South Africa Macro Daily(Beta Mode)

Rand Weakens as US Inflation Shifts Fed Outlook

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 106,842.10 | -2.59% |

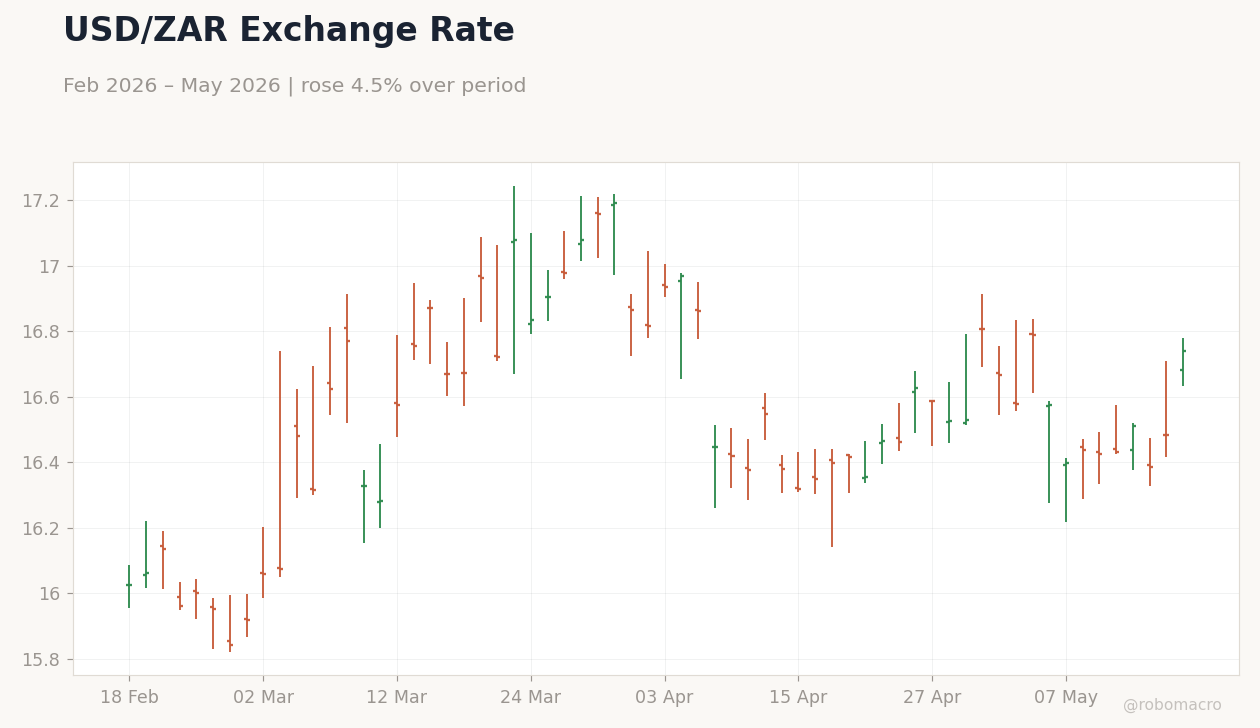

| USD/ZAR | 16.74 | +1.53% |

| EUR/ZAR | 19.45 | +1.20% |

| Platinum | 1,972.90 | -0.42% |

| Gold | 4,543.60 | -0.27% |

| Brent Crude | 111.20 | +1.78% |

| Naspers | 86,842.00 | +1.69% |

| Bitcoin | 77,014.50 | -1.43% |

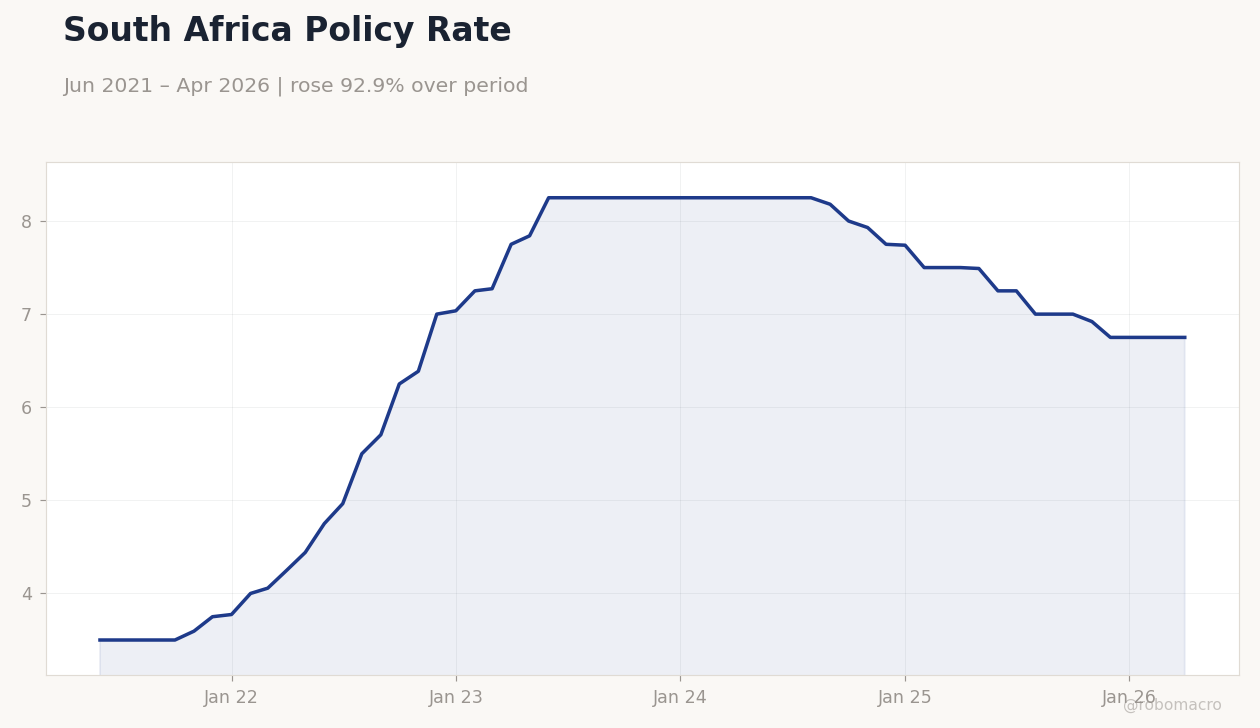

| South Africa Short-term Rate | 6.75% | +0.00% |

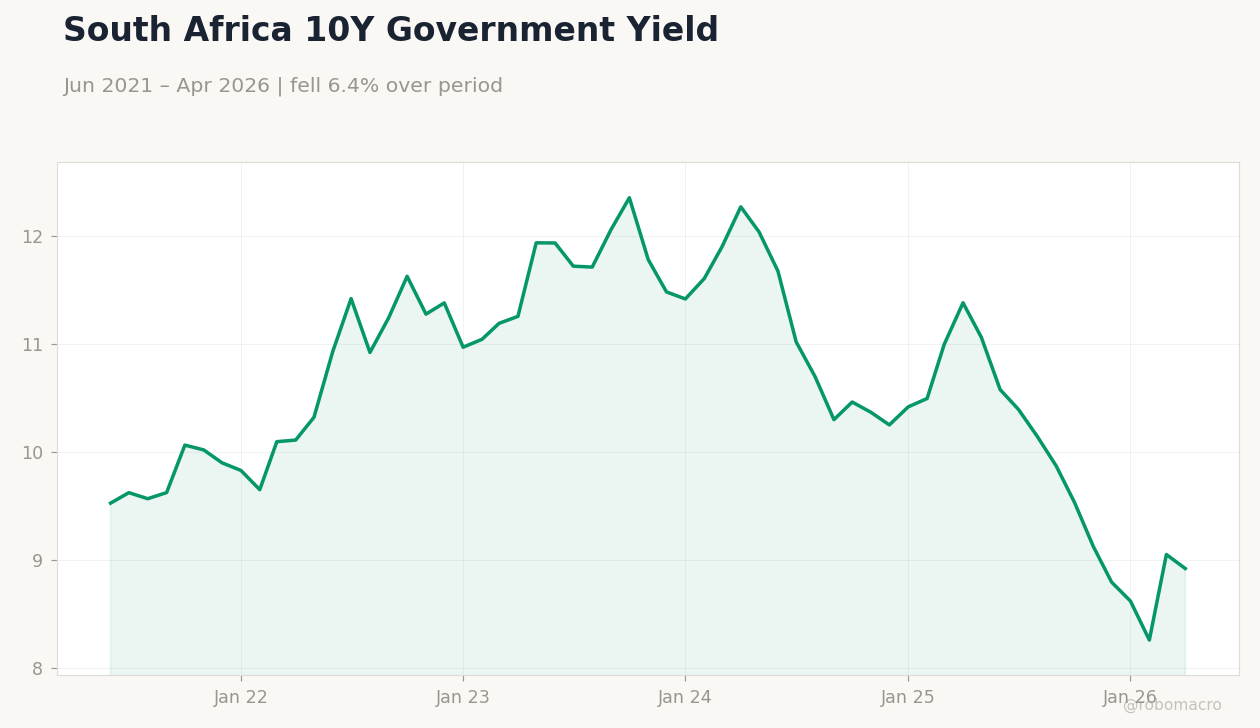

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

South Africa Policy Rate | Type: macro_line | Repo Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.5,8.25,7.75,6.75

South Africa Policy Rate | Type: macro_line | Repo Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.5,8.25,7.75,6.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-05-20) | |||

| Inflation Rate Month-over-Month | 0.60 | - | 04:00 |

| Inflation Rate Year-over-Year | 3.10 | - | 04:00 |

- USD/ZAR rises 1.53% to 16.74 as US inflation data shifts Fed expectations

- JSE Top 40 drops 2.59% to 106,842.10 while long-term yields ease 14 bp to 8.92%

- SARB holds repo rate at 6.75% ahead of May 20 inflation release

Yesterday's Recap

South African markets absorbed the fallout from hotter US inflation prints that prompted investors to reassess the Fed path. The rand weakened sharply, with USD/ZAR climbing to 16.74 and EUR/ZAR reaching 19.45. Equities sold off, sending the JSE Top 40 down 2.59% to 106,842.10 amid broad risk aversion.

Brent crude gained 1.78% to 111.20 while gold and platinum posted modest losses. The 10-year government bond yield declined 14 bp to 8.92%, reflecting some safe-haven demand for local duration. No domestic data releases occurred on 17 May, leaving the focus squarely on external drivers and rand volatility.

Short-term rates remained anchored at 6.75%.

The Day Ahead

Markets will monitor the 20 May release of South African inflation figures for both month-over-month and year-over-year readings. The prints follow the 3.1% y/y outcome and will shape expectations for the next SARB decision. Treasury bond auctions of R4.5 billion in the R2035 and R2040 lines are also scheduled.

Traders will watch for any comments from SARB officials on data dependence. Mining output data due later this week could highlight weather or energy-related disruptions. Positioning ahead of these releases is likely to keep the rand sensitive to global risk sentiment.

Other Economic Notes

Persistent energy constraints continue to weigh on industrial output and mining sector confidence. Uranium exploration plans in the Kalahari region have drawn scrutiny over potential aquifer risks, adding to long-term environmental policy uncertainty. Fiscal issuance remains steady, with the Treasury maintaining its weekly auction schedule despite softer growth signals.

The combination of contained inflation and external shocks leaves little room for near-term policy easing. Markets continue to price only modest cuts later in the year.

Global Macro News

Stronger US inflation readings triggered a reassessment of the Federal Reserve’s easing timeline, boosting the dollar and pressuring emerging-market currencies. <i>↓ p.2</i>