South Africa Macro Daily(Beta Mode)

SARB Eyes First Hike Since 2023

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 107,510.00 | -0.42% |

| USD/ZAR | 16.46 | +0.61% |

| EUR/ZAR | 19.08 | +0.24% |

| Platinum | 1,880.90 | -1.97% |

| Gold | 4,403.20 | -1.00% |

| Brent Crude | 95.57 | +1.36% |

| Naspers | 85,583.00 | +0.10% |

| Bitcoin | 72,825.77 | -3.96% |

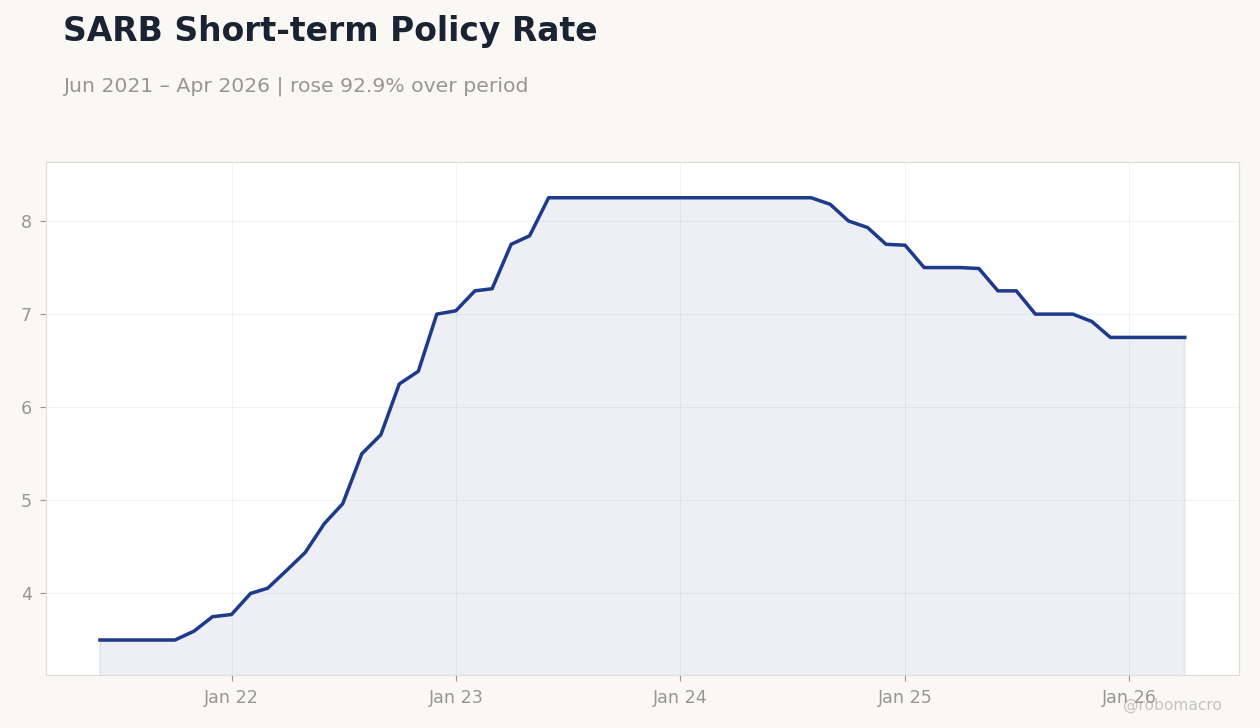

| South Africa Short-term Rate | 6.75% | +0.00% |

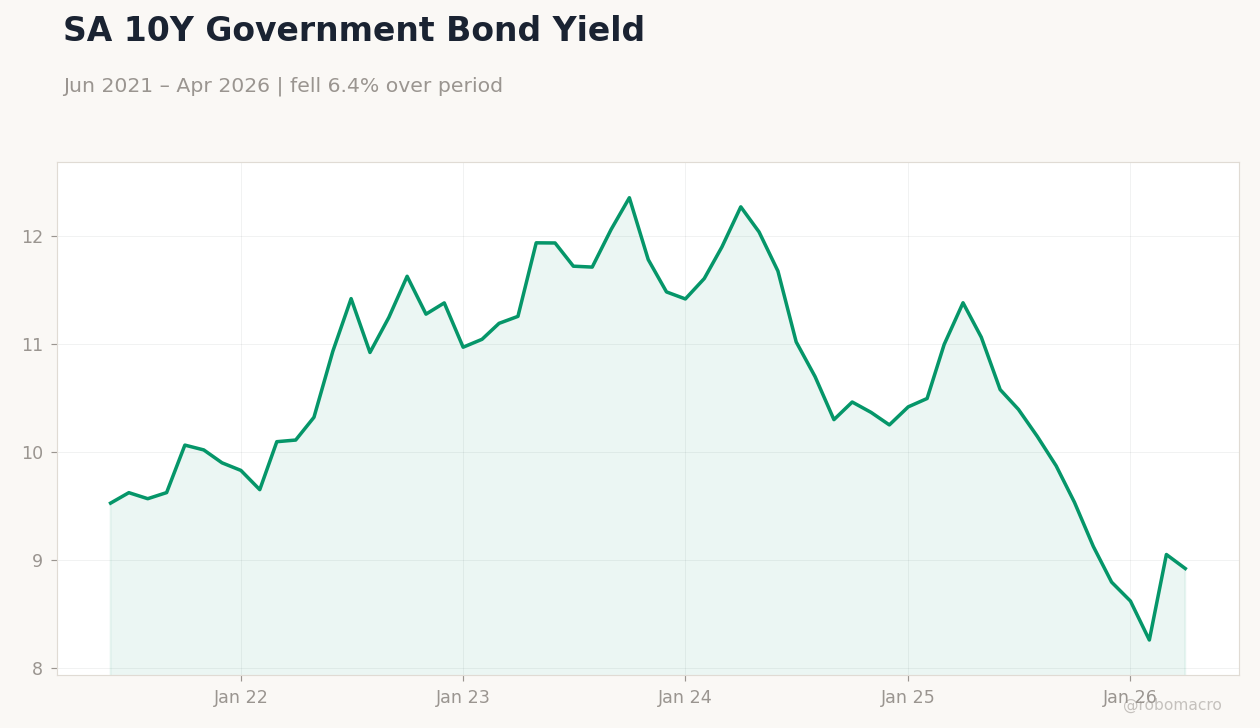

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

SARB Short-term Policy Rate | Type: macro_line | Policy Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.5,8.25,7.75,6.75

SARB Short-term Policy Rate | Type: macro_line | Policy Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.5,8.25,7.75,6.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-05-29) | |||

| Trade Balance | 31,870m | - | 04:00 |

- SARB signals rate hike intent as Iran war lifts inflation risks

- JSE Top 40 falls 0.42% while USD/ZAR rises 0.61% to 16.46

- Business confidence index climbs 2.4% in latest SARB reading

Yesterday's Recap

South African markets closed mixed on 27 May with the JSE Top 40 declining 0.42% to 107,510 amid resource stock weakness. The rand weakened as USD/ZAR climbed 0.61% to 16.46 and EUR/ZAR advanced 0.24% to 19.08. Platinum fell 1.97% to 1,880.90 while gold slipped 1.00% to 4,403.20; Brent crude gained 1.36% to 95.57.

The long-term government bond yield dropped 1.44% to 8.92% as the short-term rate held at 6.75%. SARB data showed a 2.4% rise in the business confidence index, signalling modest economic improvement. Reports highlighted growing expectations that the central bank will raise rates for the first time since 2023 to counter imported inflation pressures.

The Day Ahead

Markets await the May trade balance release scheduled for 04:00 ET on 29 May. The prior print stood at 31.87 billion rand with no consensus forecast available. No other South African data prints are listed for the session.

Attention will centre on whether the trade surplus narrows or widens amid softer commodity prices. The release could influence rand volatility and near-term rate expectations. No MPC speeches are scheduled before the next policy meeting.

Other Economic Notes

The 2.4% BCI increase points to gradual improvement in domestic sentiment despite external headwinds. Xenophobic tensions have prompted Ghana to begin repatriating citizens, adding social friction that could weigh on labour markets and investor perception. Mining output remains under pressure from lower platinum and gold prices.

Eskom load-shedding risks persist though not quantified in today’s releases. Treasury continues to direct fuel-levy revenue toward deficit reduction.

Global Macro News

Iran-related supply concerns have pushed Brent higher and stoked imported inflation fears for South Africa. Softer US PCE data improved broader EM risk appetite but failed to support the rand. OPEC+ supply discipline signals supported energy prices while Chinese auto data lifted platinum briefly before today’s reversal.

Global bitcoin weakness of 3.96% reflected risk-off flows that also pressured JSE resources. EM currencies broadly faced headwinds from higher US yields and geopolitical premiums. South Africa’s terms of trade remain sensitive to these commodity swings.