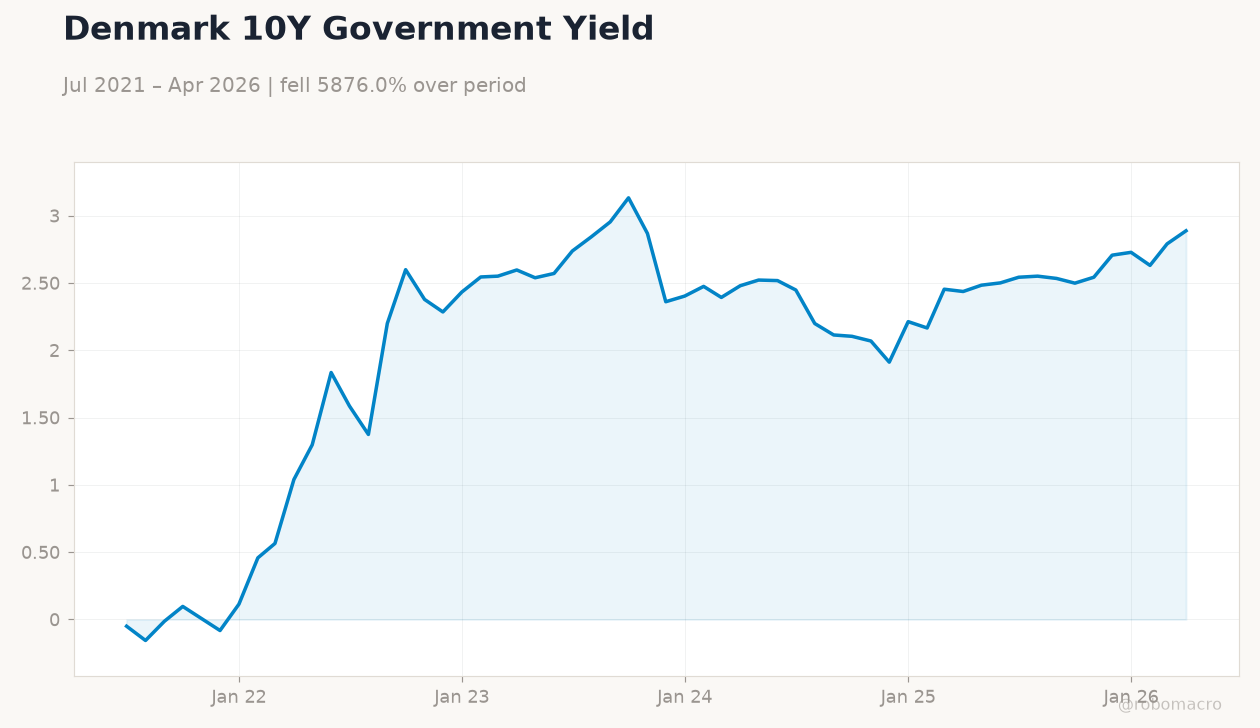

Swedish housing starts continued to contract while prices showed tentative stabilization. Norway’s oil production shortfall trims expected fiscal revenue and limits krone support. Denmark’s manufacturing exports remain sensitive to euro-area demand given the ERM II peg.

Finland’s eurozone membership transmits ECB policy directly to domestic borrowing costs without independent rate setting.

Global Macro News

The ECB maintains its deposit rate at 2.25%, leaving Nordic central banks with divergent paths. Eurozone unemployment stands at 6.70%, supporting a cautious ECB stance. Global energy price pressures continue to feed into Nordic inflation readings.

Dollar strength against both krona and krone reflects wider yield differentials versus the United States. <i>↓ p.2</i>