South Africa Macro Daily(Beta Mode)

JSE Slides as Rand Weakens on 4% Inflation

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 104,171.80 | -2.48% |

| USD/ZAR | 16.27 | +0.24% |

| EUR/ZAR | 18.88 | -0.14% |

| Platinum | 1,958.50 | +1.88% |

| Gold | 4,543.40 | +1.52% |

| Brent Crude | 94.21 | -0.81% |

| Naspers | 85,213.00 | +0.38% |

| Bitcoin | 70,693.15 | -3.92% |

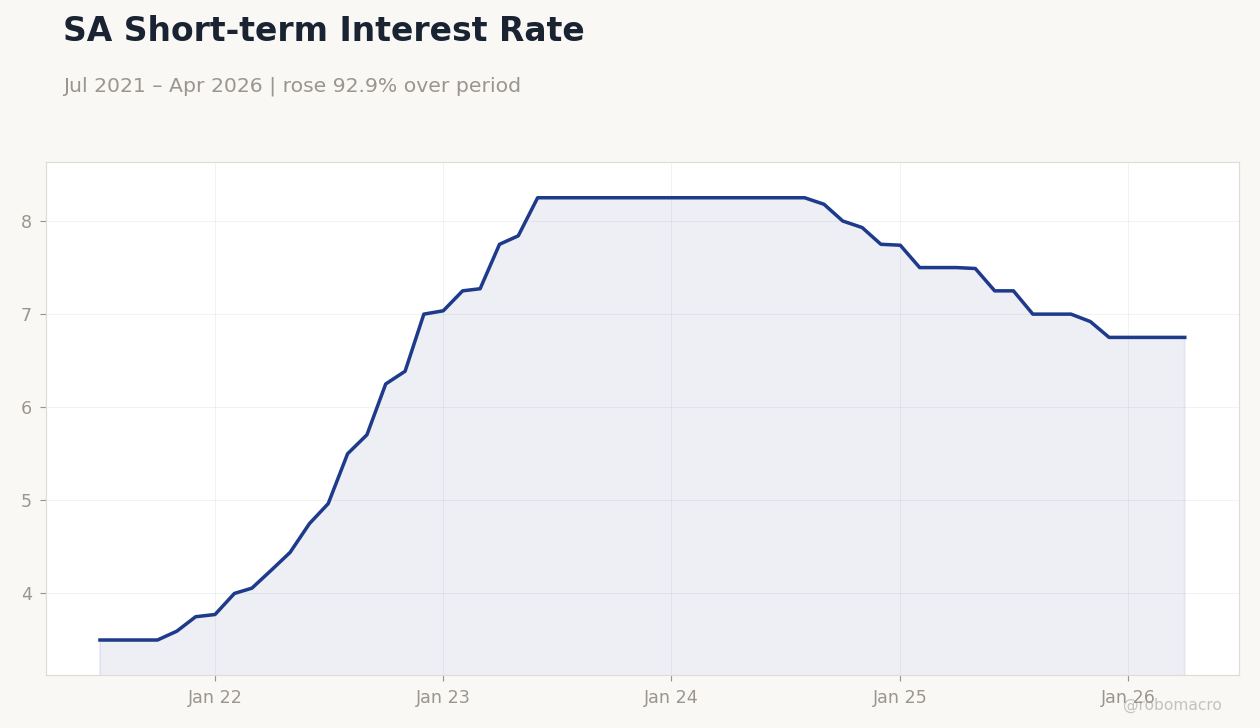

| South Africa Short-term Rate | 6.75% | +0.00% |

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

SA Short-term Interest Rate | Type: macro_line | Policy Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.705,8.25,7.74,6.75

SA Short-term Interest Rate | Type: macro_line | Policy Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.705,8.25,7.74,6.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- JSE Top 40 fell 2.48% to 104,171.80 while USD/ZAR rose 0.24% to 16.27 on softer demand.

- South African inflation reached 4%, prompting warnings of household financial pressure at the 6.75% repo rate.

- Platinum and gold rose 1.88% and 1.52% respectively, supporting mining equities amid global supply concerns.

Yesterday's Recap

South African markets closed lower as the JSE Top 40 declined 2.48% amid fading domestic demand and ongoing supply disruptions. The rand weakened modestly against the dollar, with USD/ZAR climbing to 16.27, while EUR/ZAR eased to 18.88. Long-term government yields fell 1.44% to 8.92%, reflecting some relief in the bond market despite the rate environment.

Platinum advanced to 1,958.50 on stronger autocatalyst demand, and gold reached 4,543.40 amid safe-haven buying. Brent crude slipped 0.81% to 94.21 as traders weighed OPEC+ discipline against Iran-related tensions. Naspers edged up 0.38% while Bitcoin dropped 3.92%.

No major data releases occurred, leaving price action driven by global commodity moves and local sentiment.

The Day Ahead

The South African calendar remains quiet with no scheduled releases for the next session. Attention will stay on global oil and fertilizer price developments stemming from the Iran conflict and their pass-through to local inflation. Market participants will monitor rand crosses for any follow-through from yesterday’s modest depreciation.

Eskom’s load-shedding schedule and mining output data will also draw focus given recent Medupi unit issues. Thin liquidity may amplify moves in USD/ZAR and JSE resources.

Other Economic Notes

Business Leadership South Africa urged continued structural reforms to preserve macroeconomic stability amid elevated borrowing costs. Wheat farmers face rising input costs from disrupted global fuel and fertilizer markets linked to the Iran conflict. Manufacturer sentiment deteriorated in May as domestic demand slumped and supply chains remained strained.

The EU Carbon Border Adjustment Mechanism is emerging as a key challenge for South African exporters reliant on carbon-intensive production. Reform momentum remains essential to anchor long-term growth expectations.