South Africa Macro Daily(Beta Mode)

SA GDP Surge Lifts Outlook as Rand Eases

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 106,285.40 | -0.62% |

| USD/ZAR | 16.44 | -0.10% |

| EUR/ZAR | 19.10 | -0.17% |

| Platinum | 1,970.10 | +0.77% |

| Gold | 4,529.00 | -0.24% |

| Brent Crude | 104.12 | +1.50% |

| Naspers | 86,415.00 | -2.58% |

| Bitcoin | 77,579.98 | +0.16% |

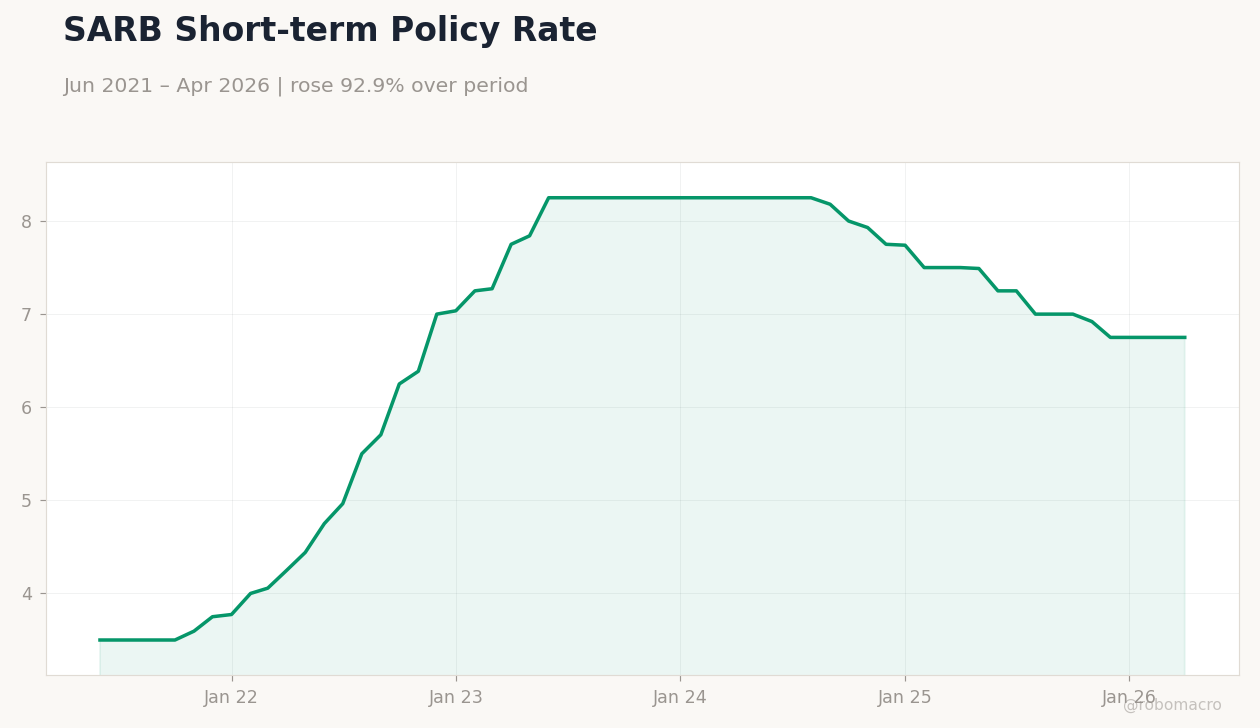

| South Africa Short-term Rate | 6.75% | +0.00% |

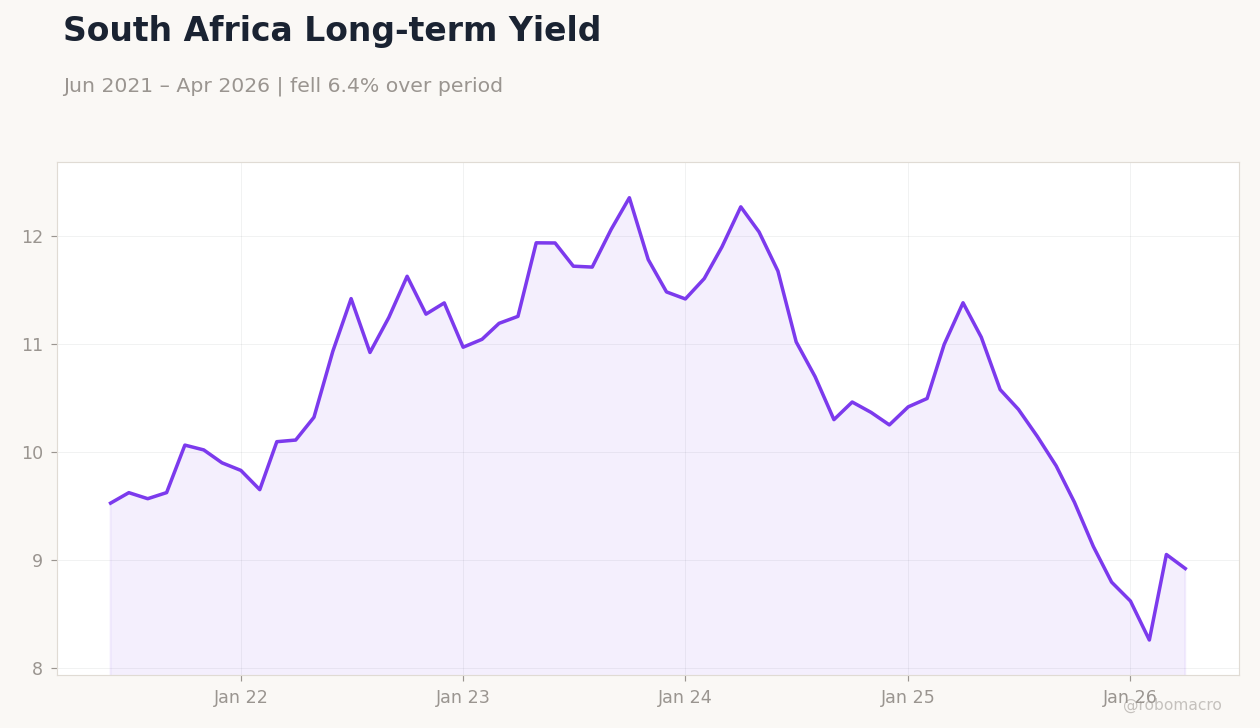

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

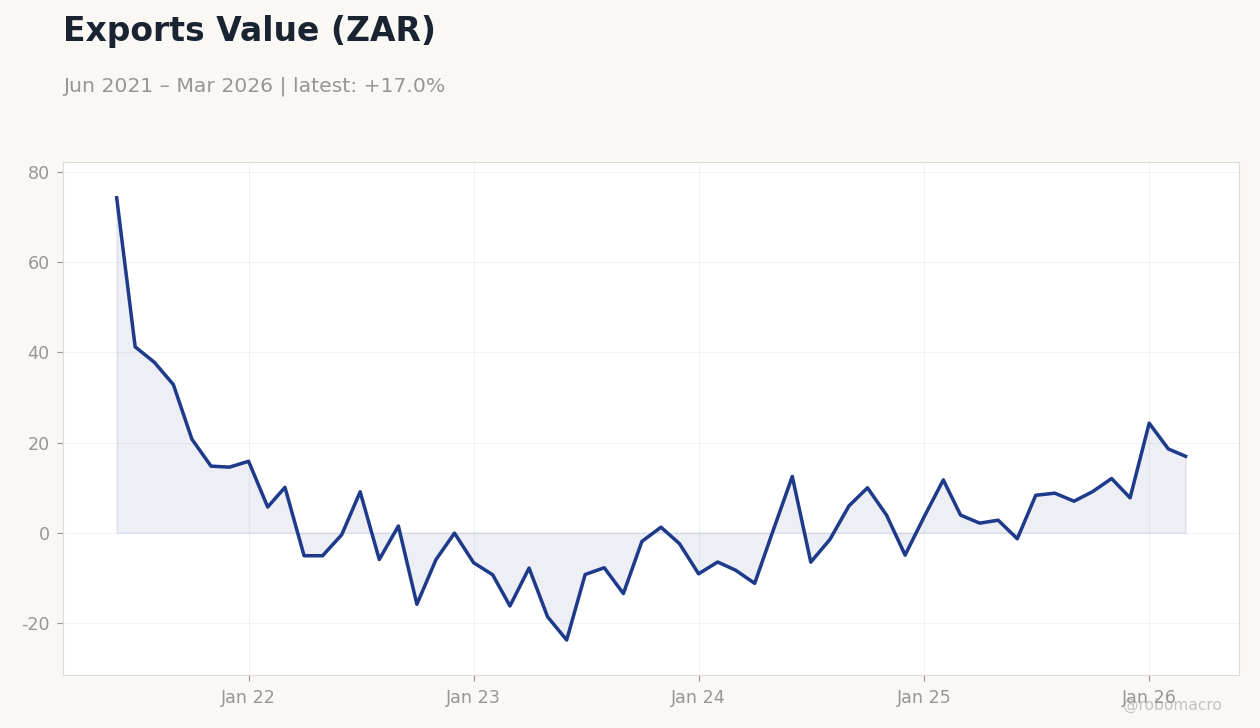

Exports Value (ZAR) | Type: macro_line | Exports (Million ZAR): 16.95 (2026-03-01) | Range: -23.83–74.35 | Trend(6pt): 74.35,-5.956,-1.96,-4.98,18.59,16.95

Exports Value (ZAR) | Type: macro_line | Exports (Million ZAR): 16.95 (2026-03-01) | Range: -23.83–74.35 | Trend(6pt): 74.35,-5.956,-1.96,-4.98,18.59,16.95

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-05-29) | |||

| Trade Balance | 31,870m | - | 08:00 |

- South Africa GDP growth reached a three-year high, driving mixed reactions across equities and fixed income.

- Rand eased against the dollar as investors monitored US-Iran talks and weighed risks of an inflation spike.

- JSE Top 40 declined 0.62% to 106,285.40 while the long-term rate fell 1.44% to 8.92%.

Yesterday's Recap

South African markets closed mixed after the latest GDP release showed the strongest expansion in three years. The JSE Top 40 fell 0.62% to 106,285.40, pressured by a 2.58% drop in Naspers. USD/ZAR eased 0.10% to 16.44 while EUR/ZAR declined 0.17% to 19.10.

Platinum advanced 0.77% to 1,970.10 on industrial demand, offsetting a 0.24% decline in gold. Brent crude rose 1.50% to 104.12. The South Africa long-term rate dropped sharply to 8.92%, reflecting improved sentiment toward the growth outlook.

No major data prints occurred yesterday, leaving the focus on the GDP surprise and external geopolitical developments.

The Day Ahead

Attention turns to the Trade Balance release scheduled for 29 May at 08:00. Markets will assess whether the strong GDP print translates into sustained export momentum. The SARB short-term rate remains steady at 6.75% with no policy meetings imminent.

Resource equities may react to any revisions in mining output expectations. Investors will also track global oil prices given Brent’s recent strength and its direct link to the rand’s terms of trade.

Other Economic Notes

Stronger GDP has lifted near-term growth forecasts but raised questions about capacity constraints in mining and logistics. Data-centre investment continues to support electricity demand and infrastructure spending, partially offsetting load-shedding risks. Fiscal projections remain under scrutiny after recent Treasury allocations for road projects widened the deficit slightly.

Mining firms are securing fresh funding to ramp up gold output, signalling capital inflows into the sector.

Global Macro News

US-Iran diplomatic talks kept external risk sentiment in focus and contributed to rand softness. Brent crude’s 1.50% gain reflected ongoing supply discipline signals from major producers. Global investors continued to monitor US inflation prints that could delay Federal Reserve easing and affect emerging-market flows.

<i>↓ p.2</i>