South Africa Macro Daily(Beta Mode)

Rand Strengthens, Bonds Rally

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 108,331.50 | -0.44% |

| USD/ZAR | 16.48 | -2.24% |

| EUR/ZAR | 19.23 | -1.16% |

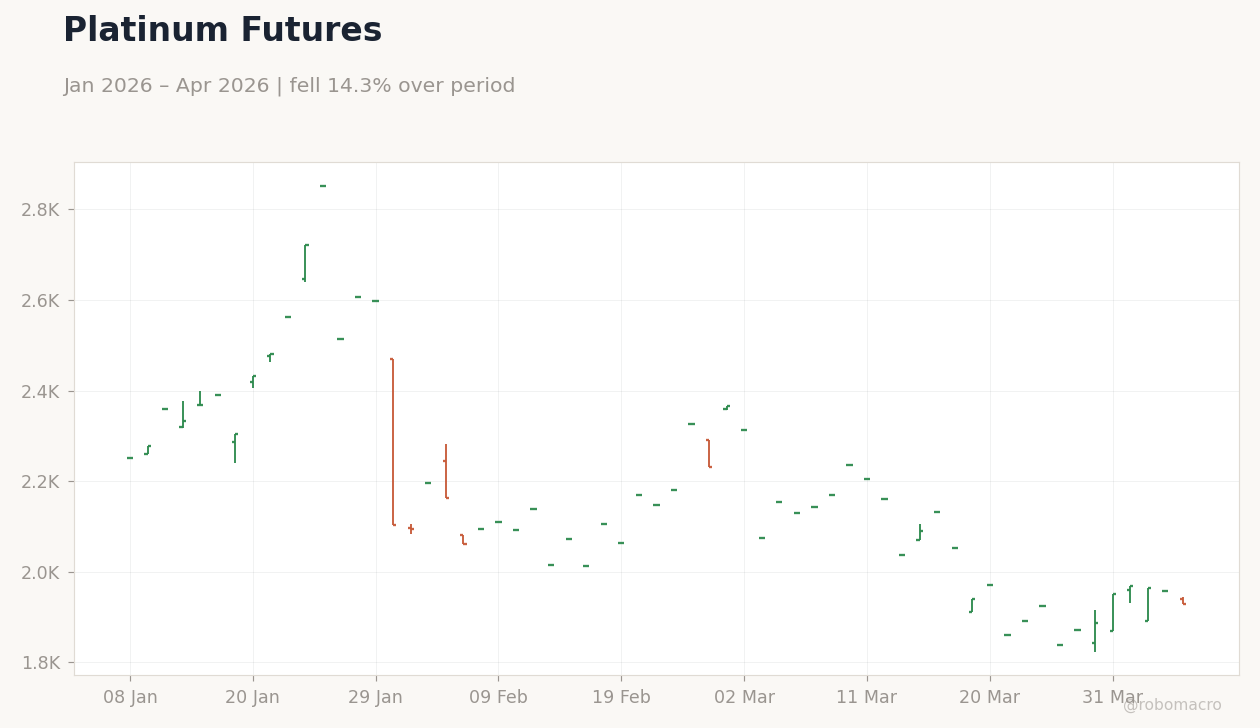

| Platinum | 1,929.10 | -1.49% |

| Gold | 4,657.10 | +0.01% |

| Brent Crude | 109.27 | -0.46% |

| Naspers | 86,196.00 | +1.03% |

| Bitcoin | 71,297.52 | +3.54% |

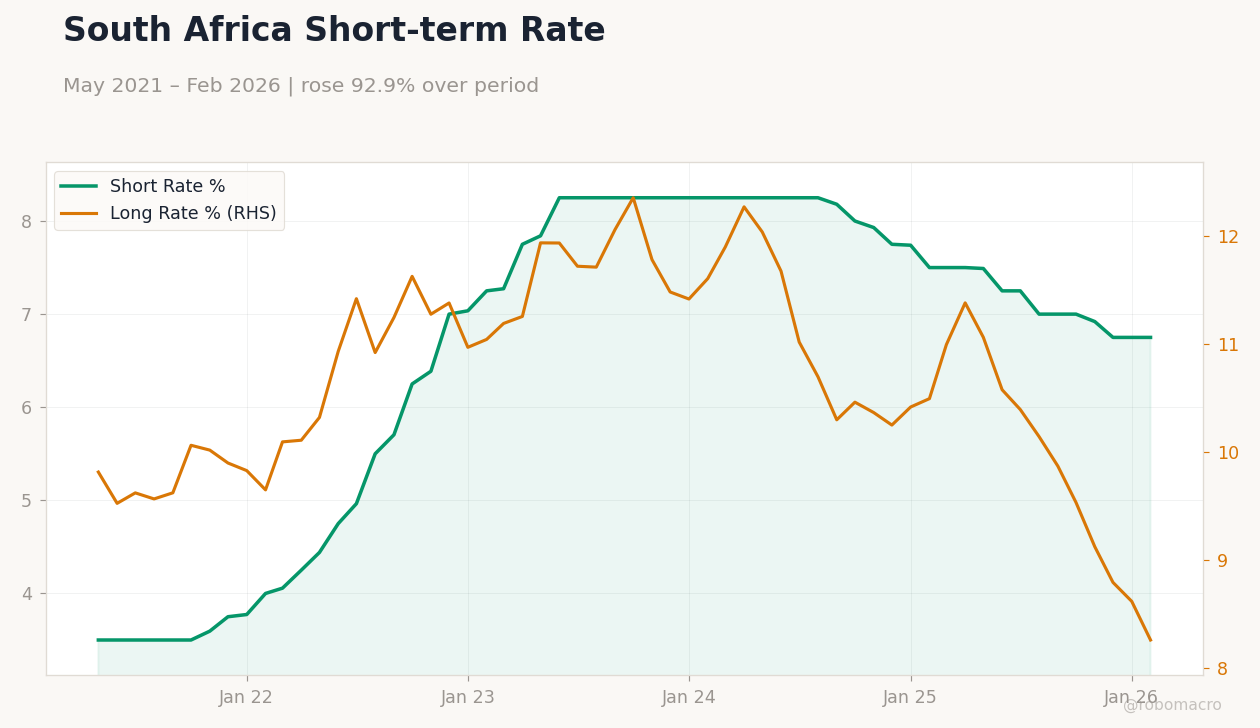

| South Africa Short-term Rate | 6.75% | +0.00% |

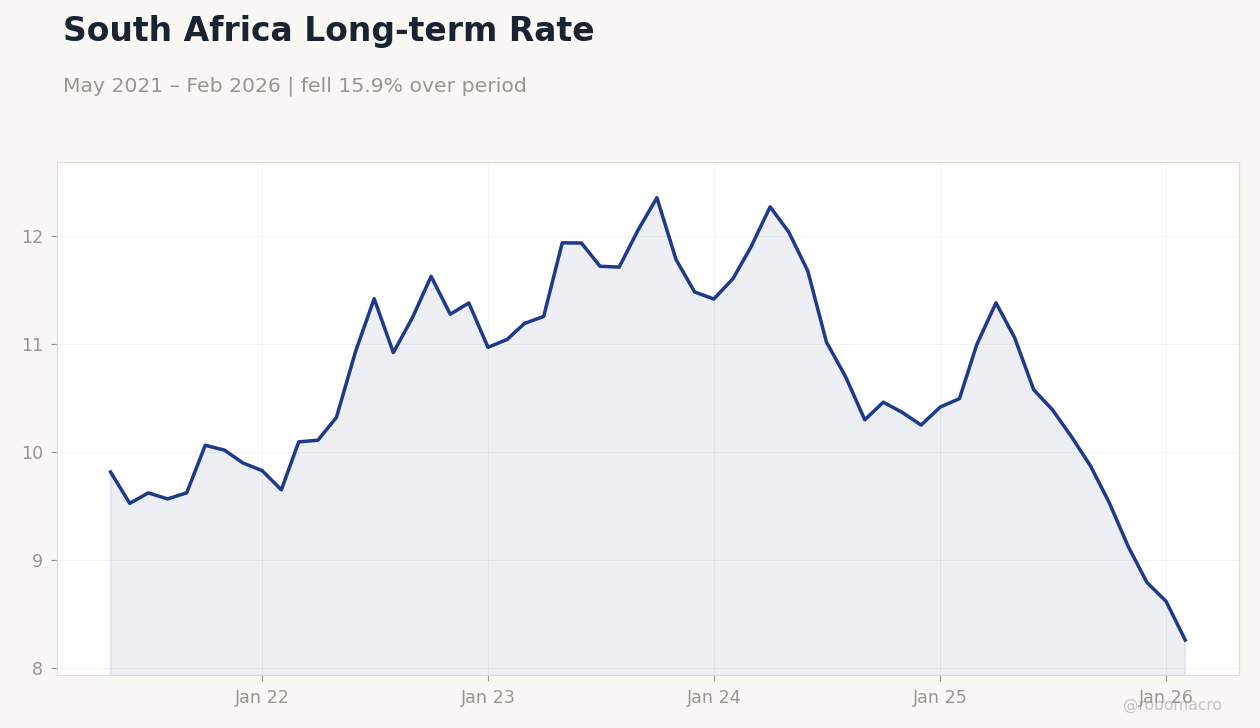

| South Africa Long-term Rate | 8.26% | -4.16% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

South Africa Long-term Rate | Type: macro_line | Long Rate %: 8.26 (2026-02-01) | Range: 8.26–12.36 | Trend(6pt): 9.817,11.42,12.06,10.37,8.618,8.26

South Africa Long-term Rate | Type: macro_line | Long Rate %: 8.26 (2026-02-01) | Range: 8.26–12.36 | Trend(6pt): 9.817,11.42,12.06,10.37,8.618,8.26

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- USD/ZAR fell 2.24% to 16.48, signaling rand strength amid mixed global cues.

- South Africa long-term rate dropped 4.16% to 8.26%, reflecting bond market rally.

- JSE Top 40 dipped 0.44% to 108,331.50, pressured by platinum's 1.49% decline.

Yesterday's Recap

South African markets showed mixed performance with no major data releases reported. The JSE Top 40 index closed down 0.44% at 108,331.50, weighed by weakness in mining stocks as platinum prices fell 1.49% to 1,929.10. In contrast, the rand strengthened notably, with USD/ZAR dropping 2.24% to 16.48 and EUR/ZAR declining 1.16% to 19.23, possibly driven by global risk sentiment shifts.

Gold held steady with a marginal 0.01% gain to 4,657.10, while Brent crude slipped 0.46% to 109.27, impacting energy-linked equities. Naspers shares rose 1.03% to 86,196.00, bucking the broader index trend on tech sector optimism. Bond markets rallied, with the long-term rate falling 4.16% to 8.26%, amid expectations of stable monetary policy.

The short-term rate remained unchanged at 6.75%, aligning with recent SARB guidance. Bitcoin climbed 3.54% to 71,297.52, reflecting broader crypto gains.

The Day Ahead

The calendar remains light with no scheduled economic releases or events for South Africa. Markets may focus on ongoing global developments, such as Iran's missile launches toward Israel, which could influence commodity prices and rand volatility. Attention turns to potential fuel price adjustments, as news highlights possible hikes in May that might pressure consumer spending.

Broader sentiment could be shaped by African tech advancements, like Morocco's 5G deployments at GITEX Africa, indirectly boosting regional investment flows. Investors should monitor JSE mining counters for any spillover from platinum and gold price movements. No SARB communications are expected, keeping rate expectations anchored.

Other Economic Notes

South Africa's agricultural sector eyes growth through pistachio exports from the Northern Cape, potentially diversifying revenue beyond traditional crops amid climate challenges. Fiscal pressures mount as high fuel prices and SARB rates strain consumers, risking slower retail and manufacturing activity. Energy stability persists without load shedding, supporting mining output in platinum and gold, though global demand fluctuations pose risks.

(cont...)