South Africa Macro Daily(Beta Mode)

SA Confidence Slumps to 39, Rand Holds Highs

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 105,239.50 | -0.96% |

| USD/ZAR | 16.34 | +0.55% |

| EUR/ZAR | 18.97 | +0.42% |

| Platinum | 1,881.30 | +0.67% |

| Gold | 4,500.90 | +1.45% |

| Brent Crude | 97.15 | -0.67% |

| Naspers | 88,935.00 | -3.83% |

| Bitcoin | 64,067.85 | -3.95% |

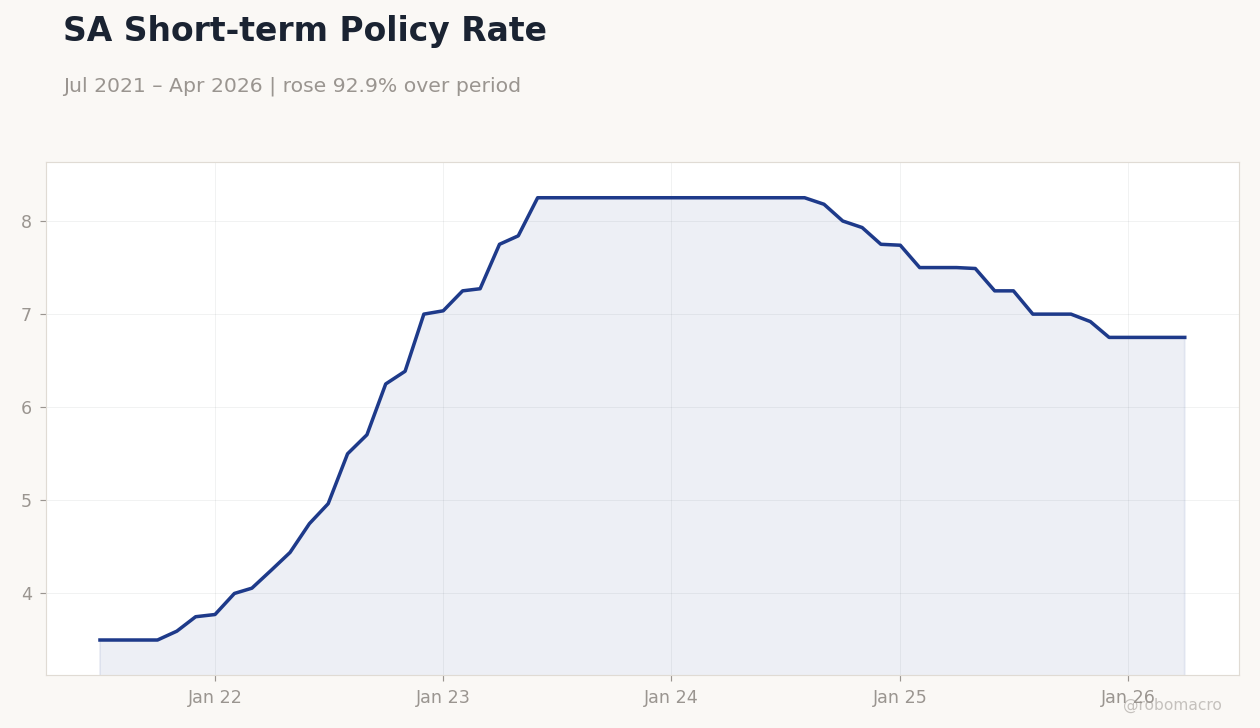

| South Africa Short-term Rate | 6.75% | +0.00% |

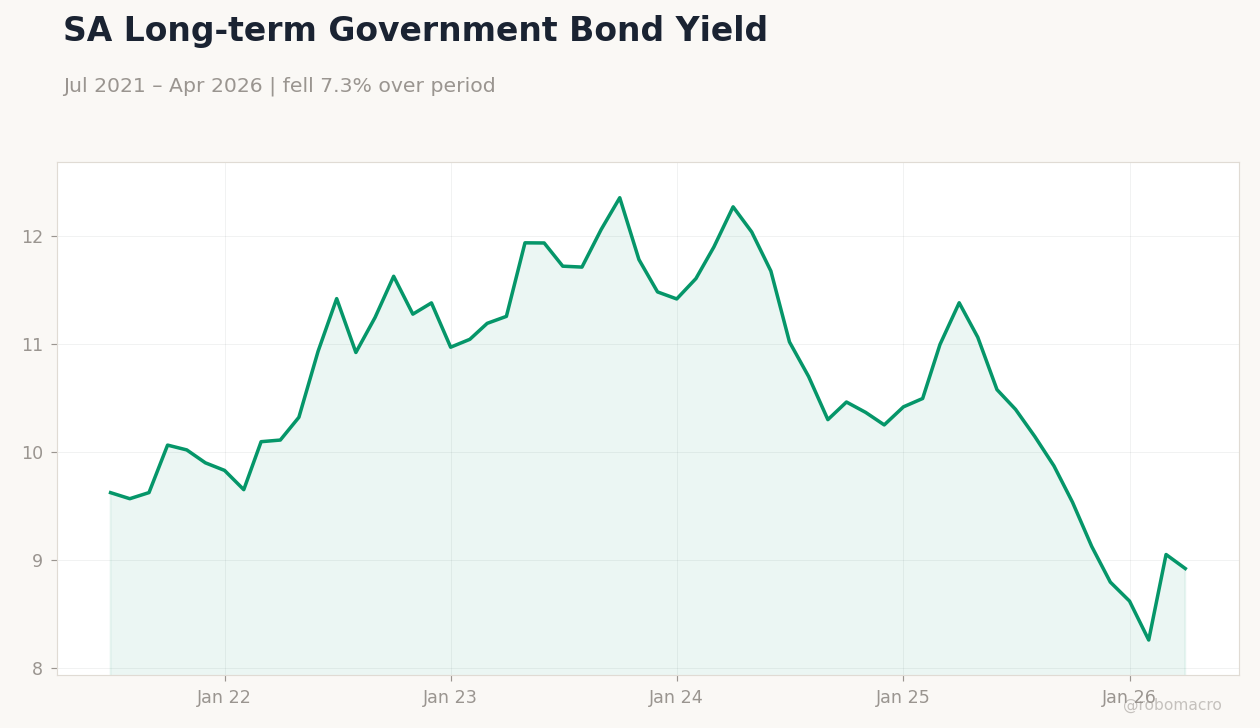

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Business Confidence Index | 47 | - | 39 |

SA Short-term Policy Rate | Type: macro_line | Policy Rate (%): 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.705,8.25,7.74,6.75

SA Short-term Policy Rate | Type: macro_line | Policy Rate (%): 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.705,8.25,7.74,6.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Business Confidence Index plunged to 39 from 47, signalling sharp deterioration in sentiment.

- JSE Top 40 fell 0.96% while USD/ZAR rose 0.55% to 16.34 amid mixed commodity moves.

- Long-term SA yields eased 1.44% to 8.92% as gold climbed 1.45% to $4,500.90.

Yesterday's Recap

South Africa’s Business Confidence Index dropped sharply to 39 on 3 June, down from 47 previously, reflecting weaker corporate optimism amid persistent structural constraints. The JSE Top 40 closed 0.96% lower at 105,239.50, pressured by Naspers declining 3.83%. USD/ZAR rose 0.55% to 16.34 while EUR/ZAR gained 0.42% to 18.97, trimming earlier gains near three-month highs.

Gold advanced 1.45% to $4,500.90 and platinum added 0.67%, supporting the mining complex, whereas Brent crude fell 0.67% to $97.15. The South Africa long-term rate declined 1.44% to 8.92% with the short-term rate steady at 6.75%. Reports of anti-migrant violence in the Western Cape added to domestic uncertainty without immediate market reaction.

The Day Ahead

No scheduled South African data releases appear on 4 June, leaving markets to digest the confidence print. Traders will monitor USD/ZAR behaviour around the 16.12 technical level flagged by Societe Generale. Broader commodity price action and any follow-through from weekend violence may influence rand flows.

The absence of high-frequency indicators keeps focus on external drivers such as global risk sentiment and oil prices. SARB speakers remain absent from the calendar.

Other Economic Notes

S&P Global highlighted South Africa as a growth outlier facing rising oil-price risks that could widen the current-account gap. Persistent electricity supply constraints continue to cap industrial output despite recent improvements at Eskom. Xenophobic attacks have triggered repatriation plans from Malawi and other neighbours, threatening labour availability in key sectors.

These developments compound already fragile business sentiment evident in the latest confidence reading.

Global Macro News

The Swiss central bank warned of a broad global growth slowdown that may weigh on South Africa’s export demand. Firmer Chinese PMI data lifted some commodity prices but failed to offset Brent’s decline. OPEC+ supply signals kept oil markets volatile, directly affecting SA import costs and the rand’s terms-of-trade support.

<i>↓ p.2</i>