Nordics Macro Daily(Beta Mode)

Denmark Intervenes to Defend Krone Peg

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| OMX Stockholm 30 | 3,225.03 | +0.46% |

| Oslo Bors | 1,935.05 | +0.25% |

| OMX Copenhagen 25 | 1,891.56 | -0.23% |

| OMX Helsinki 25 | 6,214.80 | +0.69% |

| USD/SEK | 9.72 | +0.14% |

| USD/NOK | 9.82 | -0.92% |

| EUR/SEK | 11.06 | -0.17% |

| EUR/NOK | 11.28 | -0.29% |

| Brent Crude | 71.67 | -0.18% |

| Gold | 4,195.40 | +2.01% |

| Bitcoin | 61,680.01 | +0.32% |

| Sweden 10Y Govt Yield | 2.74% | -1.45% |

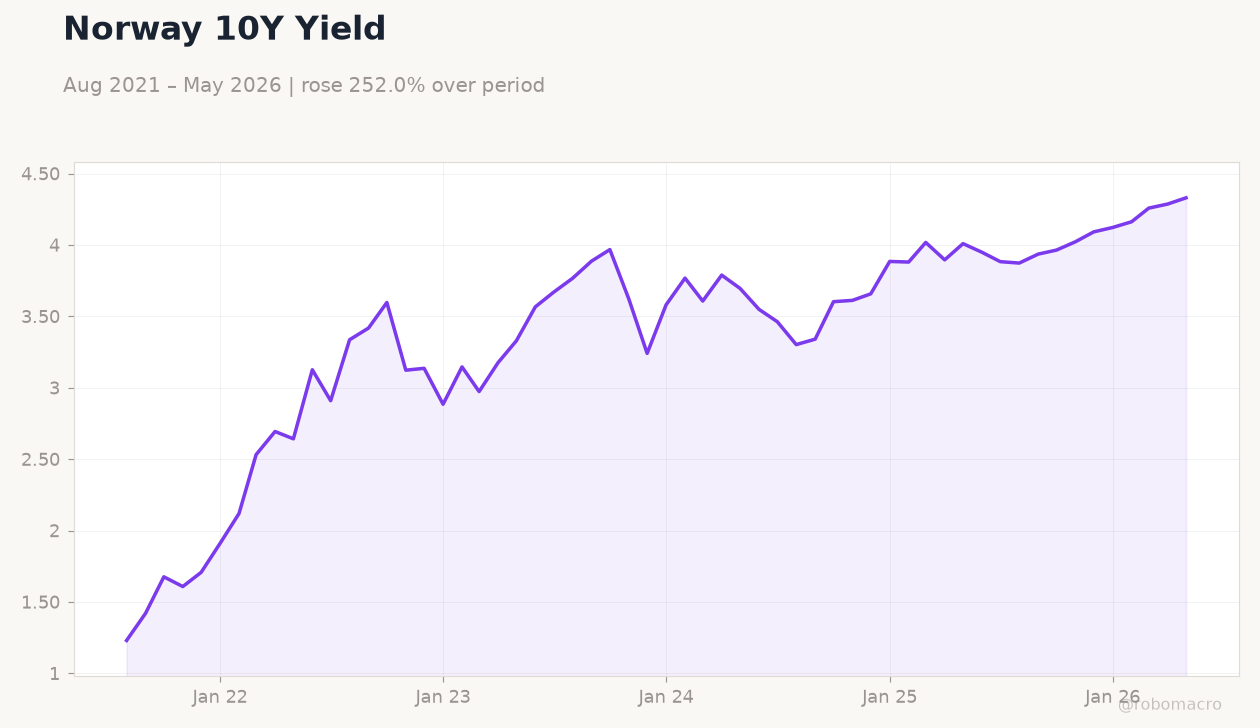

| Norway 10Y Govt Yield | 4.33% | +1.01% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

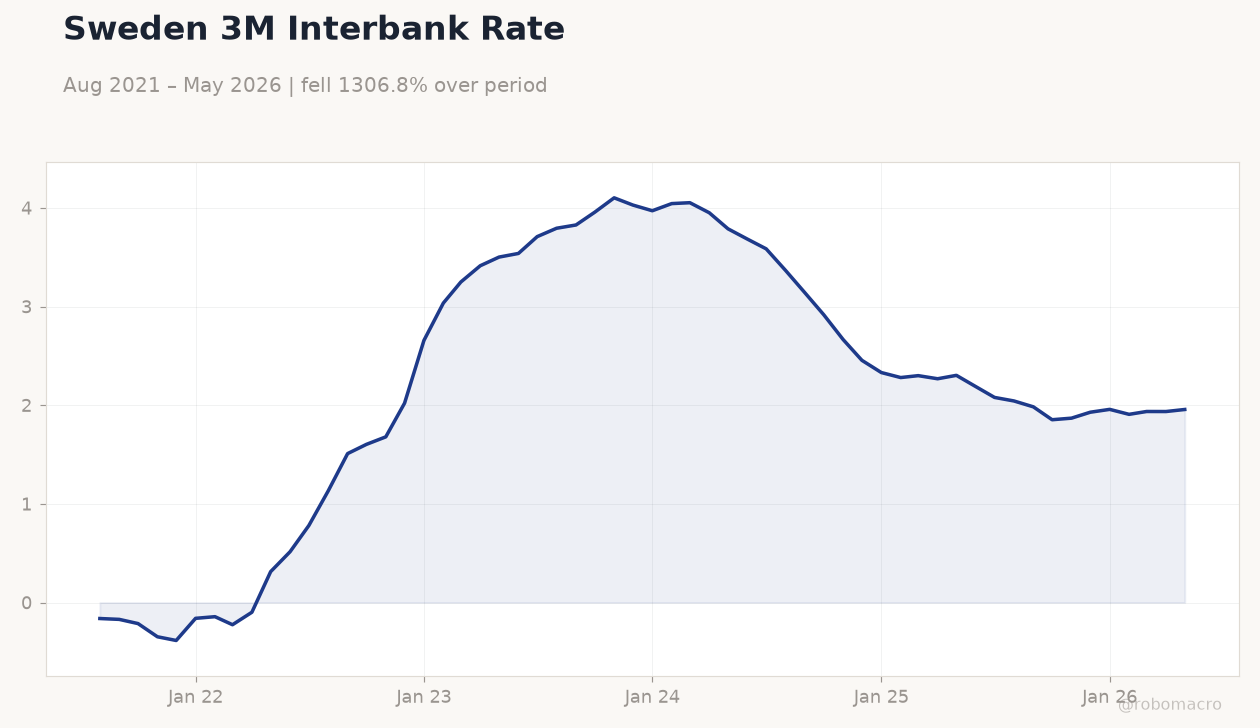

Sweden 3M Interbank Rate | Type: macro_line | Sweden 3M %: 1.957 (2026-05-01) | Range: -0.3847–4.102 | Trend(6pt): -0.1621,1.603,4.028,2.28,1.936,1.957

Sweden 3M Interbank Rate | Type: macro_line | Sweden 3M %: 1.957 (2026-05-01) | Range: -0.3847–4.102 | Trend(6pt): -0.1621,1.603,4.028,2.28,1.936,1.957

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Danmarks Nationalbank intervenes to defend EUR/DKK peg after krone hits weakest level.

- OMX Helsinki 25 leads gains at +0.69% while OMX Copenhagen 25 falls 0.23%.

- NOK strengthens sharply versus USD as Brent holds near $71.67 and regional yields diverge.

Yesterday's Recap

Nordic equity markets posted modest gains on July 2 with OMX Stockholm 30 rising 0.46% to 3,225.03 and Oslo Bors advancing 0.25% to 1,935.05. OMX Helsinki 25 climbed 0.69% to 6,214.80 while OMX Copenhagen 25 slipped 0.23% to 1,891.56. The Danish krone came under pressure, prompting Danmarks Nationalbank to intervene in FX markets to support the EUR/DKK peg.

USD/NOK fell 0.92% to 9.82 while USD/SEK edged up 0.14% to 9.72. EUR/SEK declined 0.17% to 11.06 and EUR/NOK fell 0.29% to 11.28. Sweden’s 10-year yield dropped 1.45% to 2.74% and Norway’s 10-year yield rose 1.01% to 4.33%.

Brent crude settled at 71.67, down 0.18%, providing limited support to Norway’s external balance. No major data releases occurred across the Nordic bloc.

The Day Ahead

The economic calendar remains empty for July 3-4 with no scheduled releases from Sweden, Norway, Denmark or Finland. Markets will monitor any follow-through from the Danish central bank’s krone intervention and ECB communications. Norges Bank will continue to track Brent dynamics given their direct impact on fiscal revenues and the krone.

Riksbank officials are expected to comment on recent inflation developments in coming days. Investors will also watch EUR/SEK and EUR/NOK for signs of further pressure on the Danish peg.

Other Economic Notes

Sweden and Denmark remain exposed to euro-area demand given their export-oriented manufacturing sectors. Norway’s oil revenue outlook stays supported near current Brent levels despite the modest daily decline. Finland continues to track ECB policy directly as a eurozone member.

Housing market data remain absent but Swedish covered-bond spreads stayed stable amid the yield decline. Broader Nordic credit conditions showed no material widening.

Global Macro News

Gold rose 2.01% to 4,195.40 on softer US data and lower oil prices, providing a safe-haven bid that indirectly supports Nordic currencies. Bitcoin gained 0.32% to 61,680.01 with limited spillover to risk assets in the region. Eurozone unemployment stood at 6.70% on the latest available reading, keeping ECB easing expectations in focus.

<i>↓ p.2</i>