South Africa Macro Daily(Beta Mode)

Rand Firms Ahead of SARB Decision

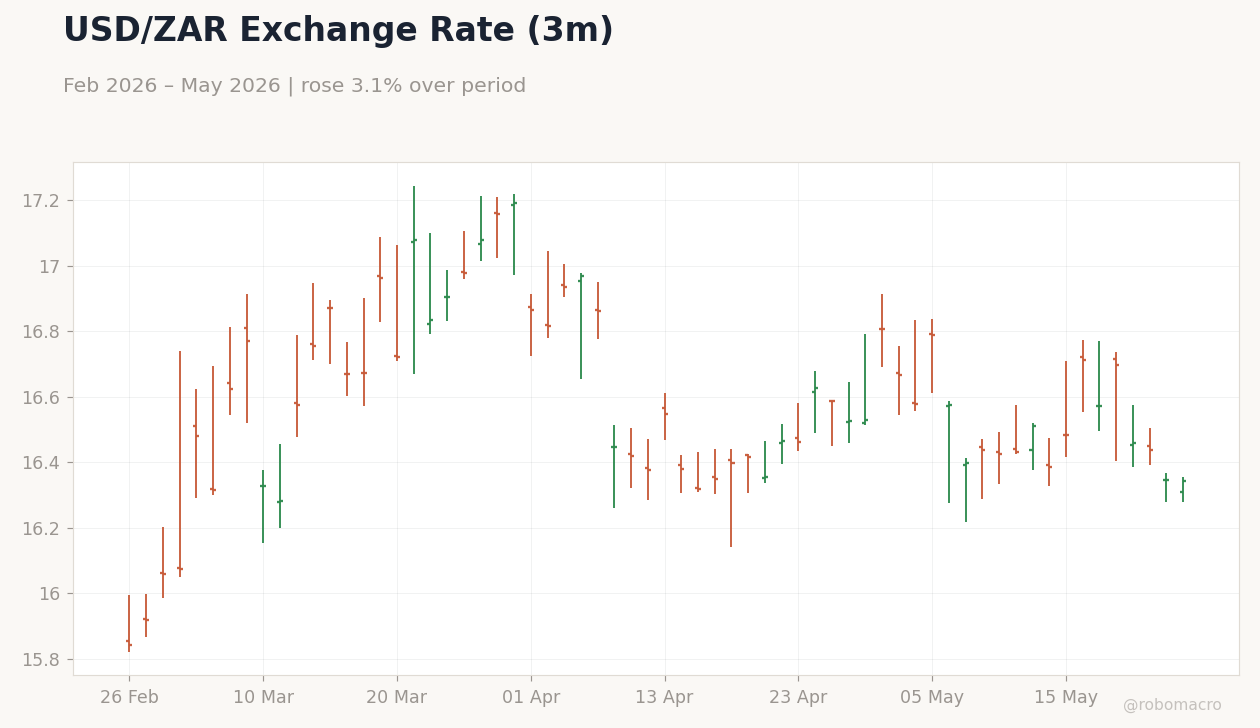

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 108,174.90 | +2.65% |

| USD/ZAR | 16.34 | -0.03% |

| EUR/ZAR | 19.00 | -0.15% |

| Platinum | 1,960.10 | +1.48% |

| Gold | 4,531.60 | +0.23% |

| Brent Crude | 95.45 | -7.81% |

| Naspers | 84,281.00 | -2.05% |

| Bitcoin | 76,841.61 | -0.18% |

| South Africa Short-term Rate | 6.75% | +0.00% |

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

SARB Policy Rate | Type: macro_line | Percent: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.5,8.25,7.75,6.75

SARB Policy Rate | Type: macro_line | Percent: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.5,8.25,7.75,6.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-05-29) | |||

| Trade Balance | 31,870m | - | 08:00 |

- USD/ZAR eased 0.03% to 16.34 as markets positioned for the 29 May MPC meeting.

- JSE Top 40 climbed 2.65% to 108,174.90, led by platinum and gold miners.

- South Africa long-term yields fell 1.44% to 8.92% while the repo rate held at 6.75%.

Yesterday's Recap

Markets priced a steady SARB stance after no domestic data releases on 25 May. The rand posted modest gains against both the dollar and euro amid softer US data and firmer commodity prices. JSE Top 40 advanced as platinum rose 1.48% to 1,960.10 and gold added 0.23% to 4,531.60.

Brent crude dropped 7.81% to 95.45, weighing on energy names but failing to derail the broader equity rally. Naspers declined 2.05% while the short-term rate remained unchanged at 6.75%. Bitcoin slipped 0.18% with limited local impact.

Overall flows reflected positioning ahead of the upcoming trade balance print and MPC decision rather than fresh domestic catalysts.

The Day Ahead

Attention turns to the 29 May trade balance release at 08:00, the sole scheduled South African data point this week. Markets will also monitor global risk sentiment ahead of the SARB MPC meeting later that day. No other local indicators are due before the weekend.

Analysts expect the rand to remain range-bound until the policy statement clarifies the inflation and growth outlook. Any surprise in the trade print could shift front-end yields and USD/ZAR positioning into the decision.

Other Economic Notes

Fiscal risks flagged by BNY continue to cap rand optimism despite the recent softening in inflation prints. Persistent load-shedding concerns have eased in recent weeks, supporting mining output, yet Eskom reliability remains a medium-term constraint. Commodity price volatility, especially in platinum group metals, continues to drive JSE Top 40 swings more than domestic policy signals.

The combination of steady repo rate and declining long-term yields suggests markets are discounting a gradual easing path only after clearer inflation confirmation.

Global Macro News

Progress on US-Iran talks supported risk assets and weighed on the dollar, aiding ZAR crosses. US PCE data later this week will influence global rate expectations and carry-over effects for emerging-market currencies. European yields moved lower, narrowing spreads versus South African bonds and supporting EUR/ZAR.

<i>↓ p.2</i>