Nordics Macro Daily(Beta Mode)

Nordic Stocks Gain as Swedish Trade Swings to Surplus

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,166.78 | +0.42% |

| Oslo Bors | 1,906.43 | +0.31% |

| OMX Copenhagen 25 | 1,805.14 | +0.24% |

| OMX Helsinki 25 | 6,150.40 | +0.11% |

| USD/SEK | 9.72 | -0.13% |

| USD/NOK | 9.95 | +0.22% |

| EUR/SEK | 11.08 | -0.02% |

| EUR/NOK | 11.34 | +0.31% |

| Brent Crude | 73.27 | +0.16% |

| Gold | 4,046.50 | +0.60% |

| Bitcoin | 59,448.68 | -1.15% |

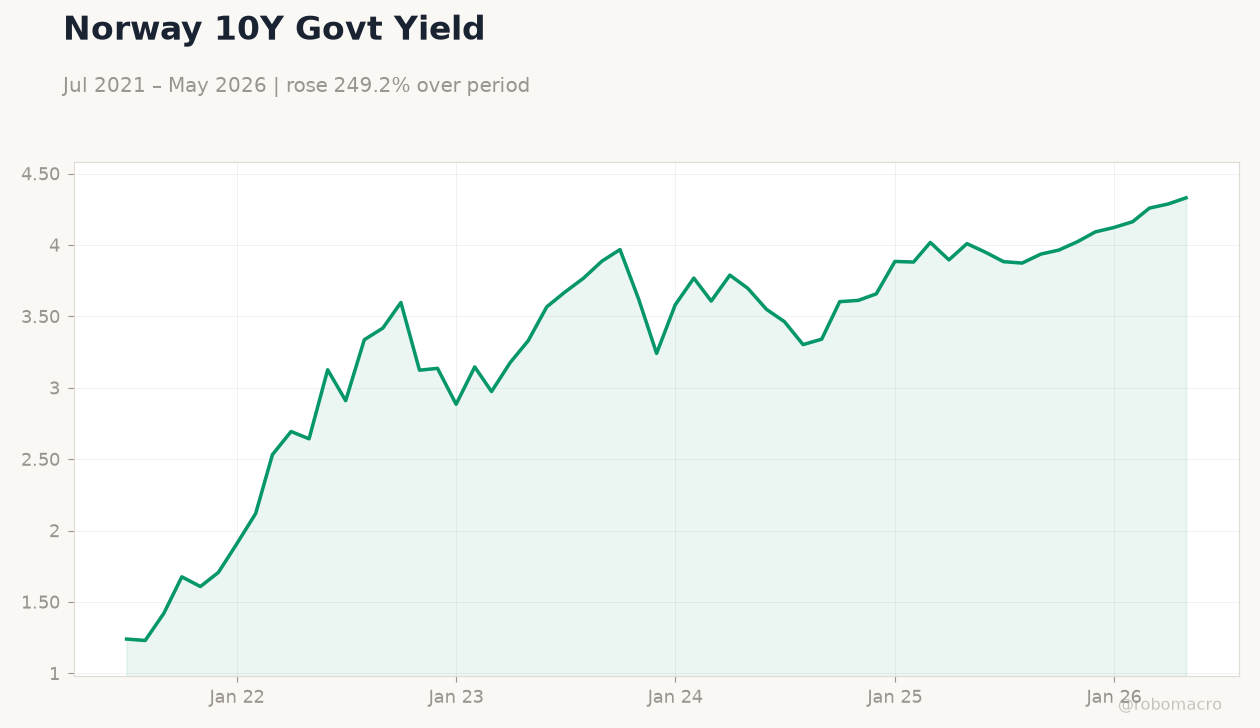

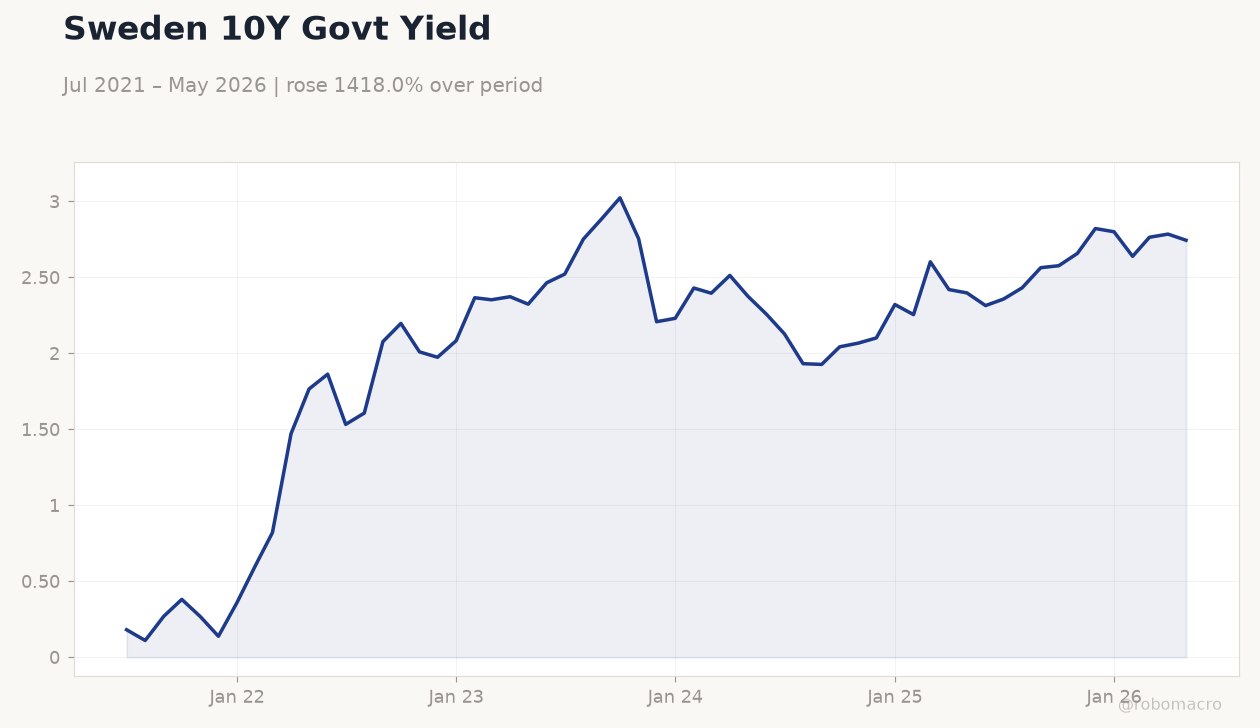

| Sweden 10Y Govt Yield | 2.74% | -1.45% |

| Norway 10Y Govt Yield | 4.33% | +1.01% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Sweden 10Y Govt Yield | Type: macro_line | Yield %: 2.745 (2026-05-01) | Range: 0.1101–3.024 | Trend(6pt): 0.1808,2.077,2.755,2.321,2.764,2.745

Sweden 10Y Govt Yield | Type: macro_line | Yield %: 2.745 (2026-05-01) | Range: 0.1101–3.024 | Trend(6pt): 0.1808,2.077,2.755,2.321,2.764,2.745

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Nordic equities advanced modestly with Stockholm leading gains

- Sweden trade balance swung to May surplus reversing prior deficit

- Riksbank certificate buybacks proceed amid stable policy outlook

Yesterday's Recap

Nordic equity markets posted gains on June 29 with the OMX Stockholm 30 climbing 0.42% to 3,166.78 while Oslo Bors added 0.31% to 1,906.43. The OMX Copenhagen 25 rose 0.24% to 1,805.14 and OMX Helsinki 25 edged 0.11% higher to 6,150.40. Sweden’s trade balance shifted to a surplus in May after recording a sharp deficit the prior month, lending support to the krona as USD/SEK declined 0.13% to 9.72.

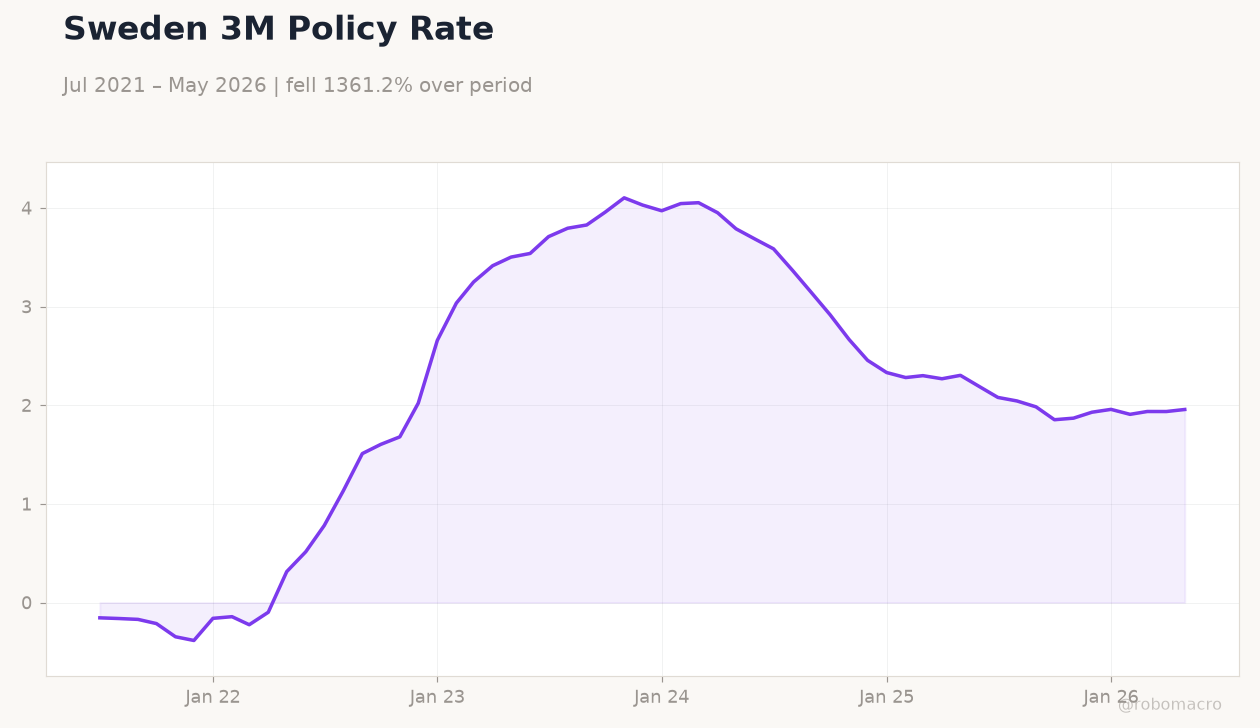

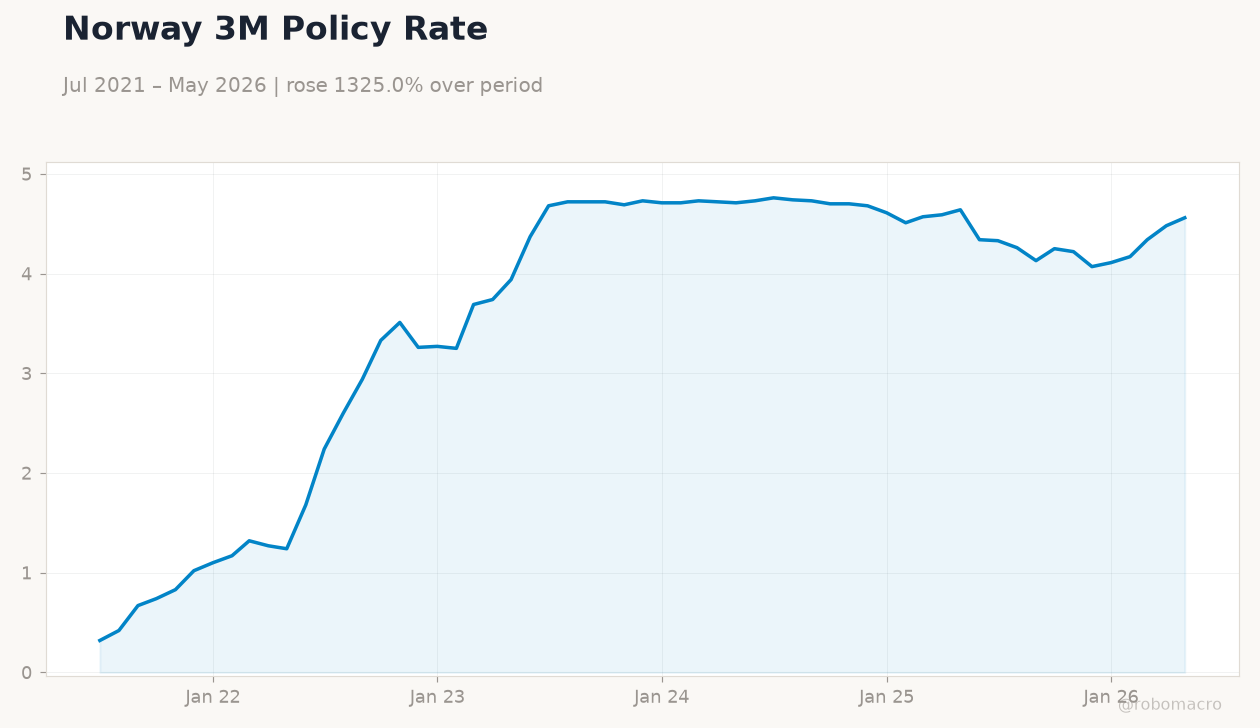

USD/NOK increased 0.22% to 9.95 alongside Brent crude at 73.27 while Swedish 10-year yields fell 1.45% to 2.74% and Norwegian 10-year yields rose 1.01% to 4.33%. The Riksbank executed further buybacks of certificates with no major economic data releases recorded across the region.

The Day Ahead

Markets face a data-empty July 1 with no scheduled releases across Sweden, Norway, Denmark or Finland. Focus will remain on external drivers including oil price movements that influence Norway’s fiscal and currency outlook. Export-oriented sectors in Sweden and Denmark may respond to any shifts in global demand indicators.

Finland continues to track eurozone developments given its ECB membership. Denmark maintains its ERM II peg to the euro without fresh intervention signals expected. Thin volumes could persist ahead of the holiday period.

Other Economic Notes

Sweden’s May trade surplus underscores resilience in its manufacturing export base despite earlier weakness. Norway benefits from stable Brent levels that support above-budget petroleum revenues and structural NOK strength. Equity gains across the region reflect contained domestic pressures with gold rising 0.60% to 4,046.50 signaling broader caution.

Housing market data remain absent but prior Swedish price increases point to gradual stabilization. Bitcoin’s 1.15% decline to 59,448.68 had negligible direct Nordic macro impact.

Global Macro News

Global risk sentiment stayed constructive for Nordic assets with modest equity advances mirroring broader developed-market trends. Oil price stability at 73.27 limited upside for the Norwegian krone while supporting fiscal projections. Gold’s advance to 4,046.50 highlighted ongoing safe-haven demand that can weigh on higher-beta currencies such as the NOK.

UK growth revisions lower offered little direct spillover to Nordic exports. <i>↓ p.2</i>