Nordics Macro Daily(Beta Mode)

Sweden PMI Beat Lifts Krona, Rate-Hike Odds

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,178.24 | -0.21% |

| Oslo Bors | 1,899.32 | -0.13% |

| OMX Copenhagen 25 | 1,856.55 | +0.51% |

| OMX Helsinki 25 | 6,138.35 | -0.12% |

| USD/SEK | 9.71 | -0.03% |

| USD/NOK | 9.91 | -0.02% |

| EUR/SEK | 11.07 | -0.03% |

| EUR/NOK | 11.29 | -0.16% |

| Brent Crude | 70.40 | -1.63% |

| Gold | 4,081.50 | +0.32% |

| Bitcoin | 60,129.92 | +0.21% |

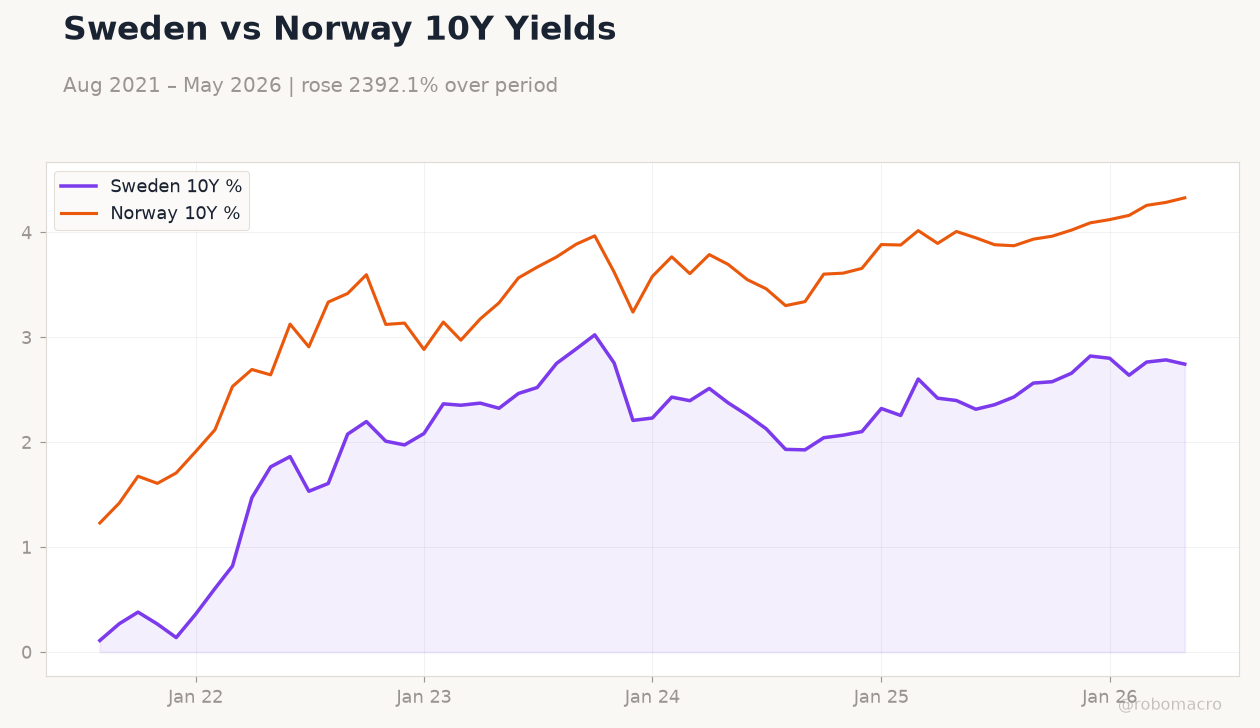

| Sweden 10Y Govt Yield | 2.74% | -1.45% |

| Norway 10Y Govt Yield | 4.33% | +1.01% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

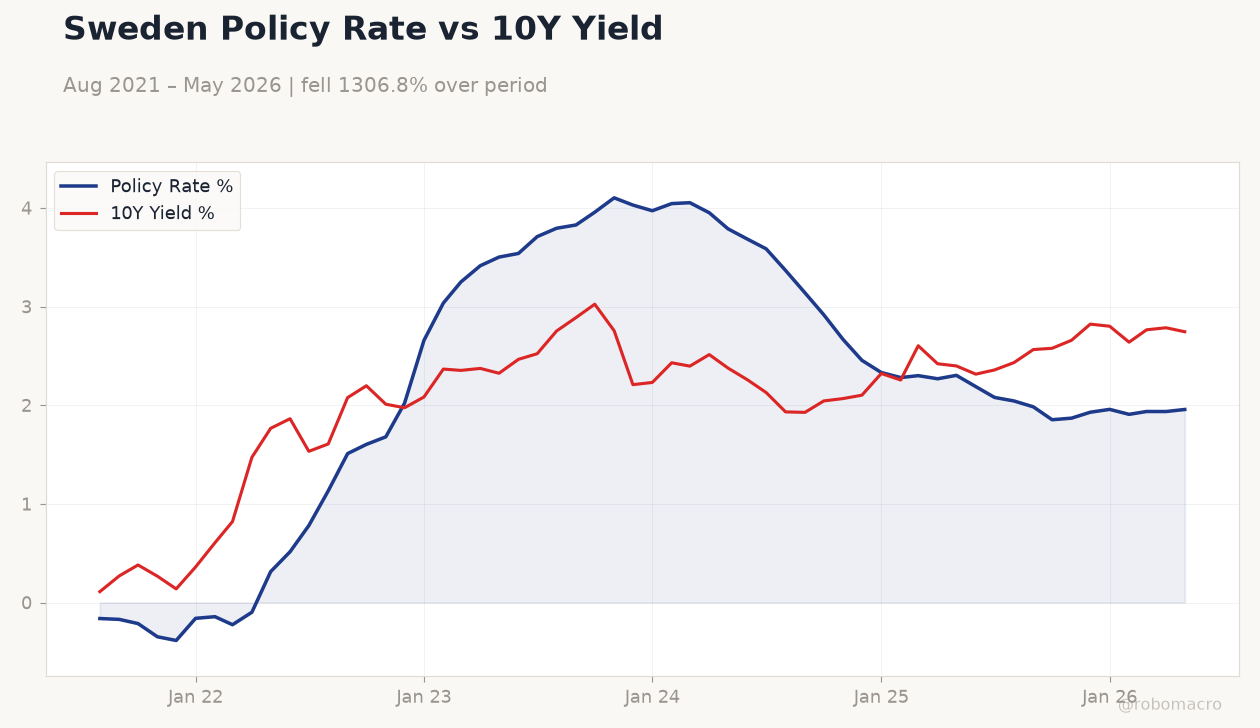

Sweden Policy Rate vs 10Y Yield | Type: macro_line | Policy Rate %: 1.957 (2026-05-01) | Range: -0.3847–4.102 | Trend(6pt): -0.1621,1.603,4.028,2.28,1.936,1.957 | 10Y Yield %: 2.745 (2026-05-01) | Range: 0.1101–3.024 | Trend(6pt): 0.1101,2.197,2.208,2.255,2.785,2.745

Sweden Policy Rate vs 10Y Yield | Type: macro_line | Policy Rate %: 1.957 (2026-05-01) | Range: -0.3847–4.102 | Trend(6pt): -0.1621,1.603,4.028,2.28,1.936,1.957 | 10Y Yield %: 2.745 (2026-05-01) | Range: 0.1101–3.024 | Trend(6pt): 0.1101,2.197,2.208,2.255,2.785,2.745

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Sweden manufacturing PMI climbed to 58.3, boosting rate-hike expectations and supporting the krona against modest equity declines.

- Nordic equities closed mixed with OMX Copenhagen 25 rising 0.51% while OMX Stockholm 30 fell 0.21% amid thin volumes.

- Brent crude dropped 1.63% to 70.40, pressuring Norway’s fiscal outlook while 10-year yields diverged across the region.

Yesterday's Recap

Sweden’s manufacturing PMI rose to 58.3, lifting krona and OMXS30 sentiment as markets priced higher odds of Riksbank tightening. OMX Stockholm 30 closed at 3,178.24, down 0.21%, while Oslo Bors slipped 0.13% to 1,899.32. OMX Copenhagen 25 advanced 0.51% to 1,856.55 and OMX Helsinki 25 eased 0.12% to 6,138.35.

USD/SEK held at 9.71 and USD/NOK at 9.91 with negligible moves. Sweden’s 10-year yield fell 1.45% to 2.74% while Norway’s 10-year yield rose 1.01% to 4.33%. Nordea flagged June core inflation likely exceeding Riksbank forecasts, reinforcing expectations for policy caution.

Brent’s decline weighed on Norwegian energy names without triggering broader krone weakness. No economic releases occurred in the Nordics on July 1.

The Day Ahead

Nordic calendars remain empty through July 3, leaving markets focused on external drivers and positioning ahead of next week’s inflation prints. Sweden retail sales data scheduled for July 4 will provide the first post-PMI gauge of consumer momentum. Norway will release June unemployment figures next week, though Norges Bank officials have signaled limited immediate reaction.

Danish and Finnish markets will track euro-area PMI revisions due mid-week. Thin summer liquidity may amplify any moves in EUR/SEK or EUR/NOK crosses.

Other Economic Notes

Export-oriented Swedish and Danish manufacturers stand to benefit from the PMI surge, supporting krona and equity outperformance versus peers. Norway’s oil revenue sensitivity remains elevated after Brent’s 1.63% drop, with fiscal transfers from the oil fund still tracking Norges Bank assumptions. Finnish activity stays anchored to ECB policy, limiting independent rate signals.

Housing data from Sweden showed modest stabilization but transaction volumes lag prior-year levels.

Global Macro News

Fed commentary from Warsh tempered inflation concerns, supporting risk assets and indirectly aiding Nordic export currencies. Yen weakness to 40-year lows raised imported inflation risks for import-dependent Nordic economies. <i>↓ p.2</i>