South Africa Macro Daily(Beta Mode)

Rand Rises on South African Inflation Surprise

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 106,948.70 | +0.99% |

| USD/ZAR | 16.48 | -1.32% |

| EUR/ZAR | 19.15 | -1.18% |

| Platinum | 1,941.80 | -0.41% |

| Gold | 4,537.70 | +0.14% |

| Brent Crude | 105.82 | +0.76% |

| Naspers | 88,565.00 | -1.46% |

| Bitcoin | 77,943.54 | +1.55% |

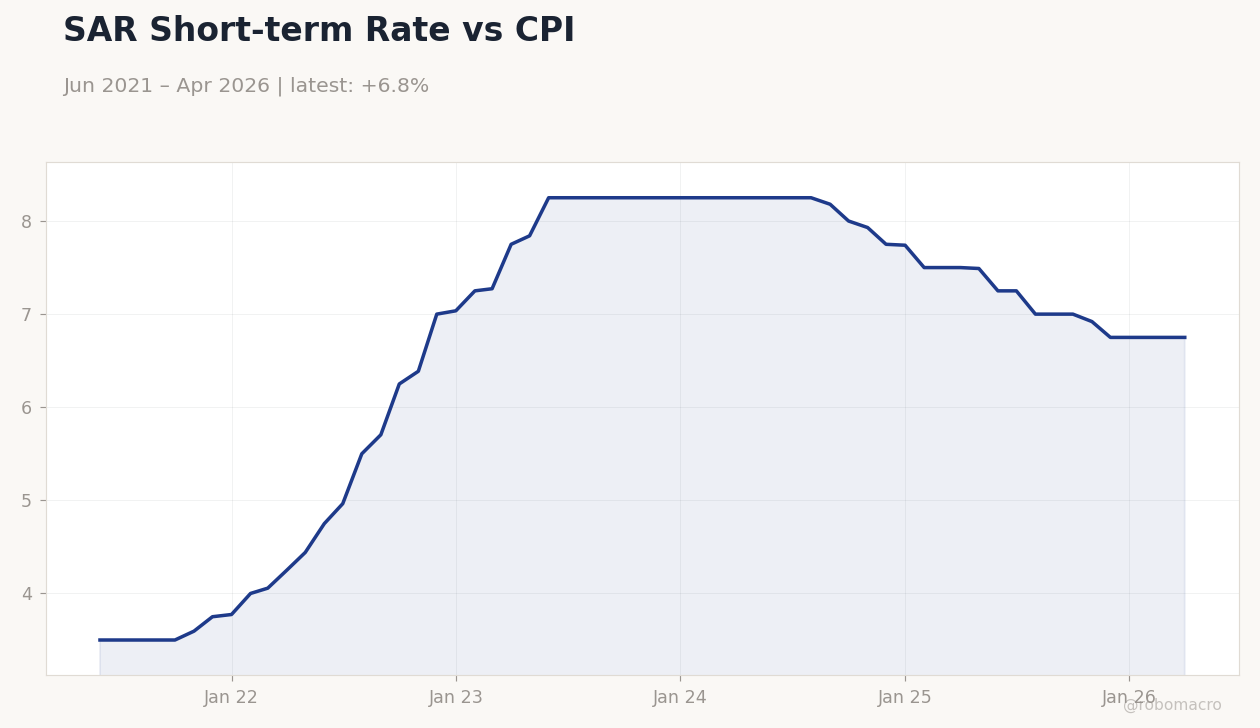

| South Africa Short-term Rate | 6.75% | +0.00% |

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Month-over-Month | 0.60 | - | 1.10 |

| Inflation Rate Year-over-Year | 3.10 | 3.90 | 4 |

SAR Short-term Rate vs CPI | Type: macro_line | Policy Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.5,8.25,7.75,6.75

SAR Short-term Rate vs CPI | Type: macro_line | Policy Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.5,8.25,7.75,6.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- South African April inflation rose to 4.0% y/y from 3.1%, beating consensus of 3.9%.

- Rand strengthened sharply with USD/ZAR falling 1.32% to 16.48 on rate-hike speculation.

- JSE Top 40 advanced 0.99% while long-term yields dropped 1.44% to 8.92%.

Yesterday's Recap

South Africa’s April inflation rate printed 4.0% year-over-year, up from 3.1% and above the 3.9% consensus forecast. Month-over-month prices jumped 1.1% versus 0.6% previously. The stronger-than-expected reading lifted expectations for possible SARB tightening and drove the rand 1.32% higher against the dollar to 16.48.

The JSE Top 40 index rose 0.99% to 106,948.70, led by mining and resource names. South Africa’s long-term government bond yield fell 1.44% to 8.92%. Gold gained 0.14% while platinum slipped 0.41% and Brent crude added 0.76% to 105.82.

The short-term policy rate remained steady at 6.75%.

The Day Ahead

No major South African data releases are scheduled for today or tomorrow. Markets will continue to assess the inflation surprise and its implications for the next MPC meeting. Traders will watch rand volatility and bond-curve moves for shifts in rate expectations.

Global commodity prices and any US data surprises will remain key external drivers. Focus stays on how the 4.0% inflation print alters the SARB’s near-term policy path.

Other Economic Notes

Higher inflation has revived speculation about earlier rate hikes despite the current 6.75% repo level. Export sectors stand to benefit from China’s zero-tariff policy on South African apples and pears. Fiscal consolidation efforts continue to anchor debt-to-GDP projections.

Stable power supply has reduced load-shedding risks and supported industrial output. Regional trade initiatives, including port-efficiency talks, could lift medium-term growth prospects.

Global Macro News

China’s zero-tariff measures are expanding demand for South African horticultural exports. The World Bank’s push to mobilize $23 billion in private capital for Africa may improve infrastructure funding access. Global maritime leaders are coordinating on port upgrades that could enhance regional trade flows.

<i>↓ p.2</i>