South Africa Macro Daily(Beta Mode)

Rand Weakens, Yields Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

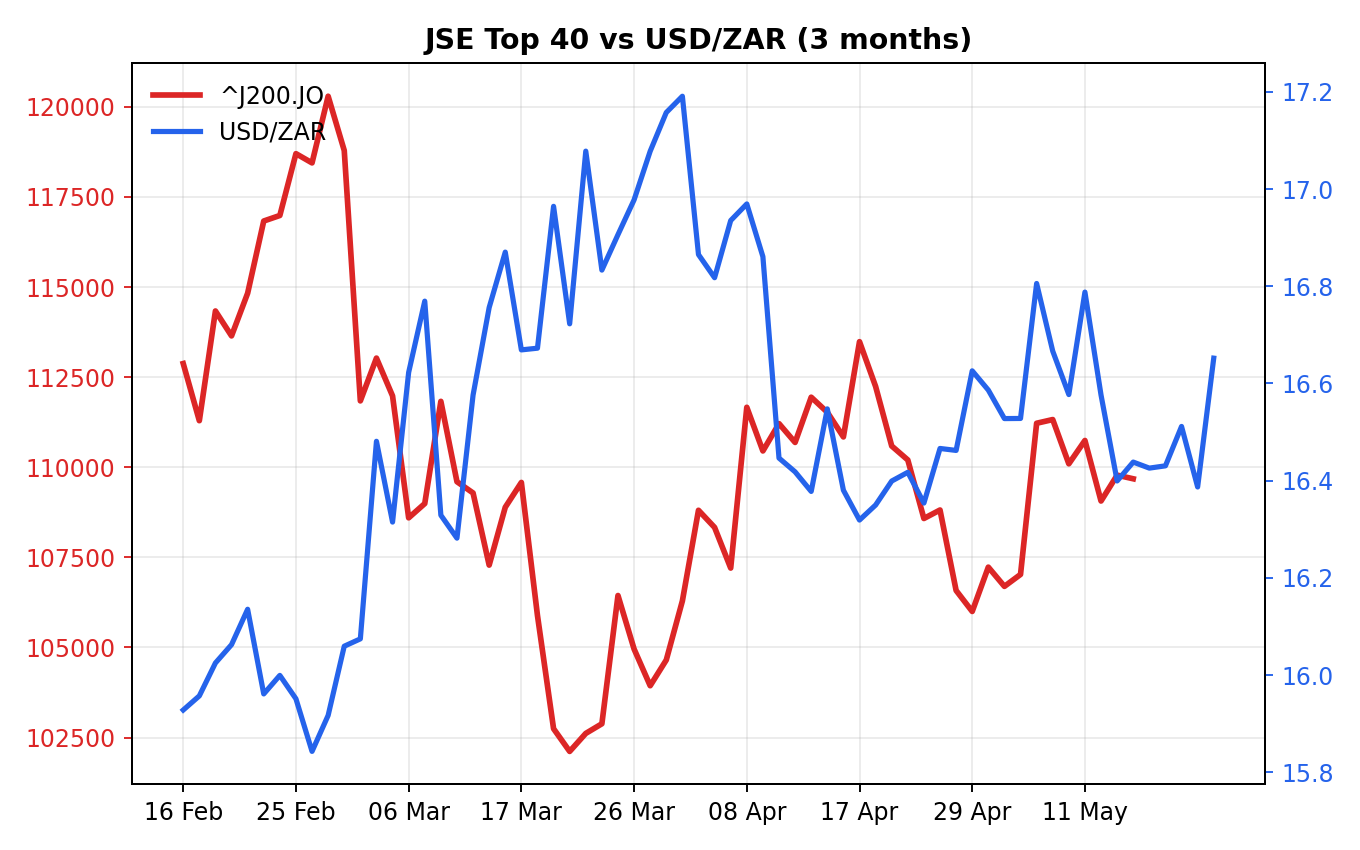

| JSE Top 40 | 109,680.90 | -0.09% |

| USD/ZAR | 16.62 | +1.41% |

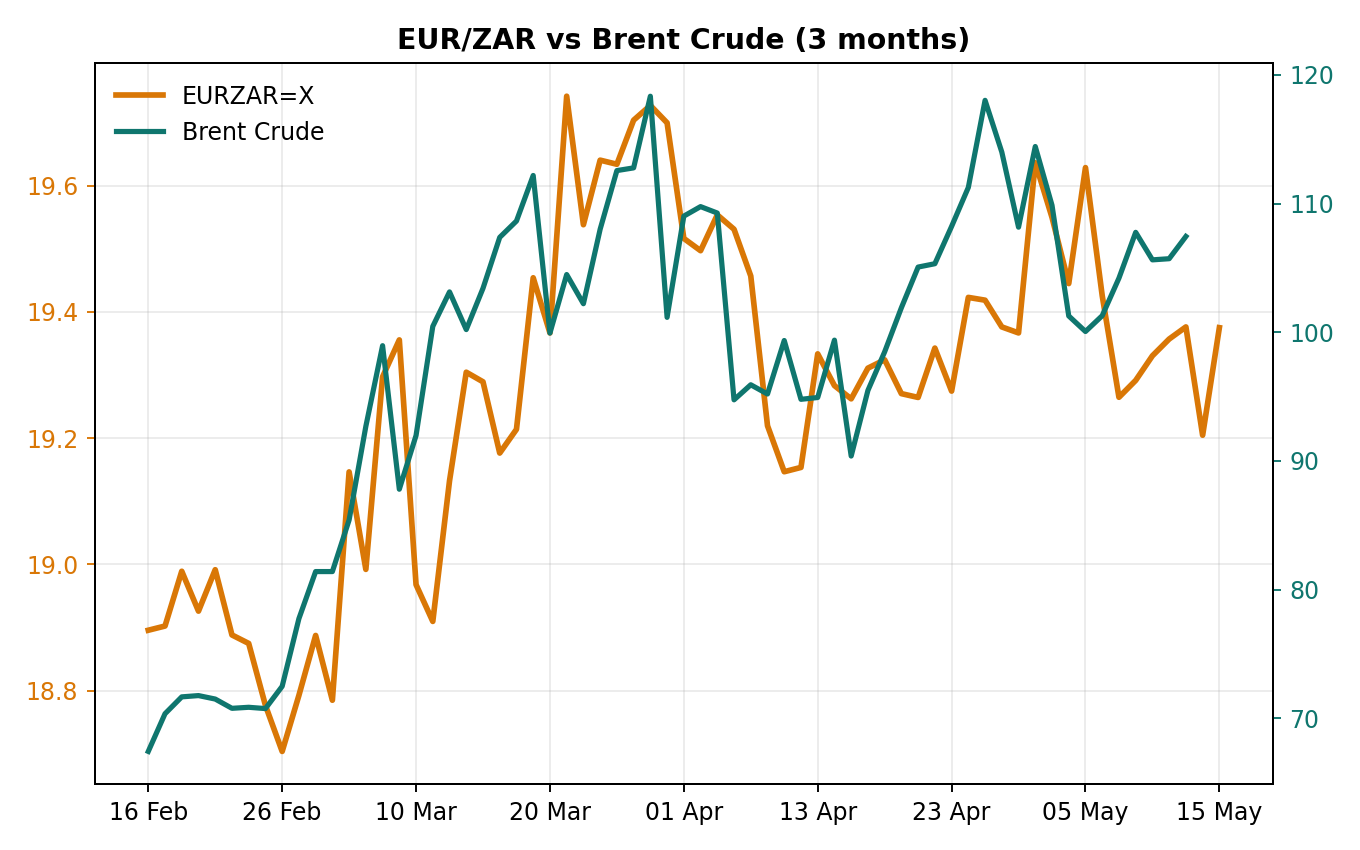

| EUR/ZAR | 19.36 | +0.78% |

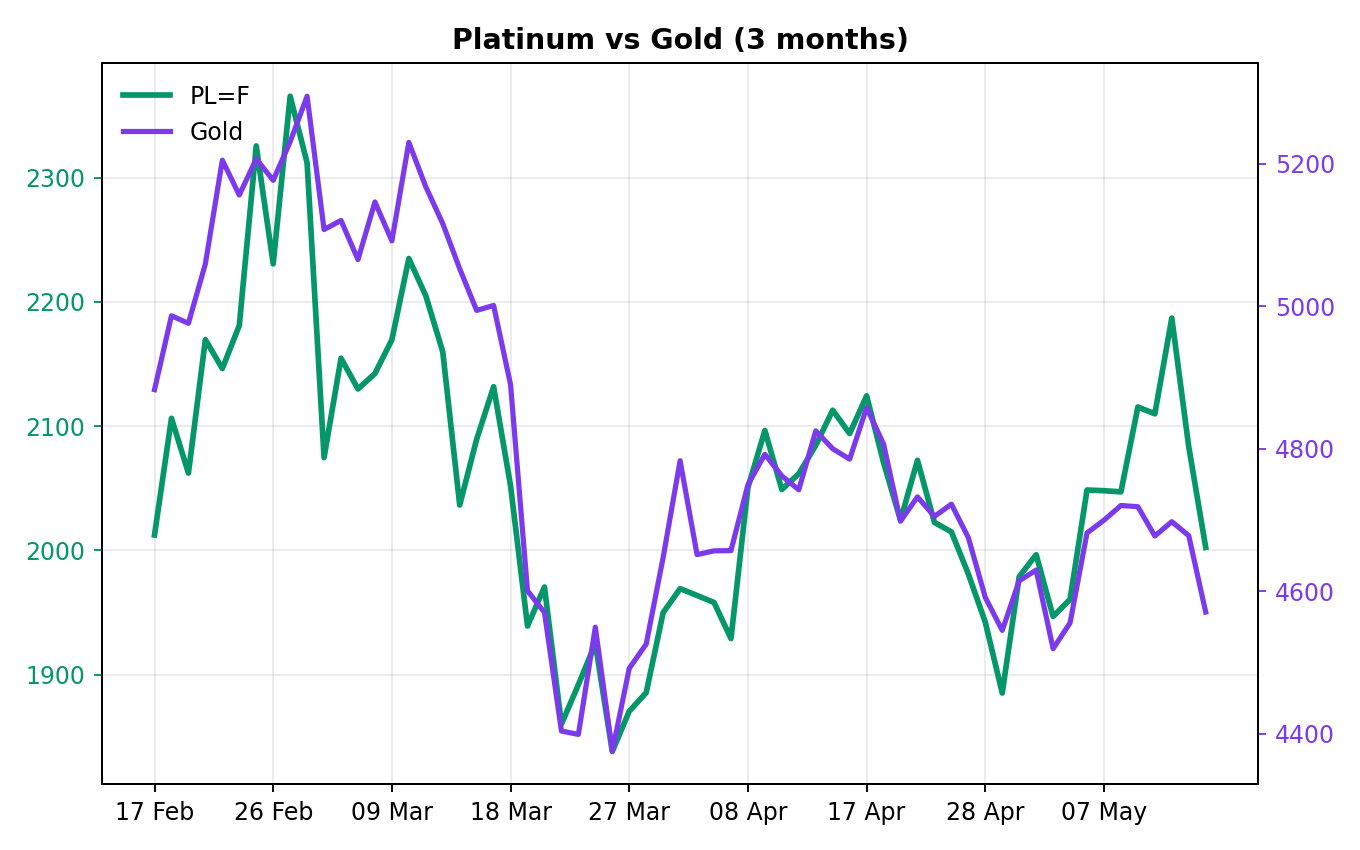

| Platinum | 2,010.90 | -3.48% |

| Gold | 4,585.80 | -1.97% |

| Brent Crude | 107.10 | +1.31% |

| Naspers | 87,895.00 | +3.67% |

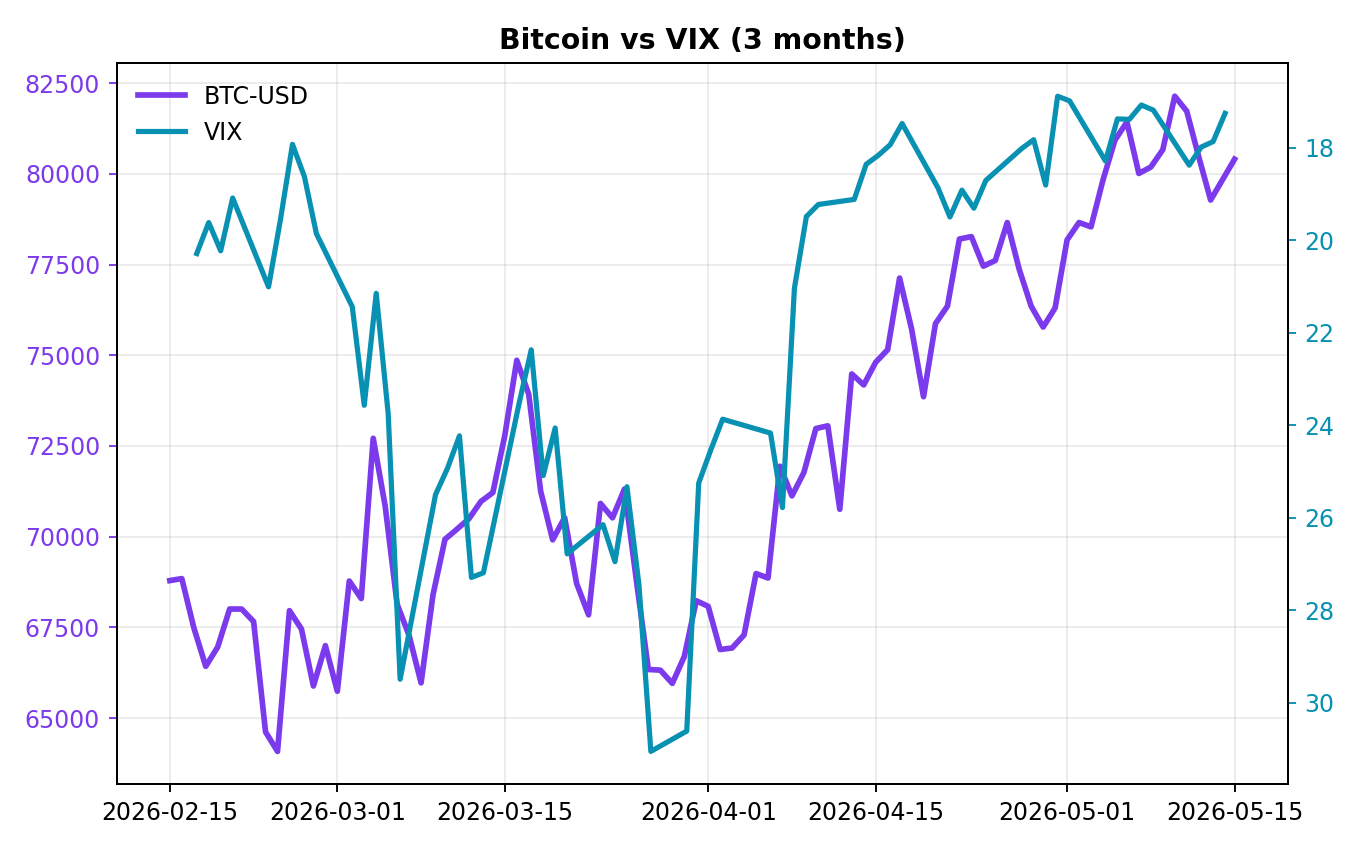

| Bitcoin | 80,350.51 | +1.35% |

| South Africa Short-term Rate | 6.75% | +0.00% |

| South Africa Long-term Rate | 9.05% | +9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

JSE vs USD/ZAR | Type: market_hloc | JSE Top 40: 1.097e+05 (2026-05-14) | Range: 1.021e+05–1.203e+05 | Trend(5pt): 1.129e+05,1.09e+05,1.047e+05,1.102e+05,1.097e+05 | USD/ZAR: 16.65 (2026-05-15) | Range: 15.84–17.19 | Trend(5pt): 15.93,16.33,16.87,16.46,16.65

JSE vs USD/ZAR | Type: market_hloc | JSE Top 40: 1.097e+05 (2026-05-14) | Range: 1.021e+05–1.203e+05 | Trend(5pt): 1.129e+05,1.09e+05,1.047e+05,1.102e+05,1.097e+05 | USD/ZAR: 16.65 (2026-05-15) | Range: 15.84–17.19 | Trend(5pt): 15.93,16.33,16.87,16.46,16.65

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-05-20) | |||

| Inflation Rate Month-over-Month | 0.60 | - | 04:00 |

| Inflation Rate Year-over-Year | 3.10 | - | 04:00 |

- USD/ZAR jumps 1.41% to 16.62 amid global USD strength; JSE Top 40 dips 0.09% to 109,680.90

- SA long-term rates spike 9.60% to 9.05%; platinum slumps 3.48% to 2,010.90

- Quiet data calendar; inflation due May 20; Transnet opens rail to private operators

Yesterday's Recap

South African markets closed mixed with no major data releases. The JSE Top 40 edged down 0.09% to 109,680.90, weighed by resource stocks as platinum plunged 3.48% to 2,010.90 and gold fell 1.97% to 4,585.80. Naspers bucked the trend, gaining 3.67% to 87,895.00 on tech momentum.

The rand weakened sharply, with USD/ZAR rising 1.41% to 16.62 and EUR/ZAR up 0.78% to 19.36, reflecting USD rally and domestic yield pressures. SA short-term rates held steady at 6.75%, but long-term rates surged 9.60% to 9.05%, signaling fiscal concerns. Brent crude rose 1.31% to 107.10, offering some commodity support.

Bitcoin climbed 1.35% to 80,350.51.

The Day Ahead

The local calendar remains empty today and tomorrow, leaving focus on global cues. Inflation data looms next week on May 20, with MoM (prev. 0.6%) and YoY (prev.

3.1%) releases at 04:00, both medium impact and no consensus available. Prints will shape SARB cut bets amid steady 6.75% repo. No MPC speeches scheduled.

Transnet's private rail operator announcement may boost logistics sentiment. Markets eye Bank of Canada rate decision and Monetary Policy Report at 09:45 ET, plus Business Outlook Survey at 11:30 ET, for carry trade implications.

Other Economic Notes

Transnet granted 11 private firms access to freight rail, a step toward easing logistics bottlenecks that crimp mining exports. Deadly floods in Western and Northern Cape disrupt agriculture and infrastructure, adding to growth headwinds. Anti-immigrant protests prompt Ghana to evacuate 300 nationals, highlighting social tensions that could deter FDI.

SA top court ruling bars repeat asylum applications, aiding home affairs efficiency but risking regional diplomatic friction.

Global Macro News

Bank of Canada announces interest rate and Monetary Policy Report at 09:45 ET, with Business Outlook Survey at 11:30 ET; a dovish tilt could weaken CAD/ZAR carry. <i>↓ p.2</i>