Nordics Macro Daily(Beta Mode)

Nordic Equities Split as NOK Slips on Brent Drop

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,178.64 | +0.55% |

| Oslo Bors | 1,950.43 | +1.20% |

| OMX Copenhagen 25 | 1,774.92 | +1.77% |

| OMX Helsinki 25 | 6,238.40 | -1.35% |

| USD/SEK | 9.58 | +0.77% |

| USD/NOK | 9.74 | +1.35% |

| EUR/SEK | 10.99 | +0.07% |

| EUR/NOK | 11.11 | -0.47% |

| Brent Crude | 78.93 | -1.15% |

| Gold | 4,214.00 | -0.24% |

| Bitcoin | 64,119.61 | -0.19% |

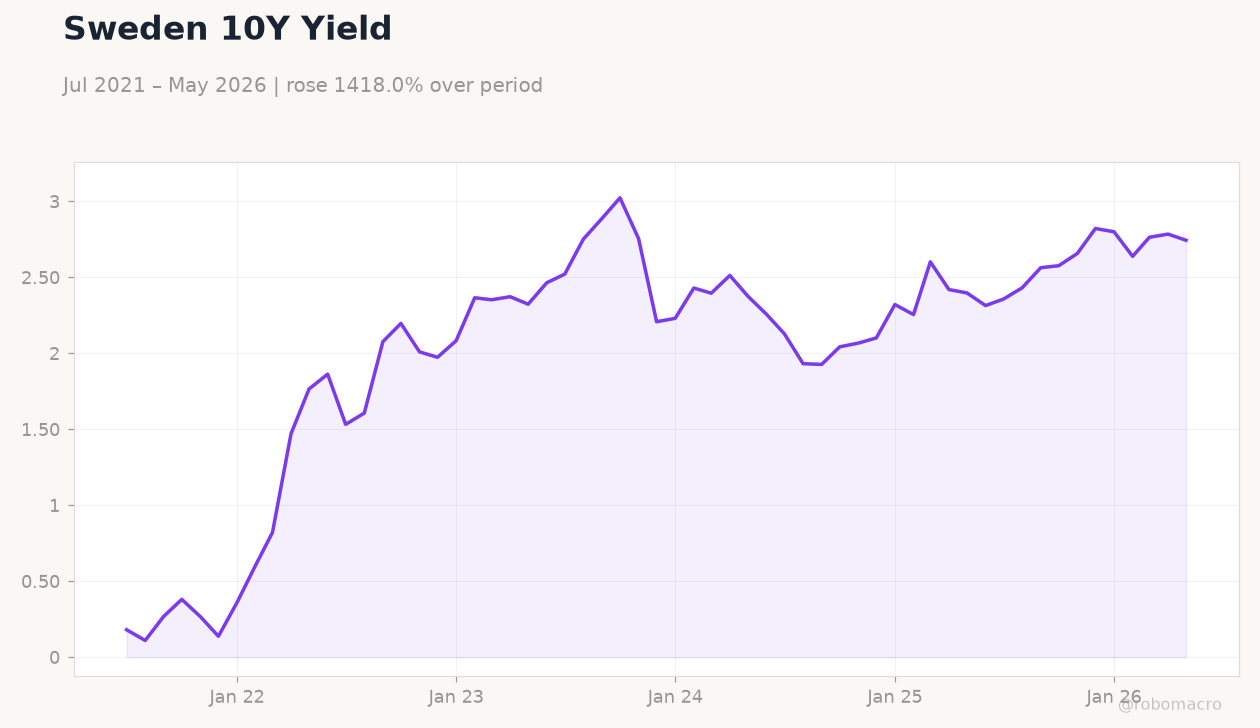

| Sweden 10Y Govt Yield | 2.74% | -1.45% |

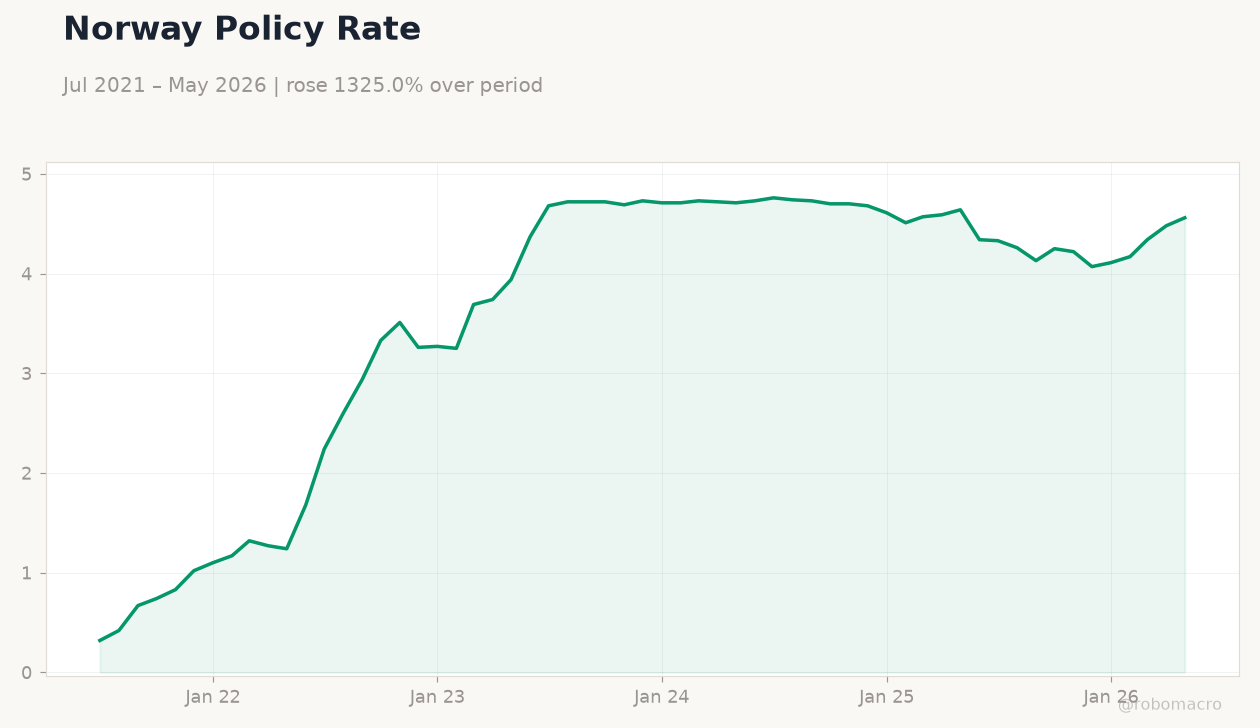

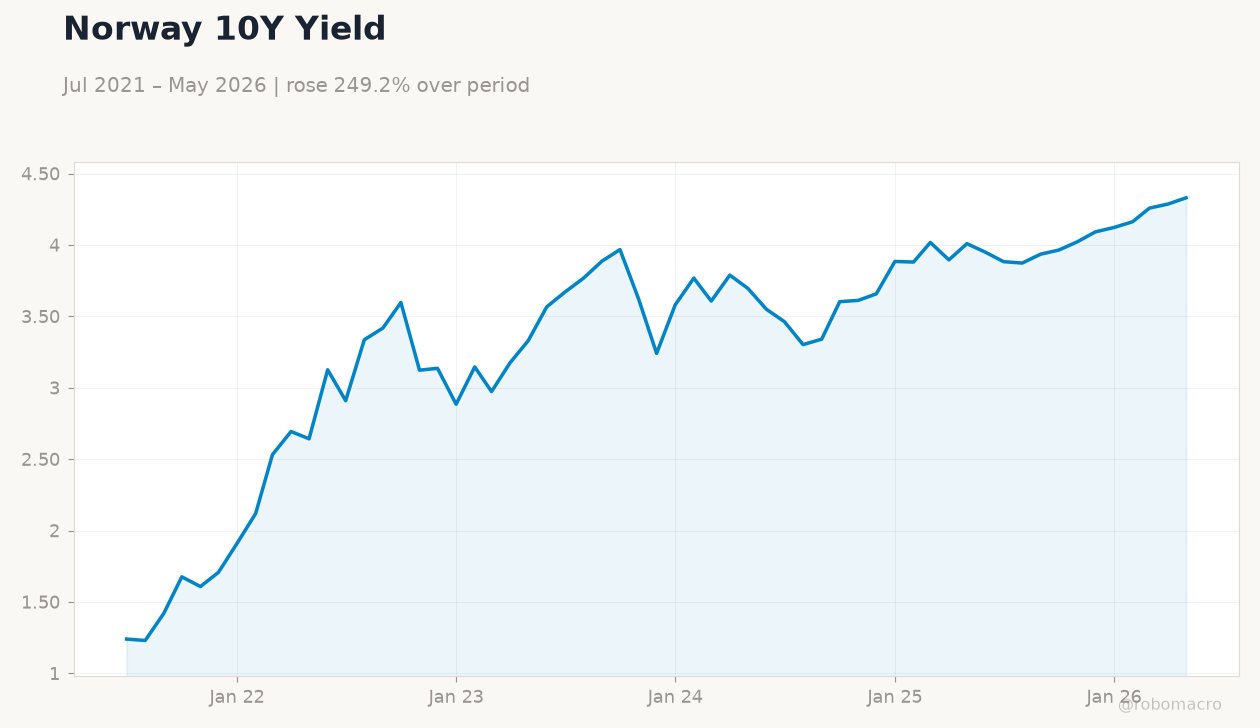

| Norway 10Y Govt Yield | 4.33% | +1.01% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

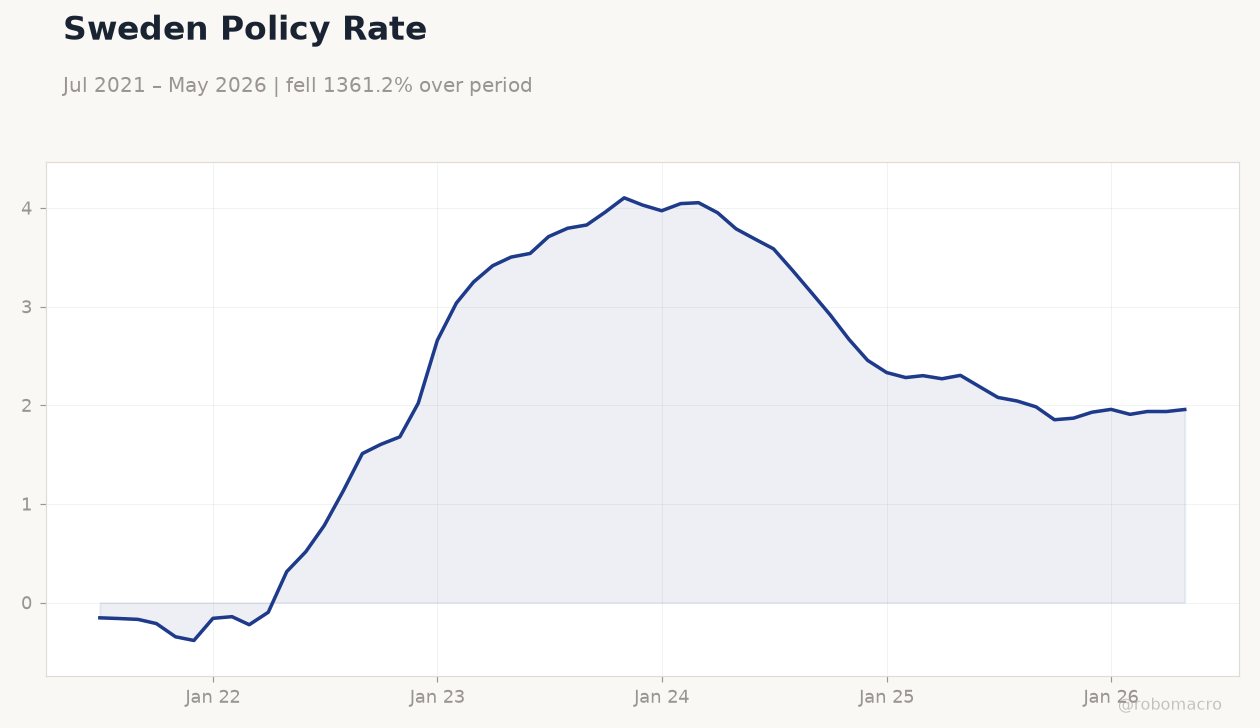

Sweden Policy Rate | Type: macro_line | %: 1.957 (2026-05-01) | Range: -0.3847–4.102 | Trend(6pt): -0.1551,1.51,4.102,2.331,1.936,1.957

Sweden Policy Rate | Type: macro_line | %: 1.957 (2026-05-01) | Range: -0.3847–4.102 | Trend(6pt): -0.1551,1.51,4.102,2.331,1.936,1.957

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Nordic equity markets posted mixed results, with Copenhagen and Oslo advancing while Helsinki declined on euro-area concerns.

- USD/NOK rose 1.35% to 9.74 and USD/SEK climbed 0.77% to 9.58 as Brent crude fell 1.15% to 78.93.

- Norges Bank held its policy rate steady while the ECB deposit rate remained at 2.25%, underscoring regional policy divergence.

Yesterday's Recap

Nordic equity indices closed with clear divergence. OMX Copenhagen 25 gained 1.77% to 1,774.92 while Oslo Bors rose 1.20% to 1,950.43, supported by energy exposure. OMX Stockholm 30 advanced 0.55% to 3,178.64, but OMX Helsinki 25 fell 1.35% to 6,238.40 amid softer euro-zone sentiment.

The Norwegian krone weakened notably, with USD/NOK up 1.35% to 9.74 and EUR/NOK down 0.47% to 11.11. Sweden 10-year yields declined 1.45% to 2.74% while Norway 10-year yields rose 1.01% to 4.33%. No macroeconomic data releases occurred across Sweden, Norway, Denmark or Finland.

Brent’s decline weighed on NOK sentiment given Norway’s oil-export reliance.

The Day Ahead

No scheduled economic releases are listed for Sweden, Norway, Denmark or Finland. Markets will likely monitor external drivers including euro-area sentiment and oil-price developments. Norges Bank’s recent hold leaves focus on incoming inflation prints next week.

Danish and Finnish data calendars remain light, consistent with the peg and ECB policy transmission. Equity and FX flows may react to any shifts in global risk appetite. Participants will also track any comments from Riksbank officials on the recent CPIF upside surprise.

Other Economic Notes

Sweden’s export-oriented manufacturing sector faces headwinds from softer external demand. Norway’s oil-fund outlook remains sensitive to Brent fluctuations around 79 dollars. Denmark’s shipping sector reported stable container rates, supporting the current-account surplus.

Finnish retail sales aligned with expectations, offering limited new signals on household spending. Housing starts in Sweden continued their multi-year contraction, weighing on construction activity.

Global Macro News

The UK economy contracted for the first time since last August, raising questions about external demand for Nordic exports. Russia’s central bank cut its key rate following an economic contraction, illustrating divergent policy paths outside the euro area. The ECB maintained its deposit rate at 2.25% while favouring greater cross-border banking integration.

<i>↓ p.2</i>