Nordics Macro Daily(Beta Mode)

Nordic Equities Slide as Krona Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,145.66 | -1.41% |

| Oslo Bors | 1,944.97 | -0.09% |

| OMX Copenhagen 25 | 1,790.48 | -0.07% |

| OMX Helsinki 25 | 6,216.15 | -1.73% |

| USD/SEK | 9.75 | +1.33% |

| USD/NOK | 9.81 | +1.27% |

| EUR/SEK | 11.08 | +0.78% |

| EUR/NOK | 11.15 | +0.70% |

| Brent Crude | 76.42 | -0.86% |

| Gold | 4,102.50 | -0.66% |

| Bitcoin | 62,765.60 | +0.16% |

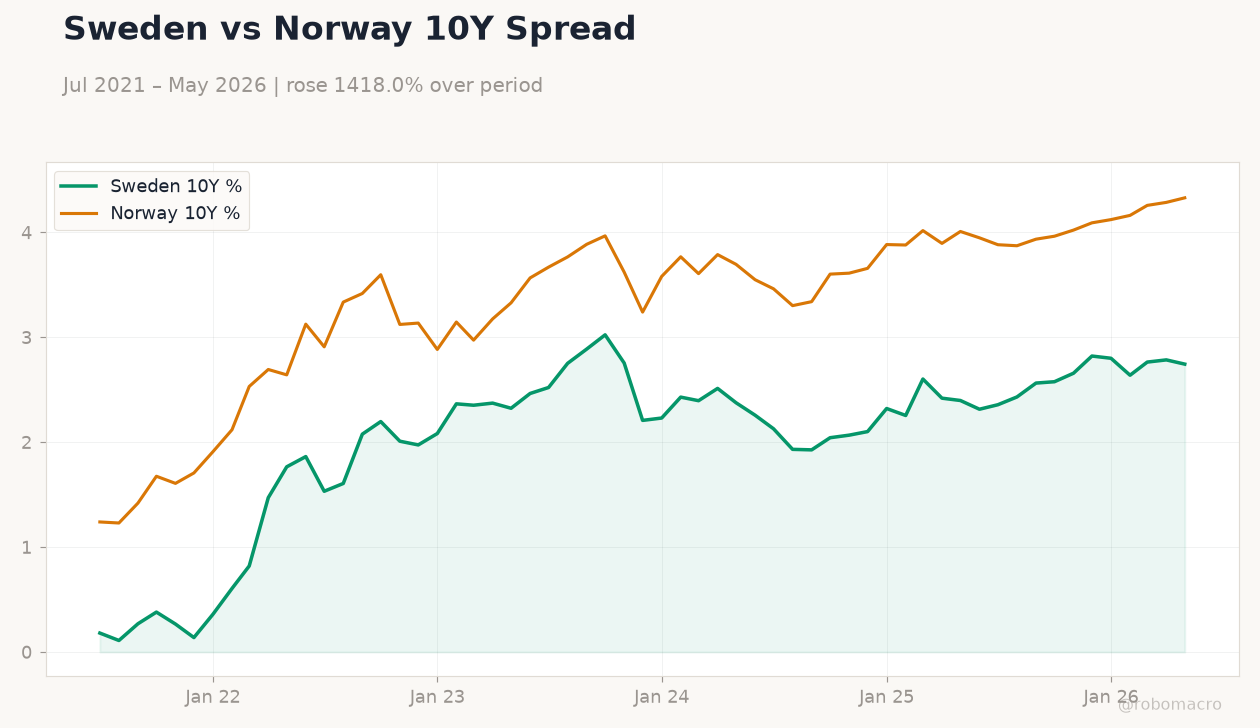

| Sweden 10Y Govt Yield | 2.74% | -1.45% |

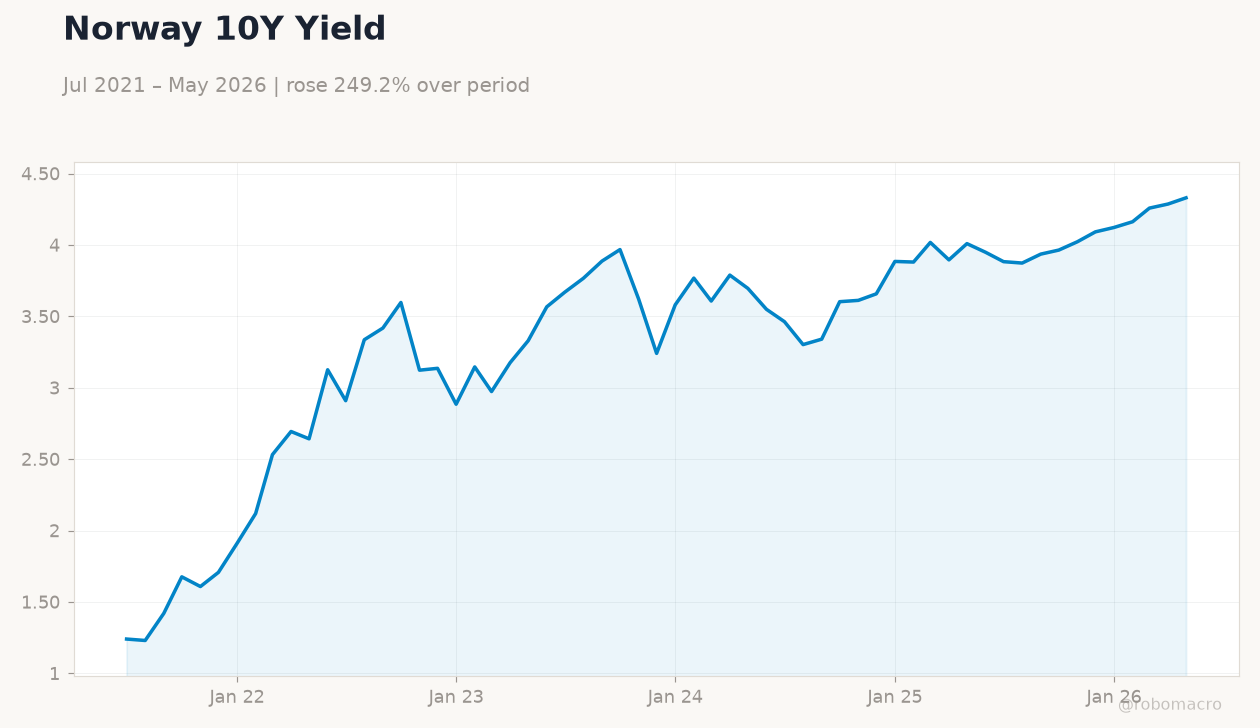

| Norway 10Y Govt Yield | 4.33% | +1.01% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

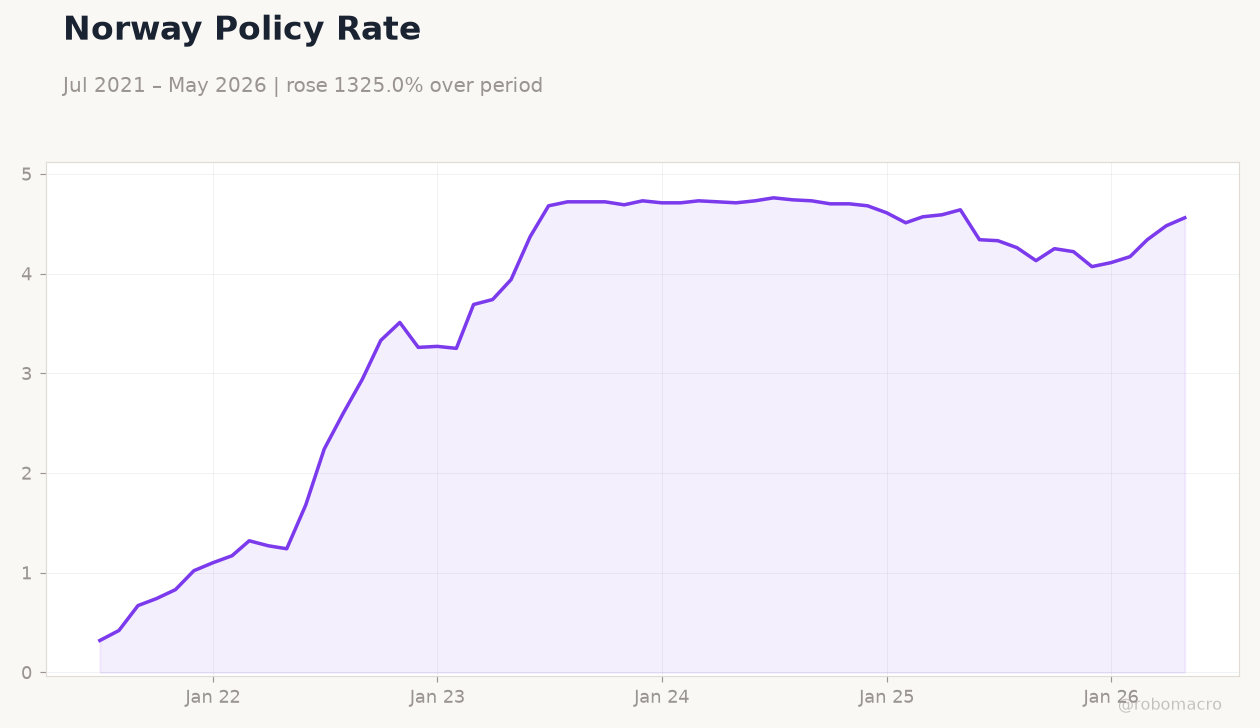

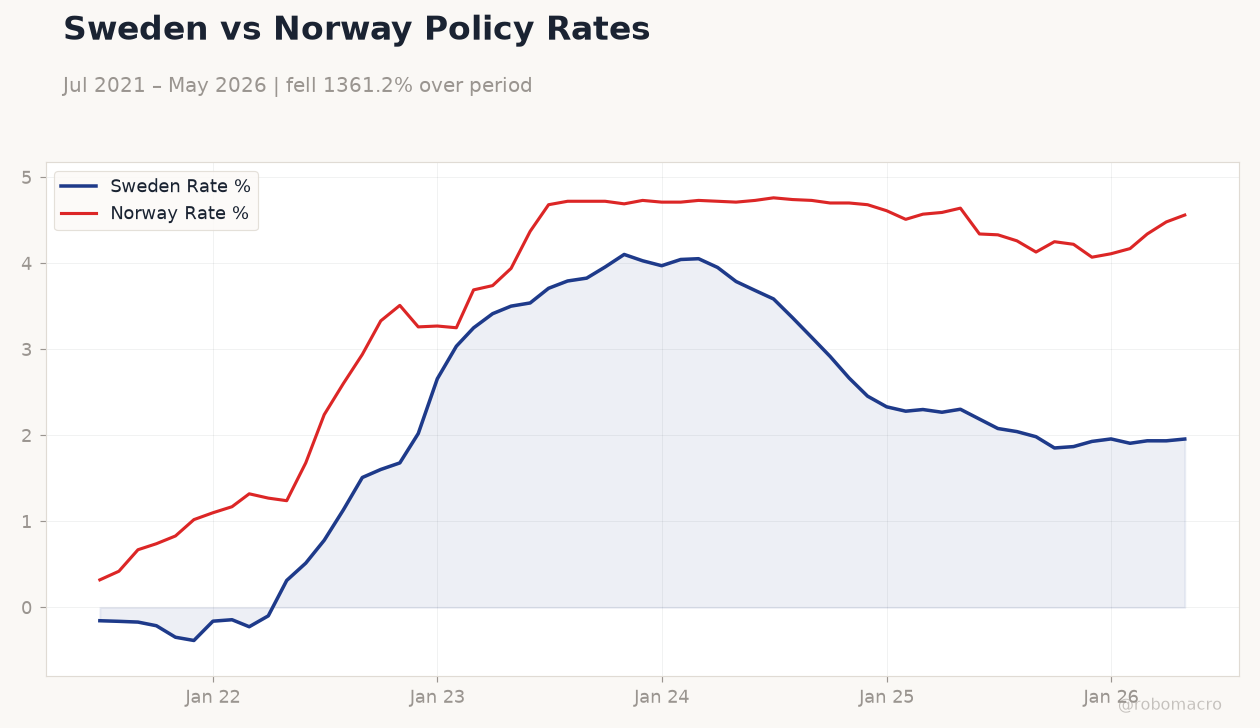

Sweden vs Norway Policy Rates | Type: macro_line | Sweden Rate %: 1.957 (2026-05-01) | Range: -0.3847–4.102 | Trend(6pt): -0.1551,1.51,4.102,2.331,1.936,1.957 | Norway Rate %: 4.56 (2026-05-01) | Range: 0.32–4.76 | Trend(6pt): 0.32,2.94,4.69,4.61,4.34,4.56

Sweden vs Norway Policy Rates | Type: macro_line | Sweden Rate %: 1.957 (2026-05-01) | Range: -0.3847–4.102 | Trend(6pt): -0.1551,1.51,4.102,2.331,1.936,1.957 | Norway Rate %: 4.56 (2026-05-01) | Range: 0.32–4.76 | Trend(6pt): 0.32,2.94,4.69,4.61,4.34,4.56

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- OMX Stockholm 30 fell 1.41% to 3,145.66 while OMX Helsinki 25 dropped 1.73%, led by rate-sensitive sectors.

- USD/SEK rose 1.33% to 9.75 and USD/NOK gained 1.27% to 9.81 amid broad dollar strength.

- Sweden 10-year yield fell 1.45% to 2.74% as Riksbank minutes signal potential policy splits.

Yesterday's Recap

Nordic equity markets closed lower on 23 June, with Sweden’s OMX Stockholm 30 declining 1.41% to 3,145.66 and Finland’s OMX Helsinki 25 falling 1.73% to 6,216.15. Norway’s Oslo Bors edged down 0.09% to 1,944.97 while Denmark’s OMX Copenhagen 25 slipped 0.07%. The Swedish krona weakened notably, with USD/SEK rising 1.33% to 9.75 and EUR/SEK up 0.78% to 11.08.

Norway’s krone also depreciated, pushing USD/NOK 1.27% higher to 9.81. Brent crude declined 0.86% to 76.42, weighing on Norwegian energy names. Sweden 10-year government yields fell 1.45% to 2.74% while Norway’s equivalent rose 1.01% to 4.33%.

Riksbank minutes released overnight pointed to internal divisions on the pace of future easing.

The Day Ahead

Trading desks expect a quiet session across Nordic markets with no major data releases scheduled for 24 June. Focus will remain on digestion of the latest Riksbank minutes and any follow-up comments from board members. Norway’s oil production figures and Norges Bank speeches could influence NOK flows later in the week.

Danish and Finnish markets are likely to track euro-area developments closely given the currency peg and ECB membership. Equity volumes may stay subdued ahead of month-end positioning.

Other Economic Notes

Swedish housing data continue to signal stabilisation rather than recovery, with starts remaining depressed year-on-year. Norwegian fiscal balances benefit from Brent near 76 despite recent softness, supporting the government’s 2026 surplus outlook. Export-oriented manufacturing in Sweden and Denmark faces mixed global demand signals, while Finland’s eurozone exposure keeps its cycle aligned with ECB policy.

Credit spreads in both Sweden and Norway stayed largely stable.

Global Macro News

The Bank of England cut its main rate by 25 basis points to 4.50% as UK growth stagnated. UK PMI readings showed the economy contracting for a second straight month. Saudi Arabia reported a V-shaped recovery after earlier shocks, while UAE growth forecasts were upgraded toward 6% for 2027-2029.

<i>↓ p.2</i>