South Africa Macro Daily(Beta Mode)

Rand Firms Ahead of Inflation Release

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 107,145.40 | +0.28% |

| USD/ZAR | 16.65 | -0.39% |

| EUR/ZAR | 19.36 | -0.31% |

| Platinum | 1,973.60 | +0.28% |

| Gold | 4,543.80 | -0.19% |

| Brent Crude | 109.98 | -1.89% |

| Naspers | 86,842.00 | +1.69% |

| Bitcoin | 76,865.64 | -0.73% |

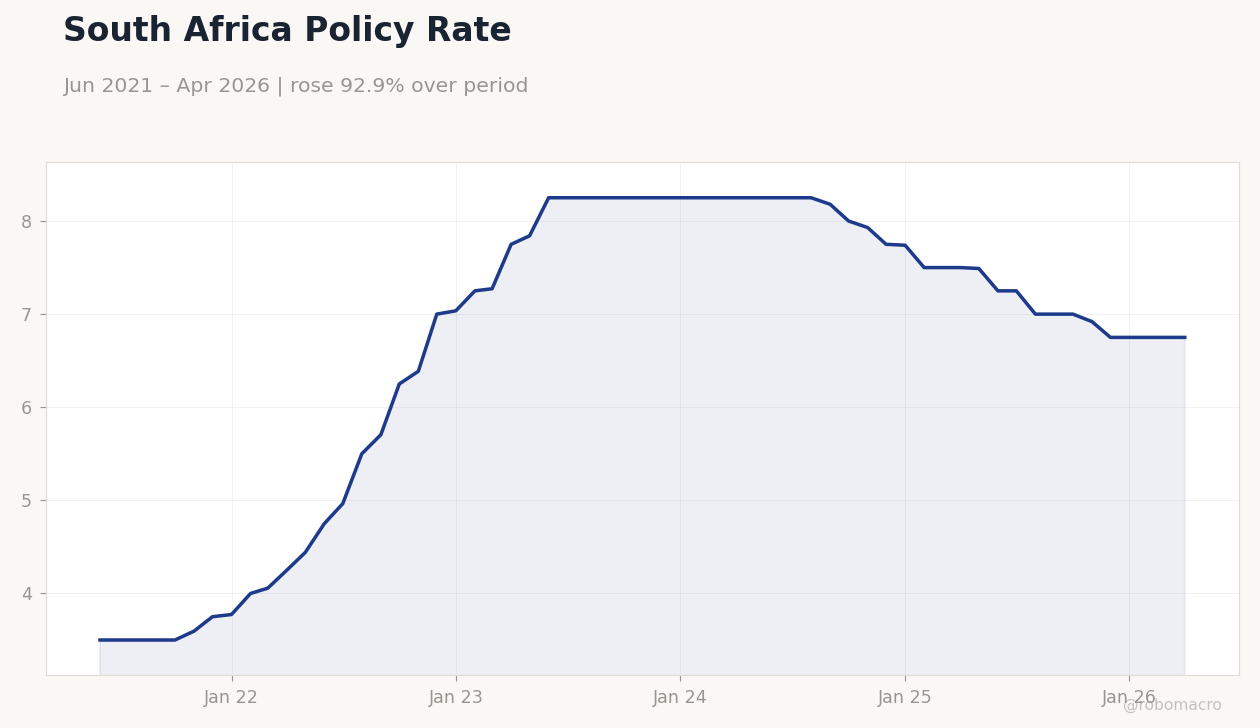

| South Africa Short-term Rate | 6.75% | +0.00% |

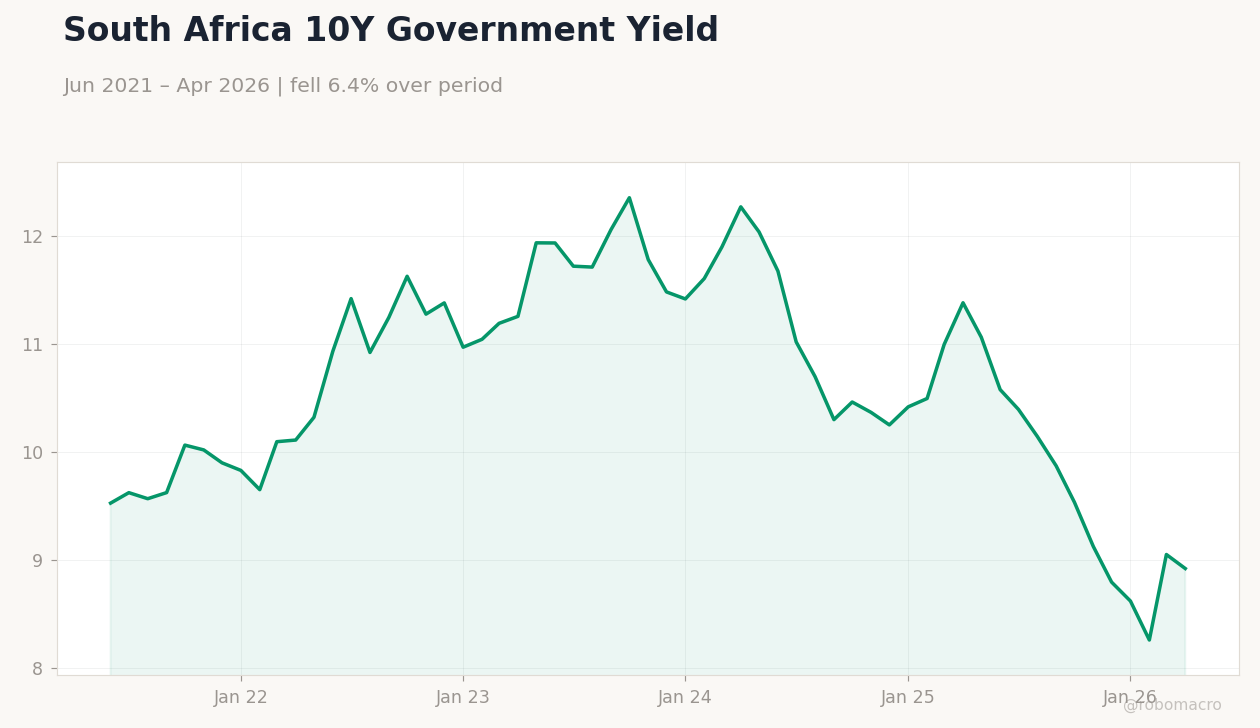

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

South Africa Policy Rate | Type: macro_line | Short-term Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.5,8.25,7.75,6.75

South Africa Policy Rate | Type: macro_line | Short-term Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.5,8.25,7.75,6.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-05-20) | |||

| Inflation Rate Month-over-Month | 0.60 | - | 00:00 |

| Inflation Rate Year-over-Year | 3.10 | - | 00:00 |

- USD/ZAR fell 0.39% to 16.65 as commodity prices and local data supported the currency.

- JSE Top 40 rose 0.28% to 107,145.40 while the long-term yield dropped 1.44% to 8.92%.

- Markets await May 20 inflation prints that will shape SARB policy expectations.

Yesterday's Recap

South African markets closed higher on May 18 with the JSE Top 40 advancing 0.28% to 107,145.40 amid firmer platinum and rand strength. USD/ZAR declined 0.39% to 16.65 while EUR/ZAR eased 0.31% to 19.36. The long-term government bond yield fell sharply 1.44% to 8.92%, reflecting improved risk sentiment and lower global yields.

Platinum gained 0.28% to 1,973.60 on autocatalyst demand while gold slipped 0.19% to 4,543.80. Brent crude dropped 1.89% to 109.98. No major data releases occurred yesterday, leaving market moves driven by external flows and commodity price action.

The short-term rate held steady at 6.75%.

The Day Ahead

South Africa will release April inflation figures on May 20, covering both month-over-month and year-over-year rates. The prior MoM reading stood at 0.6% and YoY at 3.1%, with consensus currently unavailable. These prints will feed directly into SARB inflation assessments ahead of the next MPC meeting.

No speeches or additional domestic indicators are scheduled for today. Traders will monitor any revisions to global growth forecasts that could influence rand flows.

Other Economic Notes

Eskom maintained stage-2 load-shedding over the weekend yet reported unplanned outages falling to 8,200 MW, supporting mining output. Anglo American Platinum plans to restart two furnaces at Mogalakwena, adding 150 koz of annual capacity. Finance Minister Godongwana reaffirmed the 3.3% of GDP fiscal-deficit target for FY26/27, easing bond-market concerns.

Retail sales rose 1.9% y/y in March, beating expectations and lifting Q2 GDP forecasts.

Global Macro News

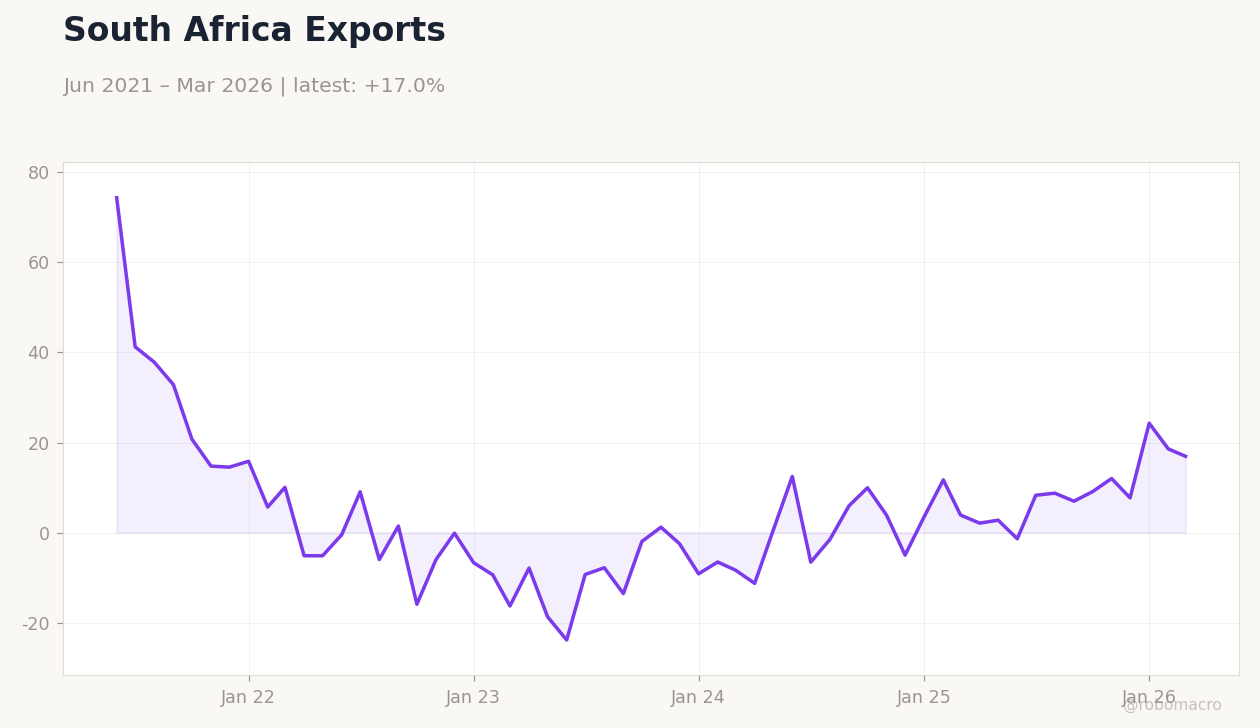

Stronger US inflation data prompted markets to reassess the timing of Fed easing, pushing USD/ZAR toward 17 in recent sessions. Brazil posted 1.3% GDP growth in Q1 despite a March slowdown, highlighting mixed EM momentum. Beijing’s zero-tariff policy for African exports gained attention as a potential boost for South African trade.

<i>↓ p.2</i>