South Africa Macro Daily(Beta Mode)

SARB Faces Rate-Hike Pressure as Inflation Looms

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 105,895.20 | -1.17% |

| USD/ZAR | 16.71 | +0.85% |

| EUR/ZAR | 19.39 | +0.38% |

| Platinum | 1,920.90 | -0.67% |

| Gold | 4,462.40 | -0.97% |

| Brent Crude | 110.72 | -0.50% |

| Naspers | 86,590.00 | -0.29% |

| Bitcoin | 76,743.48 | -0.27% |

| South Africa Short-term Rate | 6.75% | +0.00% |

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

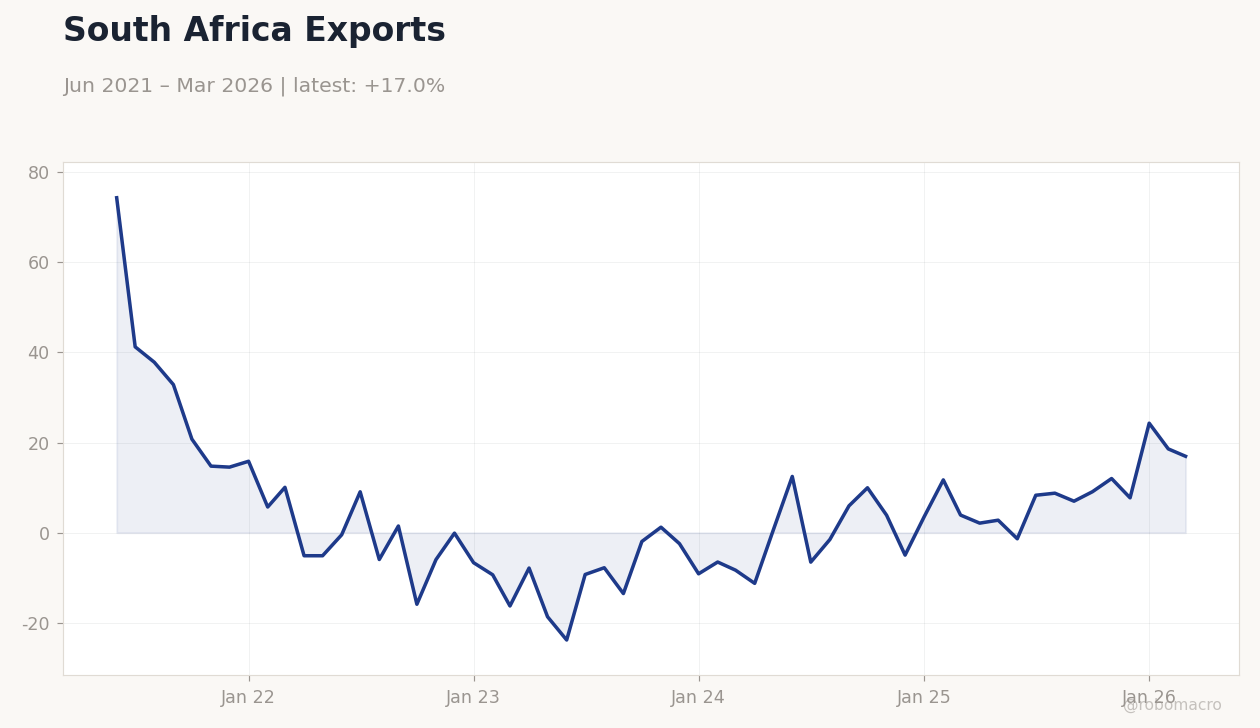

South Africa Exports | Type: macro_line | Exports YoY %: 16.95 (2026-03-01) | Range: -23.83–74.35 | Trend(6pt): 74.35,-5.956,-1.96,-4.98,18.59,16.95

South Africa Exports | Type: macro_line | Exports YoY %: 16.95 (2026-03-01) | Range: -23.83–74.35 | Trend(6pt): 74.35,-5.956,-1.96,-4.98,18.59,16.95

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Month-over-Month | 0.60 | - | 00:00 |

| Inflation Rate Year-over-Year | 3.10 | 3.90 | 00:00 |

- April inflation data due today with consensus 3.9% y/y, up from 3.1%, raising hike risks amid Iran war spillovers.

- JSE Top 40 fell 1.17% while USD/ZAR rose 0.85% to 16.71 as rand weakened on global risk-off flows.

- SARB repo rate holds at 6.75% with long-term yields dropping 1.44% to 8.92%, pricing policy caution.

Yesterday's Recap

South African markets closed lower as the JSE Top 40 dropped 1.17% to 105,895.20 amid weaker mining shares and global caution. USD/ZAR climbed 0.85% to 16.71 while EUR/ZAR gained 0.38% to 19.39, reflecting rand pressure from risk aversion. Platinum fell 0.67% to 1,920.90 and gold slipped 0.97% to 4,462.40 despite safe-haven bids.

Brent crude eased 0.50% to 110.72. The short-term rate stayed at 6.75% while the long-term rate declined 1.44% to 8.92%, flattening the curve slightly. No major data releases occurred yesterday, leaving focus on external drivers and positioning ahead of today's inflation prints.

Naspers declined 0.29% with Bitcoin off 0.27%.

The Day Ahead

Markets await the April inflation rate month-over-month and year-over-year releases scheduled for today. Consensus points to a rise to 3.9% y/y from the prior 3.1%, with war-related energy costs likely to feature in the breakdown. Analysts will assess whether the print reinforces or delays any SARB policy shift.

Mining production figures and the SARB Quarterly Bulletin also draw attention for growth signals. Rand volatility may increase on the data, particularly if upside surprises emerge in core components. Traders monitor JSE resources for any follow-through from commodity moves.

Other Economic Notes

Mining output remains a key swing factor for GDP and the current account given platinum and gold exposure. Energy supply constraints continue to weigh on industrial activity despite no fresh load-shedding escalations reported. Fiscal data showed a narrower April deficit than budgeted, easing near-term debt concerns.

Broader sentiment ties to commodity prices and external risk appetite, with the rand oscillating between gold-trade and risk-trade dynamics. Corporate positioning shows limited fresh flows into local assets.

Global Macro News

Iran's war drove gasoline prices higher, pushing Canada's inflation to 2.8% and highlighting similar pass-through risks for South Africa. Dollar steadiness and yen weakness after strong Japanese GDP kept external yields supported. <i>↓ p.2</i>