Nordics Macro Daily(Beta Mode)

Nordic Equities Diverge as Currencies Weaken

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,190.72 | +0.38% |

| Oslo Bors | 1,946.67 | -0.19% |

| OMX Copenhagen 25 | 1,791.76 | +2.73% |

| OMX Helsinki 25 | 6,325.50 | +1.40% |

| USD/SEK | 9.65 | +0.60% |

| USD/NOK | 9.75 | +0.52% |

| EUR/SEK | 10.99 | +0.09% |

| EUR/NOK | 11.14 | +0.18% |

| Brent Crude | 76.80 | -1.41% |

| Gold | 4,133.50 | -1.16% |

| Bitcoin | 62,880.28 | -1.68% |

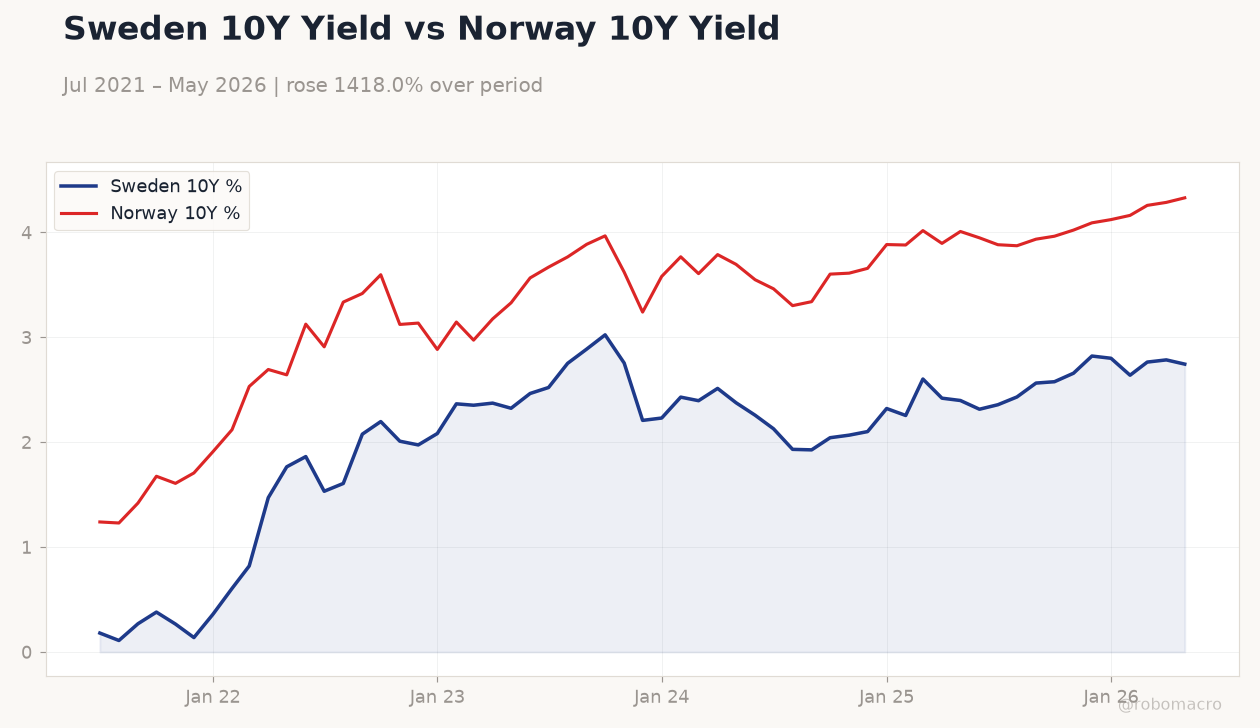

| Sweden 10Y Govt Yield | 2.74% | -1.45% |

| Norway 10Y Govt Yield | 4.33% | +1.01% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Sweden 10Y Yield vs Norway 10Y Yield | Type: macro_line | Sweden 10Y %: 2.745 (2026-05-01) | Range: 0.1101–3.024 | Trend(6pt): 0.1808,2.077,2.755,2.321,2.764,2.745 | Norway 10Y %: 4.33 (2026-05-01) | Range: 1.23–4.33 | Trend(6pt): 1.24,3.418,3.622,3.884,4.258,4.33

Sweden 10Y Yield vs Norway 10Y Yield | Type: macro_line | Sweden 10Y %: 2.745 (2026-05-01) | Range: 0.1101–3.024 | Trend(6pt): 0.1808,2.077,2.755,2.321,2.764,2.745 | Norway 10Y %: 4.33 (2026-05-01) | Range: 1.23–4.33 | Trend(6pt): 1.24,3.418,3.622,3.884,4.258,4.33

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- OMX Copenhagen 25 surged 2.73% while Oslo Bors fell 0.19% on Brent decline

- USD/SEK rose 0.60% to 9.65 and USD/NOK gained 0.52% to 9.75

- Sweden 10Y yield fell 1.45% to 2.74% as Norway 10Y yield rose 1.01% to 4.33%

Yesterday's Recap

Nordic equity markets closed mixed on 22 June with no major data releases across the bloc. Sweden’s OMX Stockholm 30 advanced 0.38% to 3,190.72 amid lower government bond yields. Norway’s Oslo Bors declined 0.19% to 1,946.67 as Brent crude fell 1.41% to 76.80, weighing on energy-exposed shares.

Denmark’s OMX Copenhagen 25 jumped 2.73% to 1,791.76 while Finland’s OMX Helsinki 25 gained 1.40% to 6,325.50. The Swedish krona weakened with USD/SEK up 0.60% to 9.65 and EUR/SEK rising 0.09% to 10.99. Norway’s krone also softened as USD/NOK increased 0.52% to 9.75 and EUR/NOK rose 0.18% to 11.14.

Ten-year yields diverged, with Sweden’s falling 1.45% to 2.74% while Norway’s rose 1.01% to 4.33%. Gold declined 1.16% to 4,133.50 and Bitcoin fell 1.68% to 62,880.28.

The Day Ahead

No economic releases are scheduled for Sweden, Norway, Denmark or Finland on 23 June. Markets will focus on global risk sentiment and any follow-through from yesterday’s equity moves. Norway’s NOK 4.5 bn nominal bond auction is the only notable domestic event.

Traders will monitor Brent crude for further impact on Norwegian fiscal flows. Quiet conditions are expected ahead of the weekend.

Other Economic Notes

The eurozone economy contracted according to recent reports, creating headwinds for export-oriented Nordic manufacturers in Sweden and Denmark. UK GDP contraction for the first time since last August adds to external demand concerns for the region. Poland’s business sentiment signals caution, indirectly affecting Nordic trade links in the Baltic area.

Broader global risk-off moves pressured Bitcoin and gold, though Nordic equities showed resilience in Copenhagen and Helsinki. Norway’s Scatec plans up to $5bn in new green energy investments in Egypt over the next two years.

Global Macro News

Eurozone contraction raised questions about ECB policy transmission to Finland. UK economic contraction weighed on risk assets. Weak monsoon risks in India highlighted commodity price volatility relevant to Norwegian energy exports.

<i>↓ p.2</i>