South Africa Macro Daily(Beta Mode)

Trade Surplus Jumps, Rand Rallies

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 108,807.40 | +2.37% |

| USD/ZAR | 16.87 | -1.89% |

| EUR/ZAR | 19.58 | +0.35% |

| Platinum | 1,969.30 | +0.99% |

| Gold | 4,783.20 | +2.92% |

| Brent Crude | 101.16 | -14.52% |

| Naspers | 86,196.00 | +1.03% |

| Bitcoin | 66,576.34 | -2.43% |

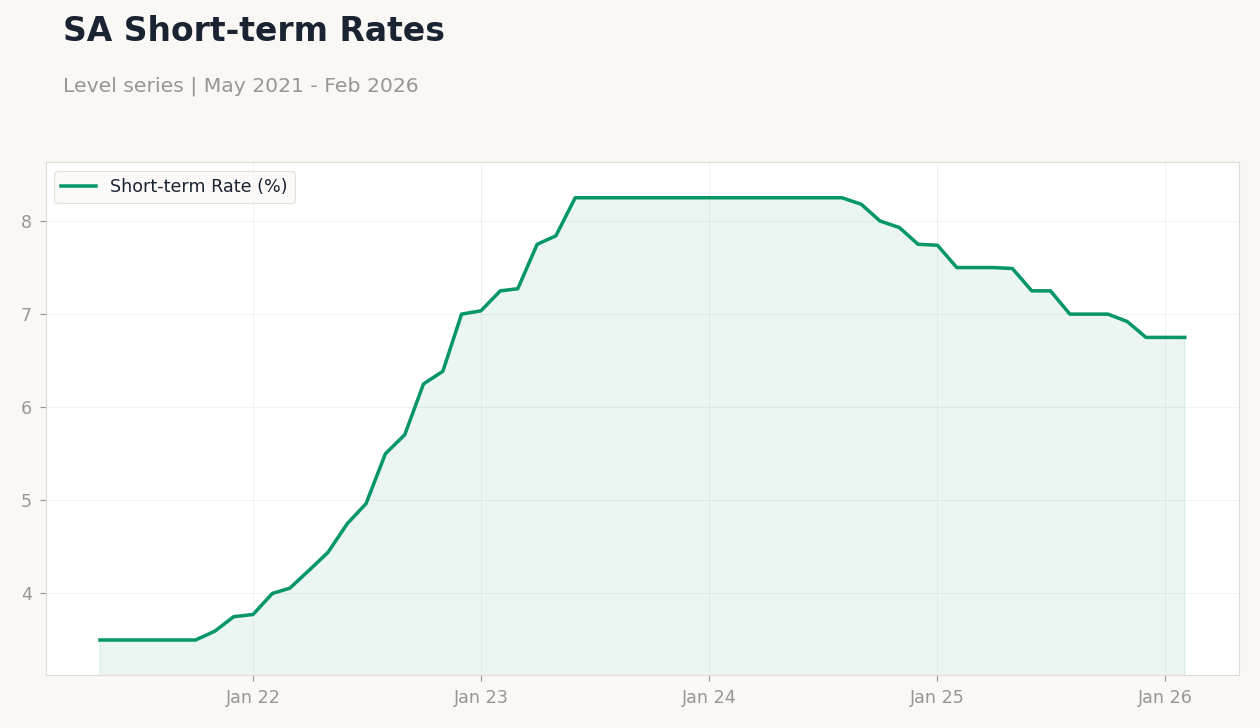

| South Africa Short-term Rate | 6.75% | +0.00% |

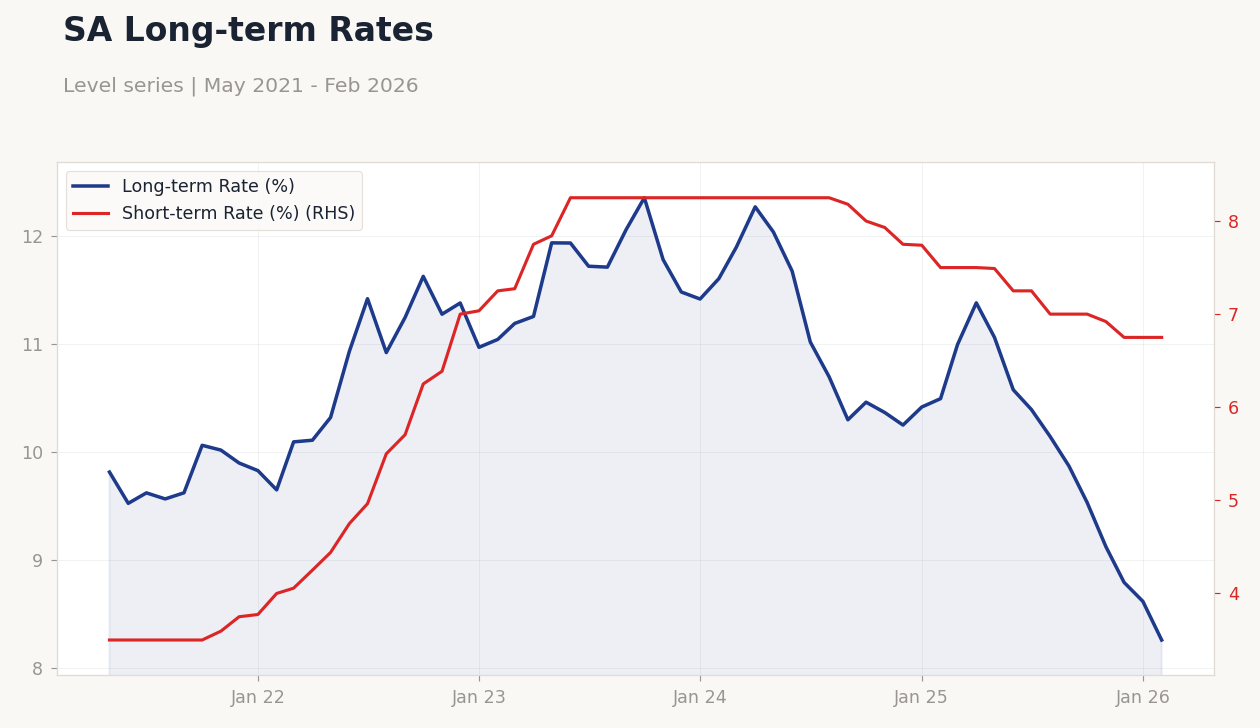

| South Africa Long-term Rate | 8.26% | -4.16% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Trade Balance | 8,500m | - | 36,920m |

SA Long-term Rates | Type: macro_line | Long-term Rate (%): 8.26 (2026-02-01) | Range: 8.26–12.36 | Trend(6pt): 9.817,11.42,12.06,10.37,8.618,8.26 | Short-term Rate (%): 6.75 (2026-02-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,4.964,8.25,7.93,6.75

SA Long-term Rates | Type: macro_line | Long-term Rate (%): 8.26 (2026-02-01) | Range: 8.26–12.36 | Trend(6pt): 9.817,11.42,12.06,10.37,8.618,8.26 | Short-term Rate (%): 6.75 (2026-02-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,4.964,8.25,7.93,6.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- South Africa's trade balance surged to ZAR 36.92 billion in March, far exceeding the previous ZAR 8.5 billion, boosting rand sentiment amid resilient exports.

- JSE Top 40 climbed 2.37% to 108,807.40, driven by gains in mining stocks as gold rose 2.92% to 4,783.20 and platinum 0.99% to 1,969.30, offsetting Brent crude's 14.52% plunge to 101.16.

- USD/ZAR fell 1.89% to 16.87, reflecting improved trade dynamics and global risk appetite, while long-term rates dropped 4.16% to 8.26%.

Yesterday's Recap

South Africa's trade balance for March printed at ZAR 36.92 billion, significantly outperforming the prior ZAR 8.5 billion and signaling robust export performance despite global headwinds. This positive data release supported a rand rally, with USD/ZAR declining 1.89% to 16.87 and EUR/ZAR edging up 0.35% to 19.58. Equity markets responded favorably, as the JSE Top 40 advanced 2.37% to 108,807.40, buoyed by resource-heavy gains including Naspers up 1.03% to 86,196.00.

Commodity prices aided the uplift, with gold surging 2.92% to 4,783.20 and platinum rising 0.99% to 1,969.30, though Brent crude tumbled 14.52% to 101.16 amid supply concerns. Bond yields softened, with the long-term rate falling 4.16% to 8.26%, while the short-term rate held steady at 6.75%. Bitcoin dipped 2.43% to 66,576.34, contrasting the broader risk-on tone in local assets.

The Day Ahead

The South African economic calendar remains light today with no major data releases scheduled, allowing markets to digest yesterday's strong trade surplus figures. Attention may shift to ongoing domestic developments, such as the army's deployment in crime hotspots, which could influence investor perceptions of stability. Tomorrow also features no key events, potentially keeping focus on global cues like oil price volatility.

Traders should monitor any unscheduled SARB commentary on resilience amid Middle East tensions. Overall, the quiet slate underscores a pause before potential upcoming indicators, with rand dynamics likely tied to commodity moves.

Other Economic Notes

South Africa's economy faces critical crossroads, with scenarios ranging from 3% growth under optimistic reforms to a lost decade of stagnation, as highlighted in recent analyses linking outcomes to policy choices like infrastructure investment. Fuel prices have surged despite a ZAR 3 per liter tax relief, pressuring household budgets and inflation expectations in an energy-vulnerable market. The deployment of 2,200 soldiers to combat gang violence in Cape Town and other provinces aims to restore order, potentially stabilizing business confidence in affected regions.