South Africa Macro Daily(Beta Mode)

Rand Holds Steady as JSE Eases on Quiet Day

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 106,822.80 | -0.38% |

| USD/ZAR | 16.22 | -0.92% |

| EUR/ZAR | 18.90 | -0.02% |

| Platinum | 1,947.90 | +1.34% |

| Gold | 4,545.10 | -0.34% |

| Brent Crude | 93.28 | +1.34% |

| Naspers | 85,213.00 | +0.38% |

| Bitcoin | 73,320.01 | -0.59% |

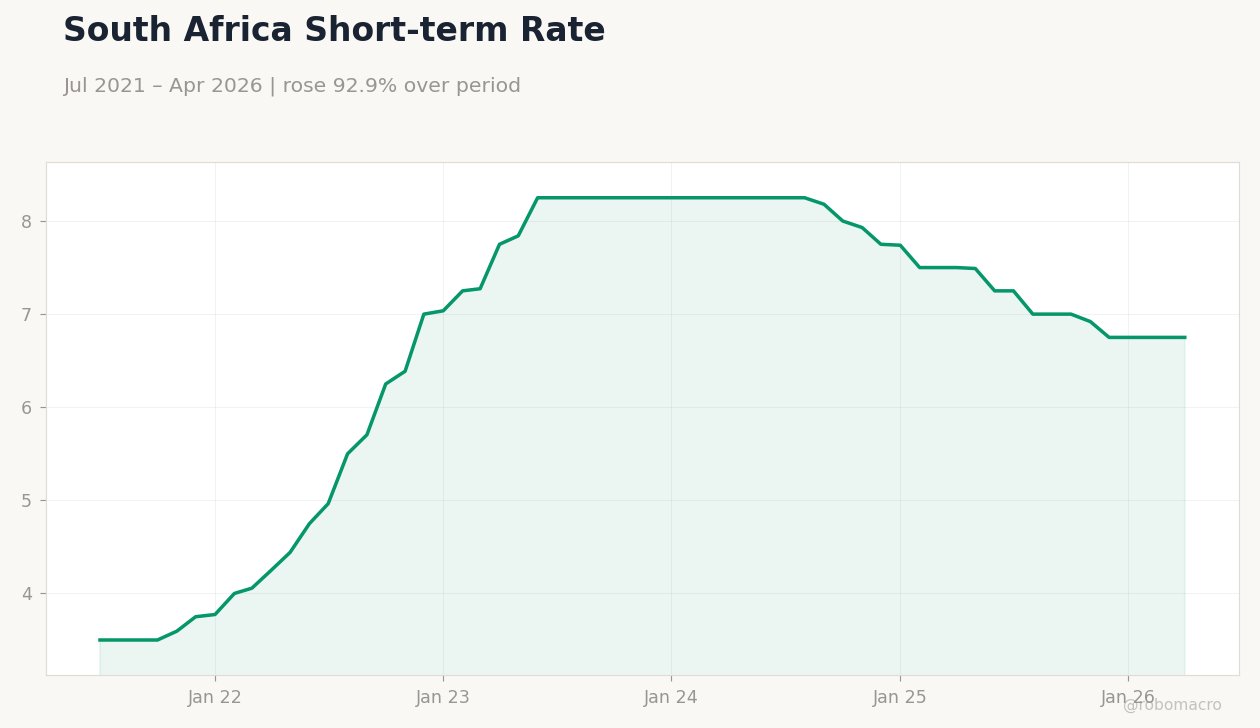

| South Africa Short-term Rate | 6.75% | +0.00% |

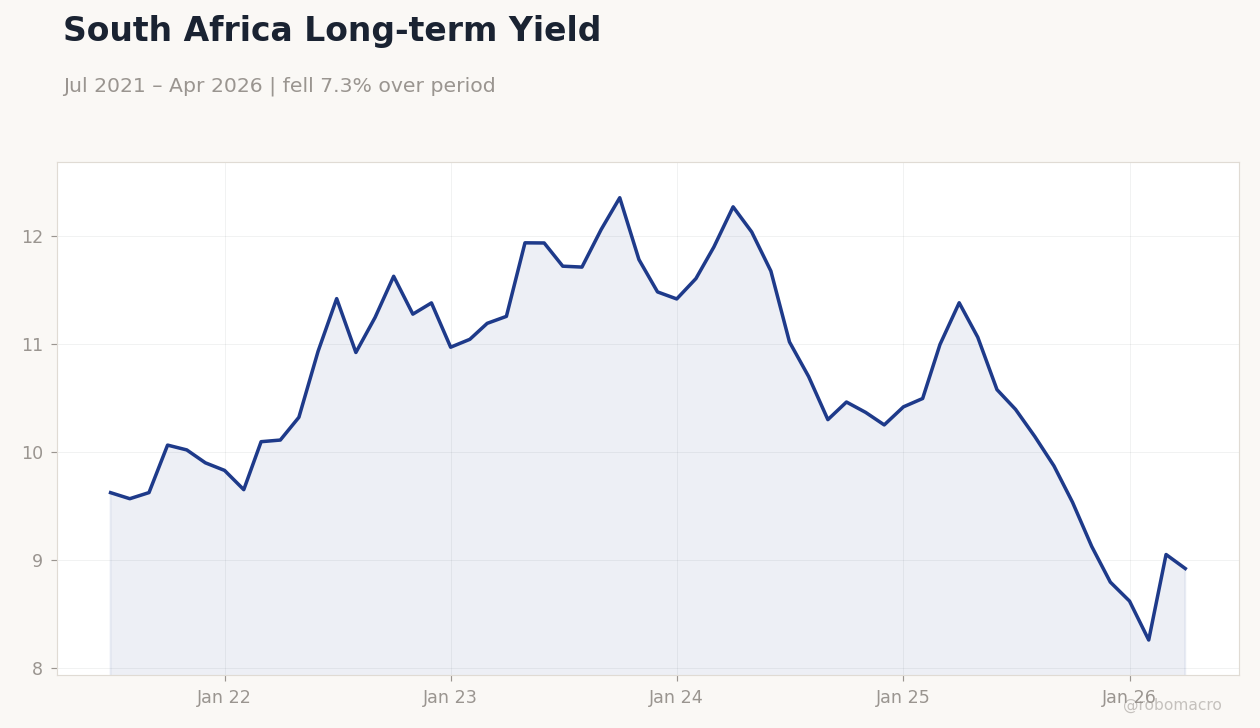

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

South Africa Long-term Yield | Type: macro_line | 10Y Yield %: 8.92 (2026-04-01) | Range: 8.257–12.36 | Trend(6pt): 9.624,11.25,11.79,10.42,9.05,8.92

South Africa Long-term Yield | Type: macro_line | 10Y Yield %: 8.92 (2026-04-01) | Range: 8.257–12.36 | Trend(6pt): 9.624,11.25,11.79,10.42,9.05,8.92

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- USD/ZAR falls 0.92% to 16.22 as rand steadies ahead of sparse releases

- JSE Top 40 declines 0.38% to 106,822.80 while long-term yields drop 1.44%

- Platinum rises 1.34% to $1,947.90 offsetting gold's 0.34% decline

Yesterday's Recap

South African markets absorbed limited domestic data with the rand holding steady in a narrow range. The JSE Top 40 closed lower at 106,822.80 after a 0.38% decline driven by selective mining weakness. USD/ZAR eased to 16.22, reflecting modest rand strength against a softer dollar.

Long-term government yields fell sharply to 8.92% as the SARB repo rate remained unchanged at 6.75%. Brent crude advanced 1.34% to $93.28, supporting energy-linked equities, while Naspers gained 0.38%. No major Stats SA releases occurred, leaving traders focused on external commodity signals and local liquidity conditions.

The Day Ahead

The calendar shows no scheduled South African data prints or SARB events for the coming session. Attention will turn to global risk sentiment and any follow-through in commodity prices. USD/ZAR and EUR/ZAR moves will likely dictate rand direction given the absence of local catalysts.

Equity traders may monitor Naspers and resource stocks for continuation of recent flows. Load-shedding updates from Eskom remain a background factor for industrial output expectations.

Other Economic Notes

Persistent high real rates at 6.75% continue to weigh on household consumption and credit growth. Mining output faces mixed signals as platinum benefits from industrial demand while gold prices soften. Broader concerns over cumulative rate effects have prompted recession risk discussions among analysts, though current indicators show no immediate contraction.

Energy supply reliability stays central to medium-term investment decisions across manufacturing and mining sectors.

Global Macro News

Higher Brent prices at $93.28 provide a tailwind for South Africa's terms of trade and fiscal revenues. US dollar softness supported emerging-market currencies including the rand overnight. Platinum's advance reflects steady global auto and industrial demand outside China.

Bitcoin's 0.59% dip to $73,320 offered little direct spillover to local assets. European growth concerns could temper external demand for South African exports in coming months. <i>↓ p.2</i>