South Africa Macro Daily(Beta Mode)

Rand Firms as JSE Slips Ahead of SARB

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 105,378.40 | -0.85% |

| USD/ZAR | 16.33 | -0.66% |

| EUR/ZAR | 19.01 | -0.49% |

| Platinum | 1,939.70 | +0.42% |

| Gold | 4,523.20 | +0.05% |

| Brent Crude | 100.21 | -3.22% |

| Naspers | 84,281.00 | -2.05% |

| Bitcoin | 77,278.71 | +0.79% |

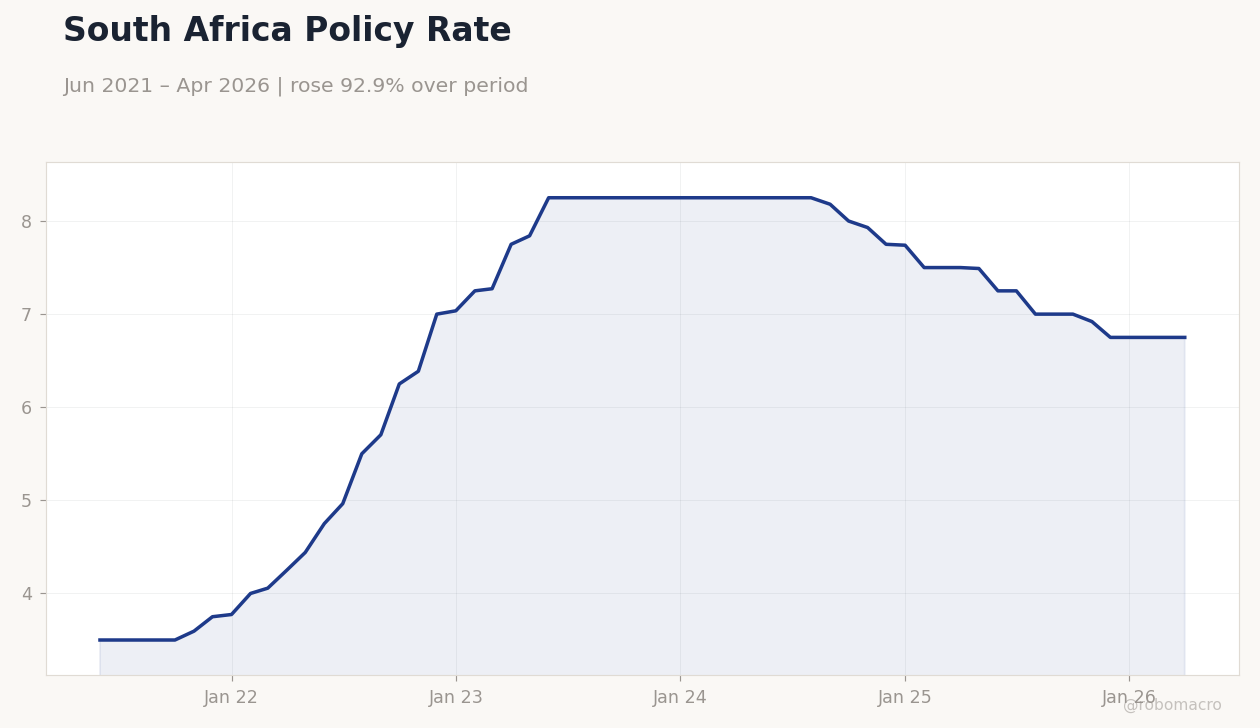

| South Africa Short-term Rate | 6.75% | +0.00% |

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

South Africa Policy Rate | Type: macro_line | Short-term Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.5,8.25,7.75,6.75

South Africa Policy Rate | Type: macro_line | Short-term Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.5,8.25,7.75,6.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-05-29) | |||

| Trade Balance | 31,870m | - | 04:00 |

- USD/ZAR falls 0.66% to 16.33 on softer dollar and steady commodity prices.

- JSE Top 40 drops 0.85% to 105,378.40 while long-term yields ease 1.44% to 8.92%.

- Traders position for next week’s SARB decision with repo rate steady at 6.75%.

Yesterday's Recap

South African markets saw limited movement on a quiet data calendar. The rand strengthened against both the dollar and euro, with USD/ZAR closing at 16.33 and EUR/ZAR at 19.01. Equity markets declined as the JSE Top 40 fell 0.85 percent, pressured by Naspers which dropped 2.05 percent.

Fixed-income markets rallied, pushing the long-term rate down to 8.92 percent. Platinum rose 0.42 percent to 1,939.70 while gold held near 4,523.20. Brent crude fell sharply, declining 3.22 percent to 100.21.

No major economic releases occurred, leaving price action driven by global flows and positioning ahead of the SARB meeting.

The Day Ahead

The Trade Balance for April is scheduled for release on Friday at 04:00 ET and carries medium market impact. No high-frequency indicators are due today or tomorrow. Market focus remains on next week’s SARB Monetary Policy Committee meeting.

Participants will watch for any shift in the committee’s data-dependent stance. Short-term rate futures continue to price a hold at 6.75 percent through the immediate horizon. Volatility is expected to rise as the meeting approaches.

Other Economic Notes

Mining output continues to support the external balance amid firm platinum and gold prices. Load-shedding risks remain contained through winter according to Eskom updates. Fiscal consolidation efforts stay on track with debt-service costs absorbing 21.4 percent of revenue.

Private-sector credit growth and consumer confidence prints later this week offer secondary signals on domestic demand. Broader sentiment hinges on sustained rand stability and contained inflation within the 3–6 percent target band.

Global Macro News

Progress toward a US-Iran deal supported risk sentiment and weighed on the dollar, aiding rand performance. US PCE data due this week will shape expectations for Federal Reserve easing and dollar direction. Brent crude’s decline reflects ample supply signals and softer global demand indicators.

<i>↓ p.2</i>