South Africa Macro Daily(Beta Mode)

Business Confidence Slumps to 39, Bonds Rally

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 106,257.30 | +2.00% |

| USD/ZAR | 16.29 | +0.39% |

| EUR/ZAR | 18.93 | -0.17% |

| Platinum | 1,933.60 | -0.20% |

| Gold | 4,500.50 | +0.25% |

| Brent Crude | 97.13 | +1.18% |

| Naspers | 92,477.00 | +10.28% |

| Bitcoin | 66,713.49 | -6.46% |

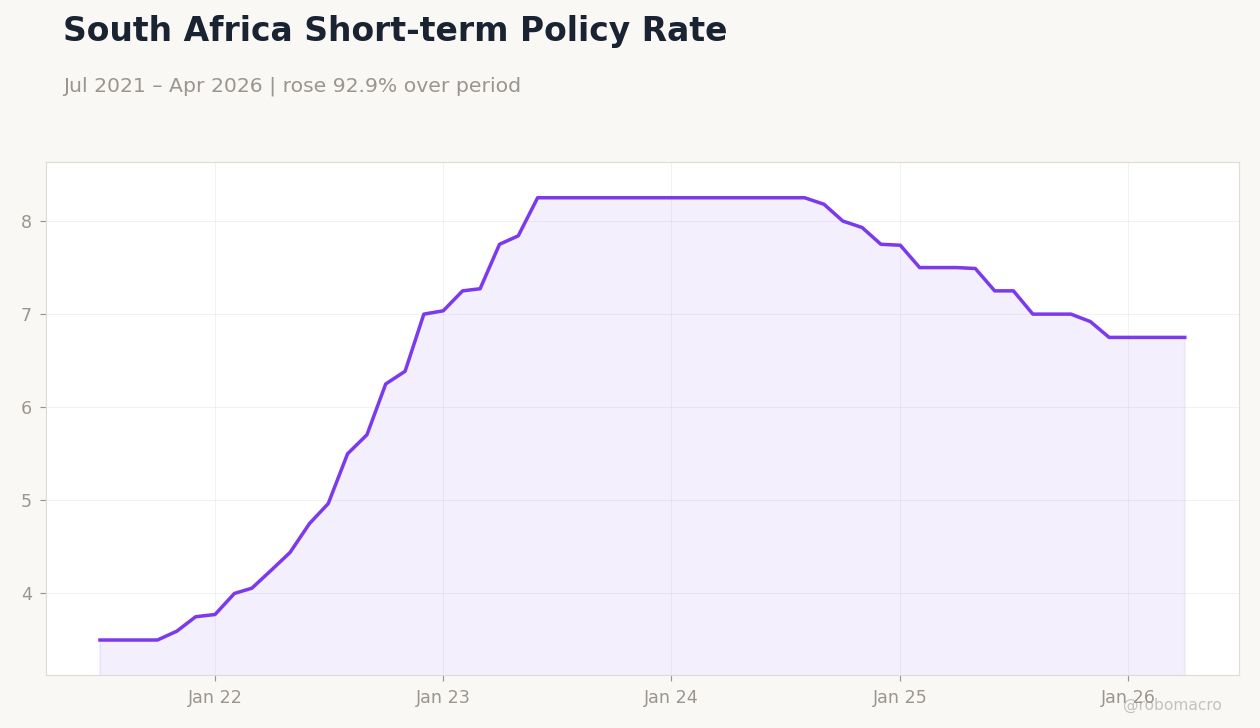

| South Africa Short-term Rate | 6.75% | +0.00% |

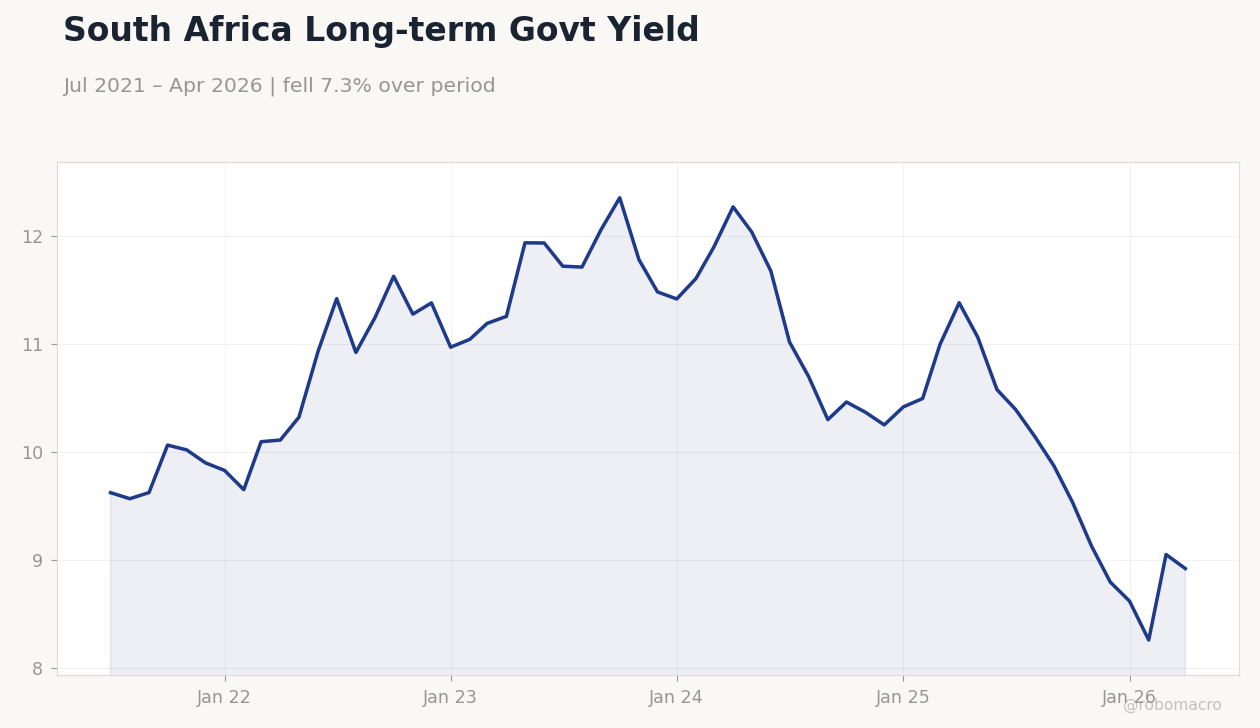

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Business Confidence Index | 47 | - | 39 |

South Africa Long-term Govt Yield | Type: macro_line | 10Y Yield (%): 8.92 (2026-04-01) | Range: 8.257–12.36 | Trend(6pt): 9.624,11.25,11.79,10.42,9.05,8.92

South Africa Long-term Govt Yield | Type: macro_line | 10Y Yield (%): 8.92 (2026-04-01) | Range: 8.257–12.36 | Trend(6pt): 9.624,11.25,11.79,10.42,9.05,8.92

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- South Africa’s Business Confidence Index fell sharply to 39 in May from 47 previously, signalling weaker sentiment.

- JSE Top 40 climbed 2.00% to 106,257.30 while the long-term government bond yield dropped 1.44% to 8.92%.

- USD/ZAR rose 0.39% to 16.29 as markets digested the confidence data and commodity price moves.

Yesterday's Recap

The Business Confidence Index release dominated South African data flow, printing at 39 and marking a steep eight-point decline that highlighted deteriorating corporate sentiment amid persistent structural constraints. Equity markets responded positively, with the JSE Top 40 advancing 2.00% and Naspers surging 10.28% to lead gains. Fixed-income markets rallied, driving the South Africa Long-term Rate down 1.44% to 8.92% and pushing the 10-year yield below 8.50%.

The rand showed modest weakness, with USD/ZAR rising 0.39% to 16.29 while EUR/ZAR eased 0.17% to 18.93. Commodity prices provided mixed support, as gold advanced 0.25% to 4,500.50 and Brent crude gained 1.18% to 97.13, while platinum slipped 0.20%. Short-term rates remained unchanged at 6.75%, leaving the policy stance on hold.

The Day Ahead

South African markets face a data-light session with no scheduled domestic releases. Attention will turn to global commodity price developments and external risk sentiment that typically influence rand and JSE flows. The absence of local indicators leaves the recent bond rally and equity gains exposed to any shift in global oil or precious-metals prices.

Traders will also monitor cross-border news that could affect investor positioning in emerging-market assets. With the next SARB MPC meeting still weeks away, markets are expected to consolidate around current levels absent external shocks.

Other Economic Notes

Elevated oil prices at 97.13 continue to pose downside risks to South African growth through higher import costs and transport inflation. The sharp drop in business confidence adds to concerns about private-sector investment momentum in an environment of elevated borrowing costs. Bond-market participants appear to be pricing a slower growth trajectory, supporting the rally in longer-dated yields.

Energy-supply constraints remain a latent headwind for mining output despite the recent absence of widespread load-shedding reports.

Global Macro News

Stronger Brent crude prices at 97.13 reflect ongoing OPEC+ supply discipline and geopolitical tensions that support South Africa’s terms of trade via higher export revenues from coal and metals. <i>↓ p.2</i>