South Africa Macro Daily(Beta Mode)

Oil Surge Batters Rand, Stocks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 111,842.41 | -5.85% |

| USD/ZAR | 16.50 | +2.67% |

| EUR/ZAR | 18.78 | -0.54% |

| Platinum | 2,107.00 | -8.86% |

| Gold | 5,135.10 | -3.01% |

| Brent Crude | 82.44 | +6.05% |

| Naspers | 86,521.00 | -2.27% |

| Bitcoin | 68,300.28 | -0.69% |

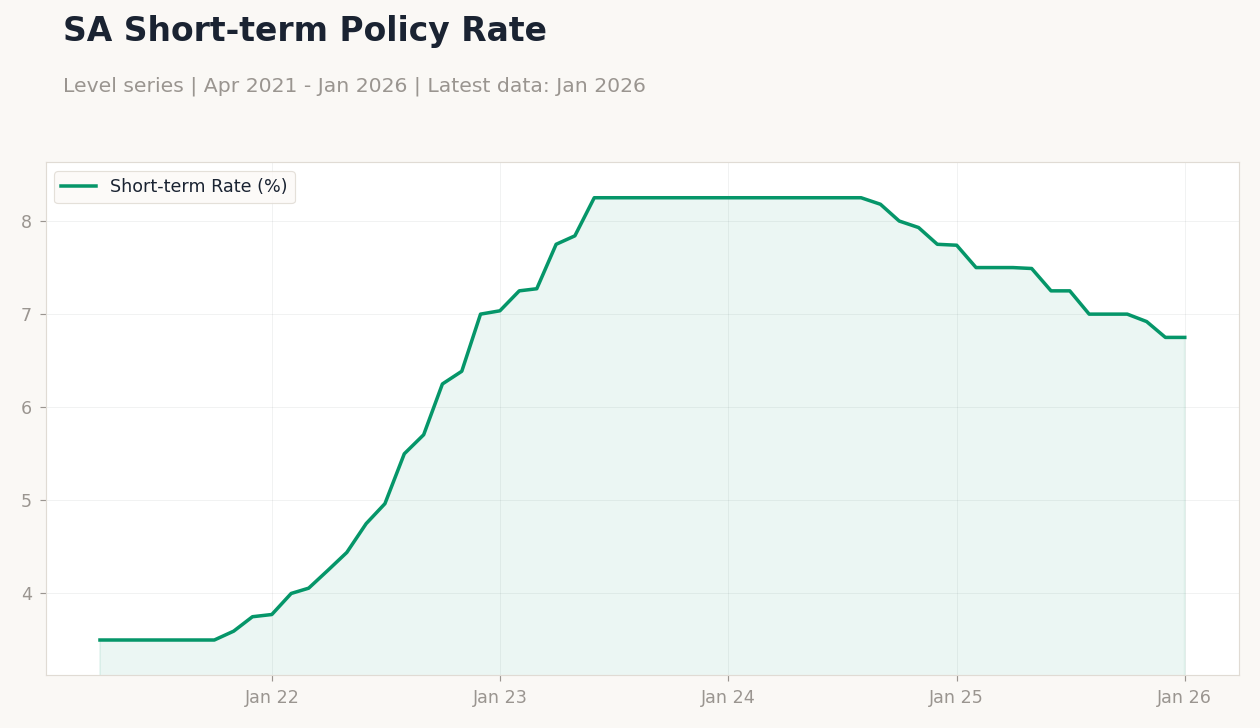

| South Africa Short-term Rate | 6.75% | +0.00% |

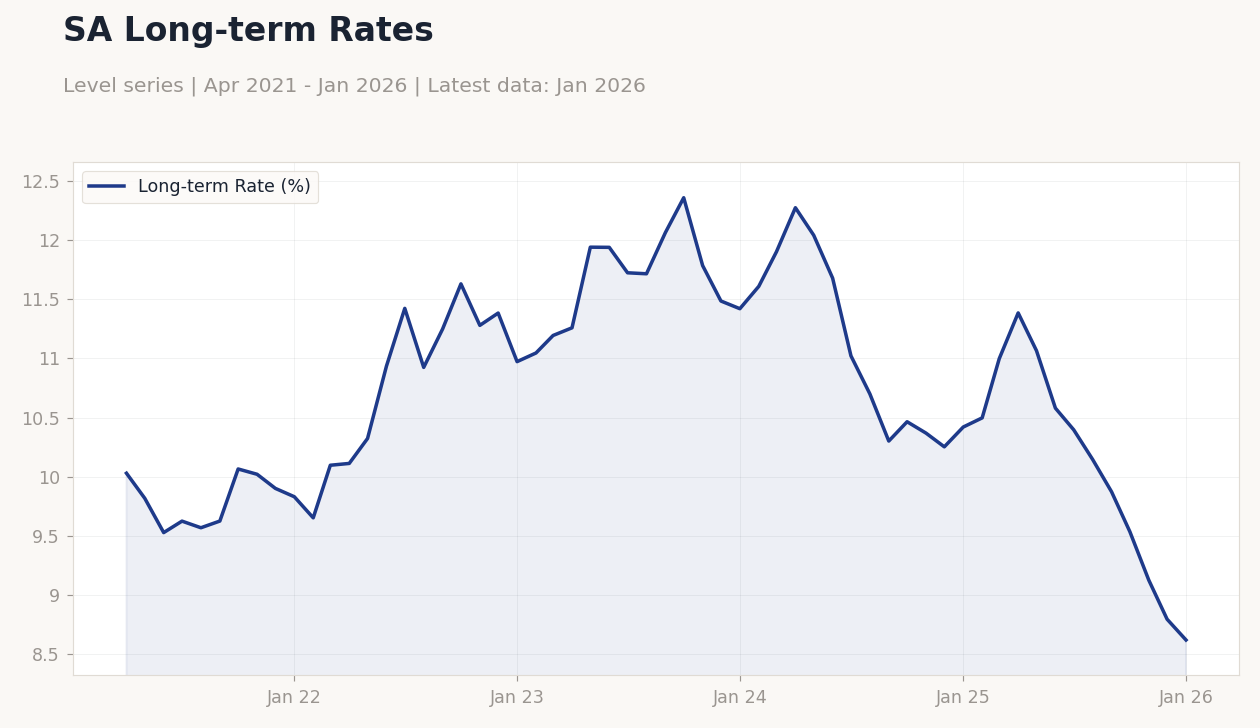

| South Africa Long-term Rate | 8.62% | -2.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-03-04) | |||

| GDP Growth Quarter-over-Quarter | 0.50 | - | 23:30 |

| GDP Growth Year-over-Year | 2.10 | - | 23:30 |

| Business Confidence Index | 44 | - | 00:00 |

- Geopolitical tensions in the Middle East drove Brent crude up 6.05% to $82.44, pressuring South African inflation and fueling a 2.67% rand depreciation to 16.50 against the USD.

- The JSE Top 40 plunged 5.85% to 111,842.41, hit by sharp declines in platinum (-8.86% to $2,107.00) and gold (-3.01% to $5,135.10) amid global risk aversion.

- South African long-term rates fell 2.00% to 8.62%, reflecting market bets on SARB caution amid rising oil-driven inflation risks.

Yesterday's Recap

South African markets endured heavy losses on March 2, with the JSE Top 40 index tumbling 5.85% to 111,842.41 as global geopolitical tensions escalated. The rand weakened sharply, with USD/ZAR rising 2.67% to 16.50, driven by surging Brent crude prices up 6.05% to $82.44 amid Middle East conflicts. Platinum prices cratered 8.86% to $2,107.00, exacerbating pain for the mining sector, while gold dropped 3.01% to $5,135.10 on reduced safe-haven demand.

EUR/ZAR edged down 0.54% to 18.78, offering slight relief, but Naspers shares fell 2.27% to 86,521.00, mirroring tech sector weakness. No major economic data releases occurred, leaving markets to react to external shocks, including higher fuel costs that threaten to amplify inflation pressures. South Africa short-term rates held steady at 6.75%, while long-term rates declined 2.00% to 8.62%, signaling investor flight to safety.

Bitcoin dipped 0.69% to $68,300.28, adding to the risk-off tone.

The Day Ahead

Investors eye South Africa's GDP growth figures releasing at 23:30 ET, with prior quarter-over-quarter at 0.5% and year-over-year at 2.1%, potentially signaling ongoing economic resilience amid energy challenges. The Business Confidence Index follows at 00:00 ET on March 4, previous reading at 44, which could reflect sentiment on load shedding and geopolitical impacts. No other major events are scheduled, allowing focus on these medium-impact indicators for clues on growth momentum.

Markets may trade cautiously ahead of these prints, with rand volatility likely if GDP surprises downward. Broader attention remains on global oil dynamics influencing SARB's inflation outlook.

Other Economic Notes

Escalating Middle East tensions are pushing up fuel prices, directly impacting South African consumers and potentially stoking inflation beyond the SARB's 3-6% target range. This comes amid persistent load shedding issues, which continue to hamper manufacturing and mining output, constraining overall GDP growth. Broader themes include the rand's vulnerability to commodity swings, with platinum and gold sectors facing headwinds from global demand slowdowns.